When Faith and Finances Collide

Ask Abbi Perets about financial pain, and she starts talking about grape juice. Specifically, she's referring to the half-gallon bottles of grape juice that her local grocery sells for $9 each. Drinking the juice is an integral part of the prayer ritual that Abbi, her husband, Guy, and their four children follow every Friday and Saturday to commemorate the Jewish Sabbath. Like all the food in the Perets household, the juice must be kosher — that is, prepared according to Jewish dietary laws. And the $9 juice, more than three times the price of the regular kind, is the only kosher grape juice she can find.

It is impossible to put a price on religious belief. But as Abbi Perets knows from her trips to Kroger, exercising that belief doesn't come free. For the most devout practitioners — perhaps 15% of Americans, if measured by how frequently they attend services — following their faith's precepts often has a profound financial impact: Religion guides how they make, spend, and invest their money. And it often leads to financial decisions and stresses far different from those of people who don't share their beliefs.

To explore how religion affects the way people manage their money, we visited with three families of different faiths who are struggling to reconcile their spiritual beliefs with their wallets. Their stories, and our advice to them, follow. What all three households have in common: the desire to let faith guide their economic prospects, without undermining their family's security or long-term goals. As you'll see, that isn't always an easy task.

Coping With the Cost of Keeping Kosher

It's not just the $9 grape juice doing damage to the Perets budget. The kosher mozzarella that Abbi uses to make pizza costs $5, double the price of the non-kosher kind; brisket, the quintessential Jewish comfort food, costs a whopping $14.99 a pound vs. $1.99. It all adds up to a monthly grocery bill of more than $1,000 for Abbi, 33, Guy, 36, and their four kids, ages 3 to 9 (a fifth is due in July).

But for Abbi and Guy, buying kosher food, no matter what the cost, is a necessity, not a choice. They're Orthodox, which means that, of the roughly 5 million Jews in the U.S., they're among the 13% whose practice of Judaism hews most closely to the Hebrew Bible's literal commandments and to centuries of rabbinical instruction. That means eating only kosher food and keeping meat and dairy products separate. It means doing nothing classified as work on the Sabbath, or Shabbat — even riding in a car. It means sending their children to a private religious school so that they become steeped in the traditions of their faith. Says Guy: "Kids that go to public school — a high percentage of them lose their religion." And each of those practices comes with a high price tag attached.

Abbi and Guy met and married in Israel. She was an American Jew who dropped out of college to live there; Guy, a native Israeli, was an air force officer. They moved to the U.S. in 2000 and began shopping for a home near Los Angeles. A top priority: finding a house inside what's known as an eruv, a symbolic wall around an Orthodox community that permits certain activities, such as pushing a baby stroller, that are otherwise forbidden on Shabbat. Houses within the eruv cost more than those outside it; homes within walking distance of a major synagogue are even more expensive, given the prohibition against driving on Shabbat. The house that the Peretses bought, a half mile from the synagogue, cost $295,000 — at least $50,000 more than homes just a few blocks farther away.

Guy, a developer for a banking software company, and Abbi, a free-lance writer, were then making more than $100,000 a year. But they felt squeezed by the high cost of California living. So after researching Orthodox communities in other areas, they decided to move to Houston. Using part of the $300,000 they made selling their Los Angeles home, they bought a three-bedroom house just a three-minute walk from their new synagogue for $270,000 — about $100,000 more than they would have paid for a similar home in a non-Orthodox neighborhood, Guy says. They spent another $30,000 renovating the kitchen. Among the upgrades: putting in two sinks, two ovens, and two dishwashers — one for meat and one for dairy.

But while it is cheaper to live in Houston, the couple's expenses have grown. Their third child, Adi, was diagnosed with Sotos syndrome, a condition marked by accelerated physical growth but delayed mental development, which has caused their out-of-pocket medical bills to soar. Meanwhile, the everyday expenses of living Judaically keep adding up. The biggest is private school tuition for the kids. (Only Adi goes to public school, so he can attend special-education classes.) Total tab, after financial aid: $18,000 a year.

The Peretses also give regularly to their synagogue and community. Annual dues are $600; plus, as is customary, they sponsor meals for the congregation, at a cost of about $500, to celebrate happy occasions, such as a child's birthday. As is also tradition in Orthodox neighborhoods, panhandlers often ring their doorbell with an introductory letter from a rabbi, asking for charity. Most of the time, Abbi gives.

The Peretses now earn $135,000, but they're still feeling squeezed, particularly since Guy's employer just cut salaries 5%. They're anxious about how they'll keep paying religious school tuition year after year, particularly with the added expense of another child. With Guy's 401(k) down 50%, they're also worried about the long term, like how they'll pay for Adi's care when he's older.

What to Do Now

To help the Peretses get their finances on track, given the extra expenses of their Orthodox faith, Money arranged a meeting with Cole Campbell, a financial planner in Houston. His recommendations:

Free up cash. To ease the strain on their budget, Campbell suggests that the Peretses consolidate and restructure their debt. He estimates they'll have an extra $1,200 to $1,500 a month if they refinance their 5.5%, 15-year mortgage and roll their credit card debt into a new, 30-year mortgage at recent local rates between 4.6% and 4.9%. That should cover future tuition increases and allow the couple to beef up retirement account contributions to compensate for recent losses.

Guy likes the idea, but Abbi is afraid they would simply run up their credit cards again. She blames Guy's impulsive spending. "He cannot leave the house without buying something for Adi," she says. Abbi says she'll go ahead with the refi only if they have a trial period beforehand proving they can stick to a strict budget.

Get education covered. Since private school is so important, Campbell thinks the couple should add to their insurance to cover tuition if Guy dies young. While Guy is already insured for $1.9 million, the planner advises adding another $500,000 in 30-year term coverage. Cost: about $440 a year.

Abbi and Guy are sure the school wouldn't drop the kids if he died prematurely, given their community's generosity toward bereaved families. Another reason not to worry: the tradition of matchmaking among the Orthodox. Says Abbi: "There is no way the community will let me be unmarried for more than two years."

Protect the kids. Abbi and Guy don't have wills, nor have they made any provisions for Adi's long-term care as an adult. Get on it, Campbell urges. For Adi, the planner suggests a special-needs trust, which can be used to pay for his living expenses without disqualifying him for government benefits. To fund the trust, Abbi and Guy can name it as a beneficiary on their life insurance policies.

Abbi thinks they haven't written wills because they haven't decided who should take care of the children if she and Guy were gone. "What do you say to someone — have my five children?" But she says they'll get started on the process.

Balancing Age-Old Beliefs and Modern Life

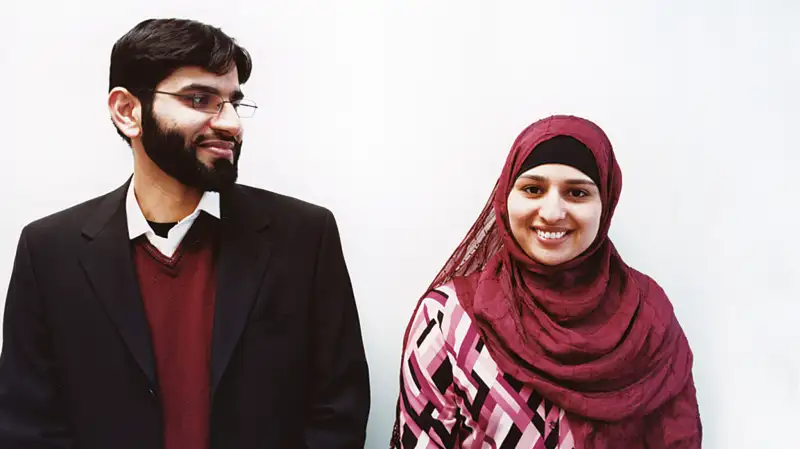

Kashif Saroya held out against getting a credit card for as long as he could. As a Muslim, he was mindful of the prohibition in the Qur'an, Islam's holiest book, against paying or receiving riba, usually understood as interest. That meant no plastic.

But just saying no to credit in a country that runs on it was a lot harder than Saroya anticipated — as he learned one day in 2003, five years after leaving Pakistan to study and work in the U.S. The Minneapolis resident needed to rent a car to pick up his parents, who were flying to America to visit him for the first time. But the rental agent wouldn't hand over the vehicle without a credit card. Panicked that he'd leave his parents stranded, Kashif got a friend to rent the car and let him sign on as a second driver. A few days later he applied for his own Visa. Just in case.

Saroya and his wife, Lori, both 28, constantly feel the tug between their desire to adhere to the teachings of Islam and the practical realities of life in the modern U.S. Take the Muslim admonition against paying or earning interest. Strictly interpreted, the rules make it tough to buy a house (traditional mortgages are off-limits), finance a major purchase (no credit cards), or put together a diversified portfolio (no bonds). Investing in stocks is limited as well — companies involved in forbidden activities (such as lending, gambling, and serving or making alcohol) are prohibited.

Lori, who grew up in Iowa, has also found that compromises are sometimes inevitable. Her scholarships and part-time jobs weren't enough to pay for college in St. Paul, so she reluctantly took out more than $30,000 in student loans — but only after first consulting Islamic scholars, who assured her that borrowing for her education was permissible.

The couple met in Minneapolis, while Lori was still at school and Kashif was working as a systems analyst. He had launched a summer camp for Muslim youth; Lori volunteered to be a counselor there. Their 2004 courtship was a new-world twist on an old-world arranged union: Former campers set them up on a chaperoned date; within three months they were married.

Soon afterward, they bought a $247,000 four-bedroom home in the suburbs. To finance the purchase, Kashif found one of the few U.S. banks offering a mortgage compliant with shari'a, or Islamic law. It's not, strictly speaking, a loan. Instead, the mortgage is structured as a purchase of the home in partnership with the bank; the Saroyas' monthly payments are part rent, part repurchase of the bank's share of the house. The mortgage costs $1,800 a year more than a conventional loan. But it's worth it, says Kashif: "We didn't want to feel that we took the easy route for our own financial comfort."

The Saroyas earn a healthy income for a young couple — between Kashif's job in IT and Lori's work for a victims' services program, they make $117,500 a year. But they don't spend much on themselves. Their biggest outlays are on community service work. Lori estimates that, for one, she's spent about $15,000 to establish the Minnesota chapter of the Council on American-Islamic Relations, which advocates for Muslims facing discrimination. The couple also follow Islam's rules on zakat — a charitable donation roughly equal to 2.5% of their net worth. While they're obligated to give only $500 a year, the Saroyas donate $10,000. "Whatever you have," says Lori, "there are other people who need it more."

Their long-term goals, however, are costly. They'd like to make hajj — the pilgrimage to Mecca that, like zakat, is a pillar of Islamic faith. They'd like to start a family. And they'd like to retire in their fifties to do community service full-time. To reach those goals, they realize they need to invest (currently they have only $17,000 saved). But they've been reluctant to do so — Kashif didn't contribute to his 401(k) for the first four years he was eligible and now puts in only enough to get the company match — because they worry their choices will be unacceptable under Islam. "We don't want to do something inappropriate," says Kashif.

What to Do Now

To help the Saroyas make the right choices, Money consulted Mohammad Raghib, a financial adviser in Los Alamitos, Calif., and Monem Salam, vice president of Islamic investing at Saturna Capital. Here are their suggestions:

Embrace stocks. While many Muslims share the Saroyas' wariness about investing in stocks, Salam says it is permissible as long as they avoid companies that derive revenue primarily from unacceptable businesses. The easiest way: Invest through a mutual fund that screens companies on the basis of their adherence to Islamic principles. Examples include Amana Growth (AMAGX), managed by Salam's company; Azzad Ethical Mid Cap (ADJEX); and Iman (IMANX). So that Kashif can put these funds in his 401(k), Salam suggests he lobby his employer for a self-directed brokerage account option in the plan.

Kashif likes the approach Salam describes. So does Lori, who says, "Now I feel more comfortable about investing in stocks."

Get the right mix. To be properly diversified, Raghib says, the Saroyas should have some income investments in their portfolio. Since bonds are out of the question, Salam points out two alternatives. One: Islamic mutual funds focused on dividend-paying stocks, such as Amana Income (AMANX) or Azzad Ethical Income (AEIFX). The second is to put a larger amount than usual into cash accounts (see below).

Kashif agrees that it's a good idea to include some investments that offer more stability. If he can't invest through his 401(k), he says he'll open an IRA to do so.

Make savings pay too. Raghib advises the Saroyas to add $150 a month to their liquid savings until they have $20,000 set aside for emergencies. The money should go in a shari'a-compliant savings account, structured as a profit-sharing agreement, which would give them a yield on their money while adhering to the rules against earning interest. One option: a University Islamic Financial Corp. money-market account, recently paying 1%.

Both Lori and Kashif like the idea of the shari'a-compliant account. But Lori rebels against setting aside so much. "I can't imagine having that much in my account and not using it to help other people," she says.

Rethinking a Righteous Aversion to Wealth

Jodi Koeman remembers that when she was young, her parents, though always short on money, tithed to their church faithfully and joyfully. She recalls, "They'd always say, 'First, we're giving to the church. Then we'll figure out the rest.' "

Until recently that's the creed that Jodi, 40, and her husband, Kent, 41, lived by too. The Whitinsville, Mass., couple have built their lives around their Christian faith: Jodi leads the arts program and coordinates social services for their church; Kent teaches Bible studies at a private Christian school. Neither position pays very well. But both spouses felt a certain righteousness in their financial struggles, believing the Bible teaches that wealth can distract one from God. Kent, the son of a pastor, cites Jesus' parable of a rich man who wants to build bigger storehouses to hold his wealth, only to be called a fool by God, who says he will die that very night. "I grew up thinking that wealth was to be avoided," says Kent. "My mistake."

The couple had no single aha! moment or loss of faith — just a growing weariness with the struggle to support themselves and their three children. Even after supplementing their income with second (and third) jobs, they've found it difficult to save for emergencies, much less to invest for key goals like retirement and a college education for the kids. After spending years avoiding wealth and trusting that God would somehow provide, they now suspect they've endangered their family's financial future by not working harder to avoid poverty. Or as Kent half-jokes, "I got sick of being poor."

Certainly he gave it a shot. Married in 1991 (he and Jodi met at a college affiliated with their Christian Reformed Church denomination), he took his first job teaching English at a Christian school in the state of Washington. Starting salary: $14,000 a year. He could have earned more at a public school. But he wouldn't have been able to share his beliefs completely with his students. "It would be like getting almost the whole deck of cards — not quite everything," he says.

When they moved east in 1994 so that Jodi could get a master's in social work, Kent landed the job he still holds at the Whitinsville Christian School. The money wasn't important: Asked in his job interview about his compensation needs, he replied, "Hey, as long as I can pay my bills."

For a while, he could. Though the couple earned less than $50,000 (after getting her degree, Jodi went to work for a social services agency), by 1996 they were able to pay off her college loans. They also put a $10,000 down payment on their current home, one-half of a two-family house.

But over the next several years their income dropped as expenses grew. Jodi quit her job to care for a growing family — Jamison, now 11, Arianna, 10, and Hadley, 6. Their income fell to $30,000, and even paying their basic bills became a struggle. Still, they continued to give to their church, although at less than their traditional rate of 10% of their net income.

The couple worked hard, and their income slowly grew again. At one point, Jodi worked three part-time jobs, including organizing the Sunday service at the fledgling church she and Kent joined in 1997. Kent spent summers painting houses. Jodi's responsibilities and hours grew at church (she's up to 32 a week now).

But the couple didn't really get any breathing room until two years ago, when Kent ditched the paintbrush and took a better-paying second job as a lab technician. The turnaround is dramatic: The couple now make $117,000 a year. They've even started saving, with $8,000 in Kent's retirement plan and $10,000 in the bank.

Finally, they can think more seriously about their financial goals. Jodi plans to start divinity school this year, and she and Kent also want to trade up to a single-family home. They'd like to pay for at least half of the children's college education and semi-retire by the time they turn 60. "We used to feel that if we just did our jobs using the gifts God gave us, we would be taken care of financially," says Kent. Now they know it's up to them to take care of themselves.

What to Do Now

To help the Koemans, Money arranged a meeting with Janice Swenor, a certified financial planner in Westminster, Mass. Her advice:

Set smart priorities. The Koemans' most pressing needs are to beef up their emergency fund and pay for Jodi's divinity school, which will cost at least $16,000 over four years. Currently they put $1,600 a month into the rainy-day fund. Swenor suggests that once the account hits $16,000 (equal to three months' living expenses) they redirect $600 or so a month into a separate savings account for divinity school. One goal that probably won't go as hoped: paying for half the kids' college costs; 30% is more realistic, Swenor says.

Kent and Jodi agree they should give other savings goals precedence over the children's education. "I had to pay for college on my own," says Jodi. "For us to be able to pay any part of tuition for our kids is a positive for me."

Stick tight to a budget. Thanks to Kent's generous pension plan at work, their dream of semi-retiring at 60 is a real possibility. But to seal the deal, they need to step up retirement contributions. To do that, Swenor says, they need to cut spending by $300 a month. One way: Make monthly deposits into a dedicated savings account for expenses like gifts and travel; the amount in the account becomes the hard-and-fast spending limit for those items.

Jodi says they're already living frugally: "How much more can we tighten?" she asks. But a month later, she says they were able to swing it by cutting down on clothing and gifts, and eating out just twice a month.

Price the house right. The Koemans have their eye on a $338,000 home with a garage apartment on the property. They figure they'll end up with no change in housing costs, since the tenant's $700-a-month rent will offset their bigger mortgage payments. But Swenor says they're overlooking increased maintenance costs, plus a weakening rental market; the maximum they should pay, the planner thinks, is $285,000.

Kent and Jodi initially agree. But a few weeks later, they get an offer on their home, so they bid $320,000 on the house they want—and are accepted. "We're increasing our quality of life with the extra space," Kent says. "We'll make it work."

This story originally appeared in the July 2009 issue of Money.