How to Build a $1 Million Retirement Plan

The 401(k) was born in 1981 as an obscure IRS regulation that let workers set aside pretax money to supplement their pensions. More than three decades later, this workplace plan has become America's No. 1 way to save. According to a 2013 Gallup survey, 65% of those earning $75,000 or more expect their 401(k)s, IRAs, and other savings to be a major source of income in retirement. Only 34% say the same for a pension.

Thirty-plus years is also roughly how long you'll prep for retirement (assuming you don't get serious until you've been on the job a few years). So we're finally seeing how the first generation of savers with access to a 401(k) throughout their careers is making out. For an elite few, the answer is "very well." The stock market's recent winning streak has not only pushed the average 401(k) plan balance to a record high, but also boosted the ranks of a new breed of retirement investor: the 401(k) millionaire.

Seven-figure 401(k)s are still rare—less than 1% of today's 52 million 401(k) savers have one, reports the Employee Benefit Research Institute (EBRI)—but growing fast. At Fidelity Investments, one of the largest 401(k) plan providers, the number of million-dollar-plus 401(k)s has more than doubled since 2012, topping 72,000 at the end of 2014. Schwab reports a similar trend. And those tallies don't count the two-career couples whose combined 401(k)s are worth $1 million.

Workers with high salaries have a leg up, for sure. But not all members of the seven-figure club are in because they make big bucks. At Fidelity thousands earning less than $150,000 a year have passed the million-dollar mark. "You don't have to make a million to save a million in your 401(k)," says Meghan Murphy, a director at Fidelity.

You do have to do all the little things right, from setting and sticking to a high savings rate to picking a suitable stock and bond allocation as you go along. To join this exclusive club, you need to study the masters: folks who have made it, as well as savers who are poised to do the same. What you'll learn are these secrets for building a $1 million 401(k).

1) Play the Long Game

Fidelity's crop of 401(k) millionaires have contributed an above-average 14% of their pay to a 401(k) over their careers, and they've been at it for a long time. Most are over 50, with the average age 60.

Those habits are crucial with a 401(k), and here's why: Compounding—earning money on your reinvested earnings as well as on your original savings—is the "secret sauce" to make it to a million. "Compounding gives you a big boost toward the end that can carry you to the finish line," says Catherine Golladay, head of Schwab's 401(k) participant services. And with a 401(k), you pay no taxes on your investment income until you make withdrawals, putting even more money to work.

You can save $18,000 in a 401(k) in 2015; $24,000 if you're 50 or older. While generous, those caps make playing catch-up tough to do in a plan alone. You need years of steady saving to build up the kind of balance that will get a big boost from compounding in the home stretch.

Here's how to do it:

Make time your ally. Someone who earns $50,000 a year at age 30, gets 2% raises, and puts away 14% of pay on average will have $547,000 by age 55—a hefty sum that with continued contributions will double to $1.1 million by 65, assuming 6% annualized returns. Do the same starting at age 35, and you'll reach $812,000 at 65.

Yet saving aggressively from the get-go is a tall order. You may need several years to get your savings rate up to the max. Stick with it. Increase your contribution rate with every raise. And picking up part-time or freelance work and earmarking the money for retirement can push you over the top.

Milk your employer. For Fidelity 401(k) millionaires, employer matches accounted for a third of total plan contributions. You should squirrel away as much of the boss's cash as you can.

According to HR association WorldatWork, at a third of companies 50% of workers don't contribute enough to the company 401(k) plans to get the full match. That's a missed opportunity to collect free money. A full 80% of 401(k) plans offer a match, most commonly 50¢ for each $1 you contribute, up to 6% of your salary, but dollar-for-dollar matches are a close second.

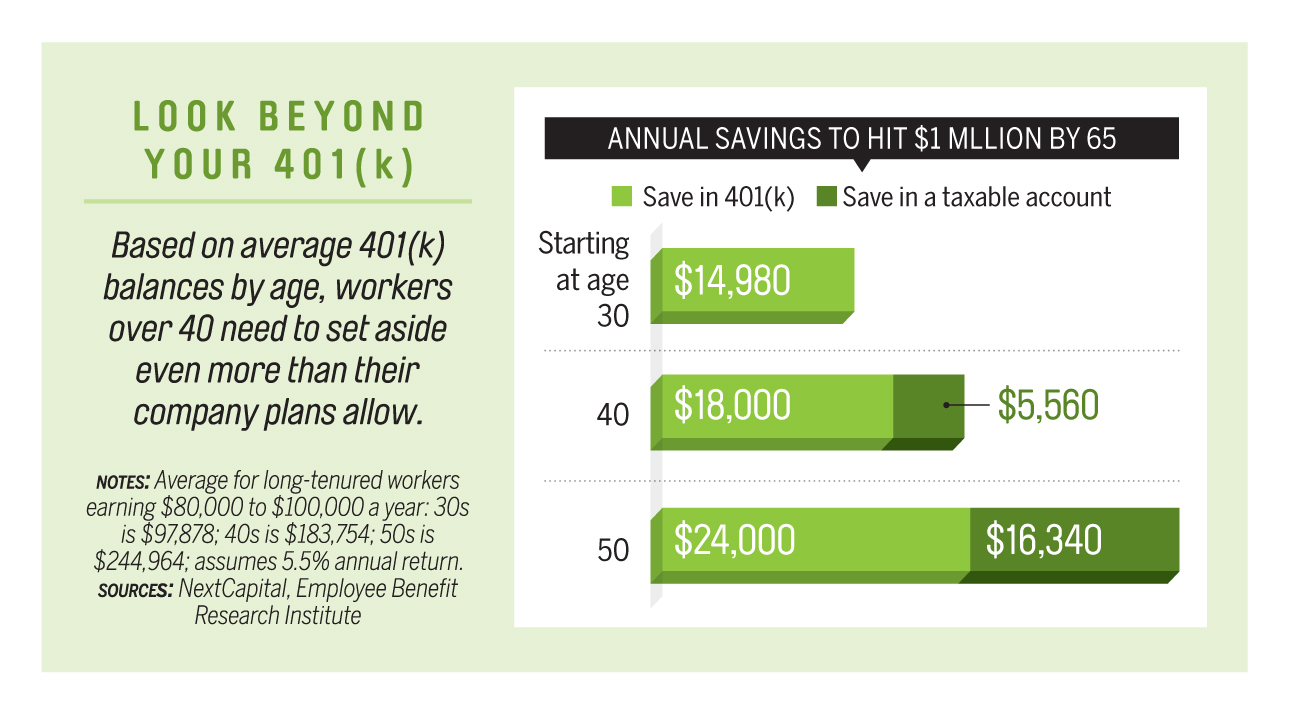

Broaden your horizons. As the graphic below shows, power-saving in your forties or fifties may bump you up against your 401(k)'s annual limits. "If you get a late start, in order to hit the $1 million mark, you will need to contribute extra savings into a brokerage account," says Dirk Quayle, president of NextCapital, which provides portfolio-management software to 401(k) plans.

2) Act Like a Company Lifer

The Fidelity 401(k) millionaires have spent an average of 34 years with the same employer. That kind of staying power is nearly unheard-of these days. The average job tenure with the same employer is five years, according to the Bureau of Labor Statistics. Only half of workers over age 55 have logged 10 or more years with the same company. But even if you can't spend your career at one place—and job switching is often the best way to boost your pay—you can mimic the ways steady employment builds up your retirement plan.

Here's how to do it:

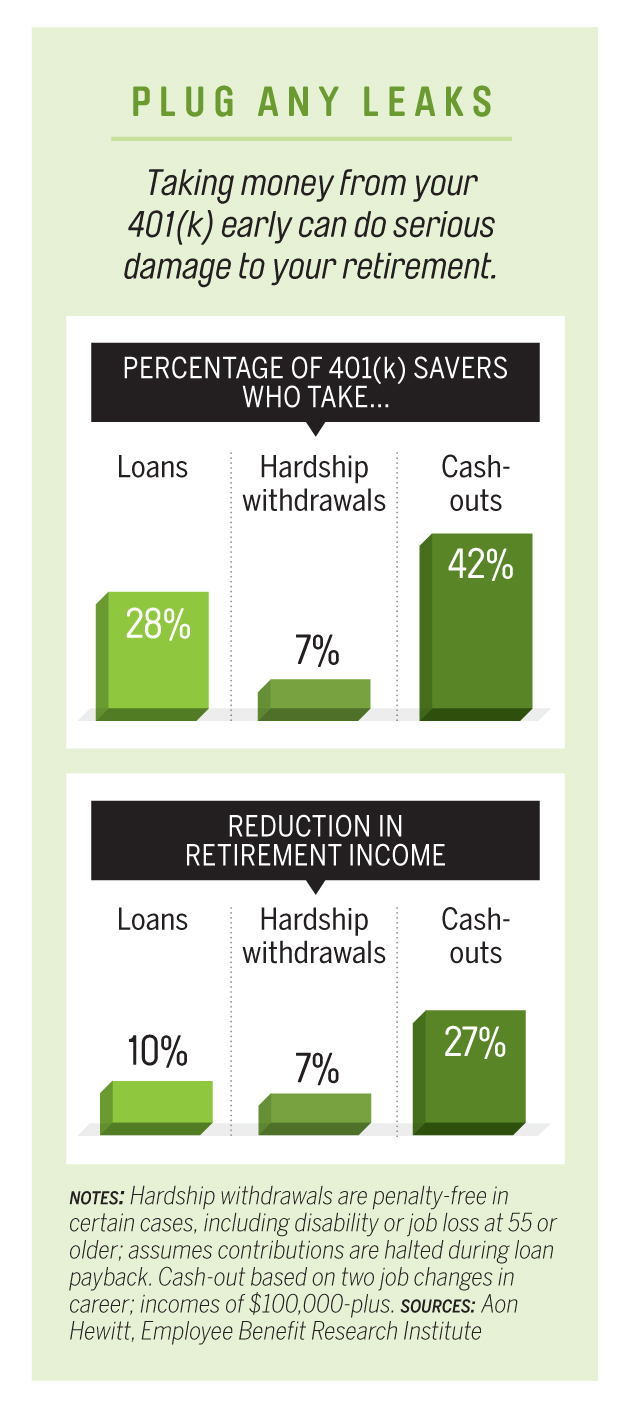

Consider your 401(k) untouchable. A fifth of 401(k) savers borrowed against their plan in 2013, according to EBRI. It's tempting to tap your 401(k) for a big-ticket expense, such as buying a home. Trouble is, you may shortchange your future. According to a Fidelity survey, five years after taking a loan, 40% of 401(k) borrowers were saving less; 15% had stopped altogether. "There are no do-overs in retirement," says Donna Nadler, a certified financial planner at Capital Management Group in New York.

Even worse is cashing out your 401(k) when you leave your job; that triggers income taxes as well as a 10% penalty if you're under age 59½. A survey by benefits consultant Aon Hewitt found that 42% of workers who left their jobs in 2011 took their 401(k) in cash. Young workers were even more likely to do so. As you can see in the graphic below, siphoning off a chunk of your savings shaves off years of growth. "If you pocket the money, it means starting your retirement saving all over again," says Nadler.

Resist the urge to borrow and roll your old plan into your new 401(k) or an IRA when you switch jobs. Or let inertia work in your favor. As long as your 401(k) is worth $5,000 or more, you can leave it behind at your old plan.

Fill in the gaps. Another problem with switching jobs is that you may have to wait to get into the 401(k). Waiting periods have shrunk: Today two-thirds of plans allow you to enroll in a 401(k) on day one, up from 57% five years ago, according to the Plan Sponsor Council of America. Still, the rest make you cool your heels for three months to a year. Meanwhile, 40% of plans require you to be on the job six months or more before you get matching contributions.

When you face a gap, keep saving, either in a taxable account or in a traditional or Roth IRA (if you qualify). Also, keep in mind that more than 60% of plans don't allow you to keep the company match until you've been on the job for a specific number of years, typically three to five. If you're close to vesting, sticking around can add thousands to your retirement savings.

Put a price on your benefits. A generous 401(k) match and friendly vesting can be a lucrative part of your compensation. The match added about $4,600 a year to Fidelity's 401(k) millionaire accounts. All else being equal, seek out a generous retirement plan when you're looking for a new job. In the absence of one, negotiate higher pay to make up for the missing match. If you face a long waiting period, ask for a signing bonus.

3) Keep Faith in Stocks

Research into millionaires by the Spectrem Group finds a greater willingness to take reasonable risks in stocks. True to form, Fidelity's supersavers have 75% of their assets in stocks on average, vs. 66% for the typical 401(k) saver. That hefty equity stake has helped 401(k) millionaires hit seven figures, especially during the bull market that began in 2009.

What's right for you will depend in part on your risk tolerance and what else you own outside your 401(k) plan. What's more, you may not get the recent bull market turbo-boost that today's 401(k) millionaires enjoyed. With rising interest rates expected to weigh on financial markets, analysts are projecting single-digit stock gains over the next decade. Still, those returns should beat what you'll get from bonds and cash. And that commitment to stocks is crucial for making it to the million-dollar mark.