14 Simple Ways to Be a Smarter (and Richer) Investor

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

1. Don’t pay 33% of your money in fees. Mutual fund charges look small, but the cost of paying an extra 1% a year in fees is that you give up 33% of your potential wealth over the course of 40 years. An index fund like Schwab Total Stock Market can keep your expenses below 0.1%, compared with over 1% for many stock funds.

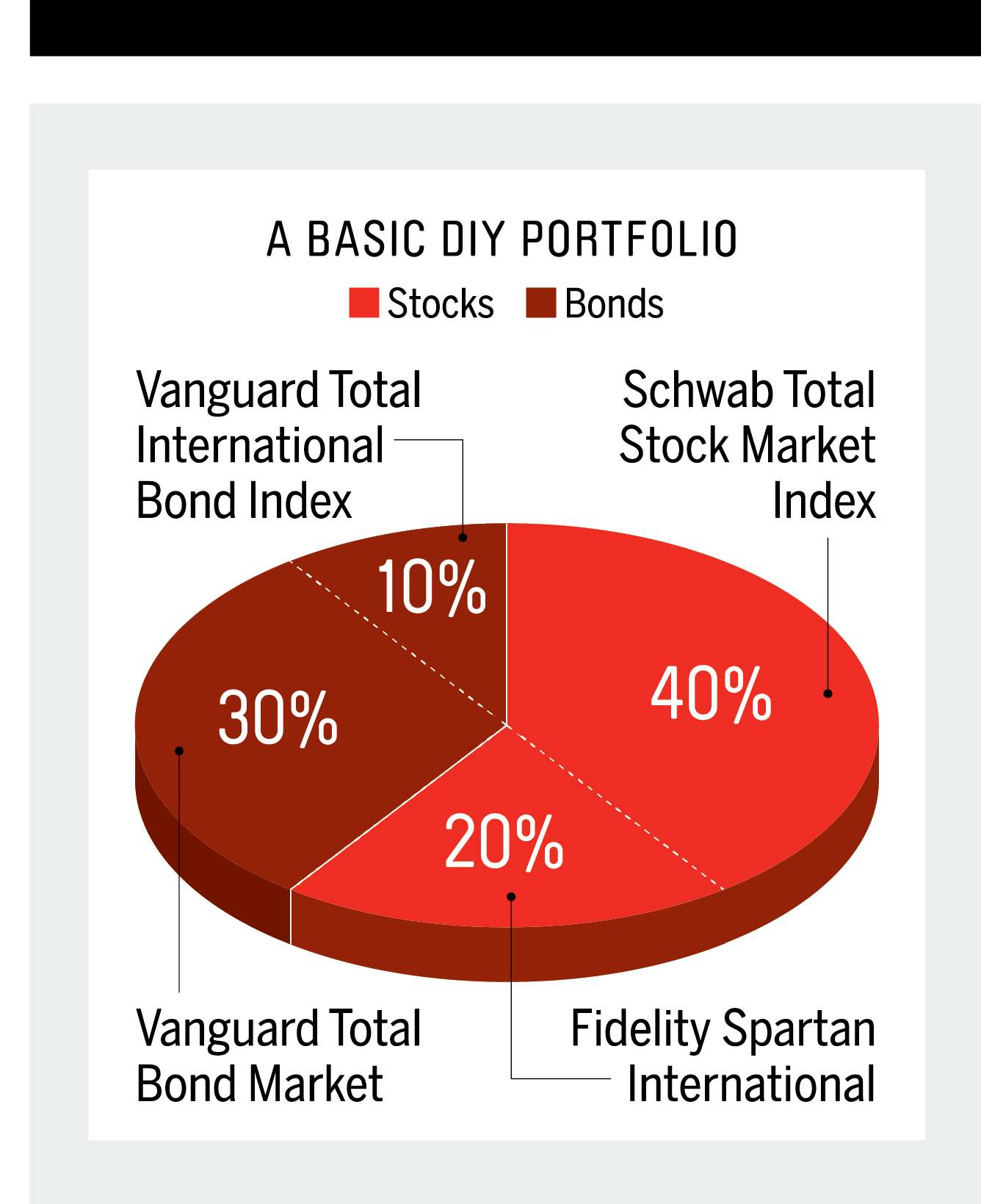

2. Mix your own simple plan. Four very low-cost index funds, recommended in the Money 50, deliver all the world’s major markets. (See graphic below.) The more aggressive you are, the more you can tilt toward stocks.

3. Or pick just one fund. You don’t have to be fancy to be an effective investor. A classic balanced mix (about 60% stocks/40% bonds) provides plenty of equities’ upside, with less pain during crashes. The Vanguard Wellington balanced fund has earned an annualized 8% over a decade.

4. Or hire a robo-adviser. Outside of a 401(k), if you want a plan that’s more tailored to you, web-based automated investment services can put you in a mix of low-cost index funds and then rebalance as you go. Betterment and Wealthfront stand out as low-cost options, charging 0.35% of assets or less.

5. Patch the holes in a 401(k). Many workplace plans offer at least an S&P 500 or total stock market index fund as a low cost option for buying U.S. stocks. But if your plan doesn’t offer good choices in other asset classes, such as bonds and foreign stocks, diversify elsewhere. Save enough to get the company match. Then fund an IRA, where you can choose which bond funds or foreign funds to go with.

6. While you’re at it, dump company stock. About $1 out of every $7 in 401(k)s is invested in employer shares. But your income is already tied to that company. Your retirement shouldn’t be too.

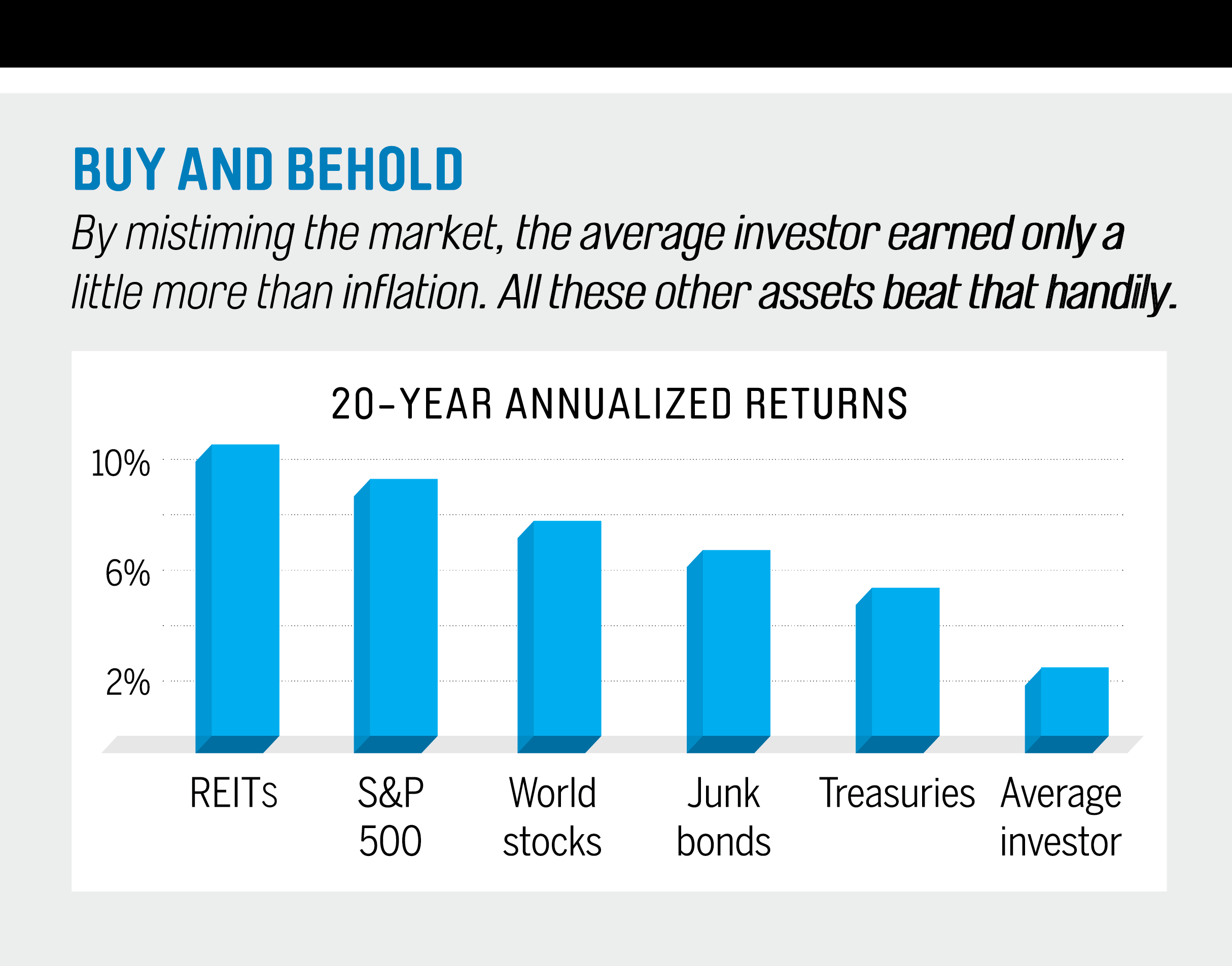

7. Pick an asset, any asset. You can get into trouble by being too clever by half. The average investor has barely beaten inflation in the past 20 years as a result of buying trendy assets high and selling low. Forget all that. As the chart below shows, you’re better off buying and holding almost any major asset class.

8. Be patient with funds. Some well-known bargain-minded funds, such as Dodge & Cox Stock , have struggled this past year. That doesn’t mean you should flee. True value funds refuse to buy popular—read expensive—stocks, so they often lag in frothy times. But over the past 15 years, Dodge & Cox has outperformed its peers by 2.5 percentage points a year and the S&P by more than four points.

9. Be stingy with funds. Cheapskates know index funds aren’t their only options. Actively managed blue-chip stock funds with an expense ratio of 0.35% or less have returned 8.5% over the past decade. That’s 0.5 percentage point better annually than the S&P 500. A great option: Vanguard Equity-Income , charging 0.29%, has outpaced the market’s gains by 3.5 points annually over the past 15 years.

10. Rebalance? Maybe not. Routinely resetting your stocks and bonds to their original levels “is a nice idea in theory,” says planner Phil Cook. But “if you rebalance too often, you can give up a lot of potential returns.” In your twenties and thirties, when you’re almost all in stocks, you can skip it. As you age, though, gradually increase the frequency of rebalancing to every few years.

11. Break up with your high-cost adviser. Stock and bond returns are expected to be muted in the coming decade, so cutting advisory fees—often 1% of assets—matters. Vanguard Personal Advisor Services charges just 0.3% of assets. Some tech-based services, such as Betterment and Wealthfront, charge even less.

12. Put your portfolios together... If you hold a third of your 401(k) in bonds, your mix may be riskier than you think if your spouse is 100% in stocks. Coordinating also improves your options. If your spouse’s plan has a better foreign fund, focus your international allocation there.

13. ...and your assets in the right place. Once you’ve maxed out your IRAs and 401(k)s, use taxable accounts for the most tax-efficient investments in your mix. They include index and buy-and-hold equity funds that trade infrequently and generate few capital gains distributions.

14. Take a fresh look at a classic. You’ve now built up enough assets that advisers will be eager to sell you clever ideas to beat the market. Before you bite, read the 2015 edition of A Random Walk Down Wall Street. Burton Malkiel has updated his skeptical investment guide to take on the latest new flavor, “smart” ETFs. If a fund has a greater return, says Malkiel, it’s probably because it’s taking on more risk.

Adapted from “101 Ways to Build Wealth,” by Daniel Bortz, Kara Brandeisky, Paul J. Lim, and Taylor Tepper, which originally appeared in the May 2015 issue of Money magazine.