Do You Really Need a Long-Term Care Plan?

Millions of boomers are wondering how to prepare for the possibility of needing costly care some day. Count me as one of them. At age 58, I am in the sweet spot for buying long-term care insurance—assuming I want it at all. After weeks of research, I still haven’t decided. But I have sorted out the moving parts.

What I’ve found is that the rising cost of both care and the insurance that pays for it is only one piece of the puzzle. New types of insurance give me more options to mull over. And recent research calls into question how common lengthy nursing-home stays really are, leaving me to think harder about the odds of needing coverage.

What’s more, I have to be concerned about the health of an industry that I would need to rely on for the next three decades. Insurers badly miscalculated how many policyholders would make claims, leading to a mass exodus of big players from the business in recent years.

The upshot: drastic price hikes from the insurers who remain. A typical long-term-care policy written 10 years ago has seen annual premiums rise about 70%, says Michael Kitces, director of research at Pinnacle Advisory Group. Even so, those old policies are cheaper by half than what a person nearing 70 has to pay for the same coverage today.

That’s because the insurers that have stayed in the business have jacked up the price of new policies. Those premiums rose an average of 8.6% last year alone, reports the American Association for Long-Term Care Insurance. For some, the price hikes are even worse. Today, for example, a healthy 55-year-old man would pay $2,075 a year for comprehensive single coverage—up 17% from last year.

All in all, the answer to the question Do you need long-term-care insurance? is a personal one—and far from easy. Here's how to think through the decision.

The Promise of Insurance

Long-term care is something you hope you never need. Or at least you hope that when and if you aren't entirely self-sufficient, your spouse or another family member can pitch in. But when you need more of a hand with daily activities than a lay helper can provide, or around-the-clock or more expert medical care becomes a must, you'll have to pay for a professional.

The national average for a shared room in a nursing home is $77,380 a year, according to the Genworth 2014 Cost of Care Survey, but the tab can go much higher—$120,000 is typical in Massachusetts, for example. Even assisted living, where you get just some one-on-one help and basic medical care, averages $42,000 a year.

Medicare covers 100 days in a nursing home if you are recovering from an illness or injury and showing improvement, but it offers no help at assisted living or in your home. Medicaid picks up the tab for a nursing home and some in-home help only after you have all but exhausted your savings (in some states, the program helps with assisted living too).

Enter long-term-care insurance, which reimburses you for at least a portion of the cost of a nursing home, assisted-living facility, adult day care, or in-home help. To qualify for benefits, you must be unable to perform two of these six day-to-day activities—bathing, dressing, moving from bed to chair, using the toilet, eating, and maintaining continence—and a medical pro must expect your disability to last at least 90 days.

How to Decide If You're a Candidate

You may figure you'll roll the dice and fund your care out of savings. In fact, sales of long-term-care policies fell by 24% in 2014 and are down 65% from 2004 levels, reports LIMRA, an insurance industry trade group. Just 13% of people 65 and older have a policy, according to estimates by Anthony Webb, a senior economist at the Center for Retirement Research at Boston College. Here's how to make the call.

Start with what you're worth. The rule of thumb is that you're a candidate to buy long-term-care insurance if you have between $200,000 and $2 million in assets. With less, you can't swing the premiums and don't have enough to protect. Medicaid will cover most of the costs of care after you whittle your savings down to as little as $2,000 if you're single. With $2 million, you can reasonably plan on paying your own way. But even in that doughnut hole, the answer isn't always clear.

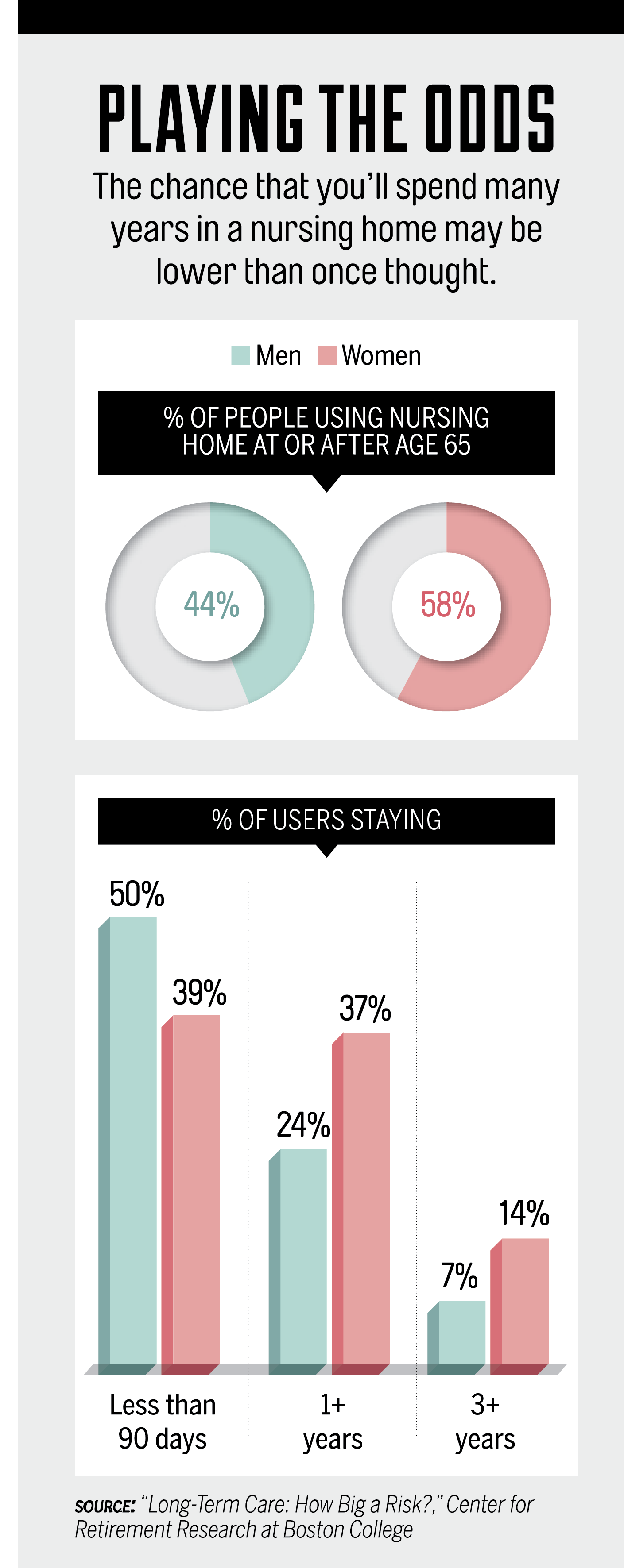

Understand the true odds. You may have heard figures that make rolling the dice seem like a foolish bet. One frequently cited stat is that 70% of Americans who reach 65 will eventually need some sort of long-term care.

But a recent paper from the Center for Retirement Research paints a less alarming picture. As the graphic below shows, a high number of people will need nursing-home care at or after 65, but only a small portion will remain long enough to run up big bills. Half of men and 39% of women stay less than 90 days, before most long-term-care policies even kick in. The average stay for a man is less than a year; for a woman, a year and a half.

Previous studies had estimated that a long-term-care policy made financial sense for 30% to 40% of 65-year-olds. The CRR pegged that number around 20%. "We're getting more people going into care for a shorter period of time," says Webb. "That's what's driving down the value of insurance."

Ask yourself what you're insuring. At its root, long-term-care insurance is about protecting your estate. A desire to preserve a legacy for their three adult children is why Craig and Jan Klaas, both 60, bought a soup-to-nuts policy. Last year Jan's mother died after eight years in a facility. Her father had spent two years in a nursing home. "I've seen people get wiped out," says Craig, a financial planner in Rockford, Ill. "I do not want my estate at risk."

Without coverage, you'll still get care, funded by savings and Medicaid, if needed. But paying for it could deny your children an inheritance.

See if you even have a choice. Insurers have stepped up medical screening. Overall, 30% to 40% of applicants are turned down for health reasons, says Jesse Slome, director of the American Association for Long-Term Care. Your chances are better when you're younger. Still, 17% of 50- to 59-year-olds are disqualified, up from 14% in 2009. Common reasons include chronic health problems like diabetes and arthritis, or any condition that can leave you incapacitated. A denial from one insurer, adds Slome, will often lead to automatic denials from others.

Check your family tree. It's not just your health that counts. Since last year, Genworth has also been considering your parents' health when you apply for a policy. With early-onset dementia or coronary artery disease in the family, you might not qualify for the best rate.

You should take your family history into consideration too. Half of all claims are triggered by care associated with dementia. On the other hand, says Howard Gleckman, senior fellow at the Urban Institute, a history of cancer may argue for less or no coverage because patients usually have a decent quality of life until just a few months from the end. That's a cold calculation, but one you shouldn't ignore.

Next: If you're ready to explore your options, here's how to keep down the costs of long-term-care insurance.