Don’t Ditch Emerging Markets Just Because They’re Down

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

When the markets took a nosedive last week in reaction to China’s bubble continuing to deflate, emerging markets dove hardest of all. The MSCI Emerging Markets Index tumbled twice as much as the S&P 500 index before recovering.

We don’t have last week’s mutual fund outflow data quite yet, but if the typical pattern plays out, I would guess that some investors freaked out and sold funds invested in emerging markets, especially in Asia. Only the previous week, worries about China triggered the largest withdrawals from emerging markets in more than seven years, according to EPFR Global.

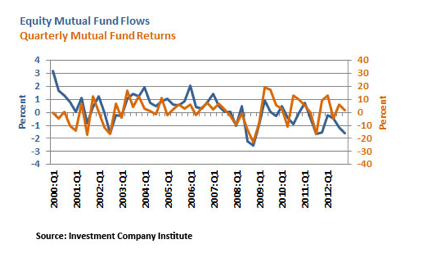

I was both heartened and saddened by these developments—heartened because I had recently reallocated a larger portion of my 401(k) contributions to a developing markets fund that has been down -14.54% in the last year, and saddened because I knew some people would likely be doing the opposite and reducing their emerging markets exposure, likely at a loss. Selling when things turn bad is the corollary to buying a fund when it is flying high and part of an overall pattern of chasing returns that economist Yili Chien of the Federal Reserve Bank of St. Louis charted last year using data from the Investment Company Institute for the period 2000-2012:

As you can see, when returns are high, flows into equity mutual funds rise, and when returns decline, flows follow suit. Wall Street types usually attribute chasing returns to the old “greed and fear” problem, but I think something else is going on cognitively whereby we misconceptualize equity funds in terms of winners and losers instead of whether the underlying investments are cheap or overpriced. We buy “winners” and we sell “losers”—which is of course the opposite of buying low and selling high. And when a fund performs poorly we all of a sudden perceive it as risky and want to get rid of it when in fact the underlying equities were a lot riskier when they were more expensive. The tendency to act on these misconceptions can be quite damaging to your investments—and your retirement planning.

Yes, emerging markets could go lower from here. Volatility will always be a part of investing in countries that grow not in a nice upward slope as we might wish but in fits and starts and reversals. As such, most advisers recommend they remain a minority portion of your portfolio.

But volatility in and of itself does not present a risk if you have a reasonably long time horizon (say, at least 3 to 5 years) and if you don’t sell in a panic. When performance is down, it’s important to remember the reason an emerging market fund was in your portfolio in the first place—the opportunity for growth over the long term as well as geographic diversification. I have no idea where emerging markets are going to go in the next week, month, or year, but I still believe that the economies of developing countries, whether through infrastructure or consumer consumption, have enormous potential for growth. Nothing that has happened in the last couple of weeks changes that story.

Konigsberg is the author of The Truth About Grief, a contributor to the anthology Money Changes Everything, and a director at Arden Asset Management. The views expressed are solely her own.