From the Money Archive: Scenes From the Housing Bubble

*Note: this article, by Stephen Gandel and Amanda Gengler with Paul Keegan, originally appeared in the May 2007 issue of Money magazine.

Newlyweds Erik and Brandi Quam can't really afford their home. The monthly carrying costs on their two-bedroom condo in Arlington, Va. run about $2,500 a month, and they fear the bill could go higher still as their adjustable mortgage resets to higher interest rates. It's already a tight squeeze: They've taken in a roommate to help pay the bills. Unfortunately, they can't afford to sell either. Thanks to a falling housing market and a prepayment penalty of about $11,500, they'd owe the bank more than their place is worth. "It makes me want to cry every month," says Brandi, 26. The irony is that the Quams should be able to afford their place: It cost just $219,000 when a still-single Brandi, fresh out of the Air Force, bought it.

So how did they get themselves in such a mess? More puzzling still, why did lenders let them—along with millions of other homeowners, many of whom, unlike the Quams, are in immediate danger of foreclosure?

In the answer to that question lies the real story behind the once dizzying, now fizzling housing boom. Sure, record-low interest rates, boomers buying vacation homes and immigrants grabbing for the American dream all did their bit to push up prices. But what really supercharged the market was the mortgage industrial complex—a machine with cogs called brokers and bankers, fueled by money poured in by investment banks, bond traders and hedge fund managers. The system prospered and grew, introducing new players into the financing transaction and transforming the roles of others. Finally it ran amok, creating huge incentives at every level of a home sale or a refi to sacrifice prudence in pursuit of a killing. Market checks and balances should have prevented the process from getting out of control. But they were corrupted, co-opted or simply steamrollered. For example:

- The lending officer of old, who often worked for a bank that underwrote the loan, was replaced by the mortgage broker. Loosely regulated and employed by a company with little or none of its own capital at stake, brokers are salespeople rewarded for steering as many prospective homeowners or refinancers as possible into the most profitable loans.

- Appraisers, who are supposed to be the independent gatekeepers of the mortgage system, increasingly caved in to pressure to approve any deal a broker or loan officer wanted to make.

- Lenders, in turn, had less and less reason to care whether the borrowers could repay. No longer did a bank have to hold a loan itself or sell it into a secondary market of cautious investors. In the super-low-interest-rate environment of recent years, Wall Street would buy just about any loan, however risky, to gain a little extra yield. To meet demand, lenders spun out a crazy profusion of mortgages that would allow more borrowers to qualify for ever-larger amounts. If a borrower might not really be able to afford the payments...well, the lender had already sold the loan off. "The mortgage market for the past few years has been playing a massive game of hot potato," says Drexel University finance professor Joseph Mason.

- Borrowers, to the extent that they understood what they were getting into, also played along. In a market that kept rising, getting your dream house seemed to make sense. A broker could find you a loan with monthly payments you could handle—at least at first. And soon enough you'd sell and pocket a big gain.

Too much money. Too little restraint. This is the story of how all the important players in the market decided that they had too much at stake to shout, "Stop!" We've been here before: Remember when Wall Street analysts told us Amazon.com was worth $400 a share? And as with the tech bubble, it may not be only speculators who get hurt. As home prices unwind from unsustainable highs, we may all feel at least a little bit poorer. That could be a drag on the economy. It's already a real drag for the Quams.

The Quams and the too-good-to-be-true mortgage

The primary mortgage on the Quams' condo was fixed at 5.25%. But Brandi had also taken out a smaller variable-rate loan. As rates rose in 2005, she went looking for a better deal and entered her contact information into a few websites. Shortly thereafter, she says, she got a call from broker Robert Hoover of CPA Mortgage in Maryland. He found her a new loan with what she says she understood to be an initial 1% rate, with only small increases in the first five years. And since she had equity (her condo had appreciated), she could even take a little cash out to pay off some bills. The transaction earned the broker and his firm about $12,600.

It took a few months before Brandi realized what she had done. The mortgage was something called an option ARM. It was true that Brandi could make initial minimum payments of about $800. But those weren't enough to cover the interest she was actually being charged, which was higher than the rate used to calculate required payments. The unpaid interest was added to the loan balance, a phenomenon called negative amortization. The Quams have decided to start paying at least the interest on the loan, but even so, the balance has grown by $7,000. Barring a market turnaround, they're stuck for at least another year and a half until the prepayment penalty phases out. They've had to turn down job offers because they can't move.

Who is to blame here? Yes, Brandi should have asked more questions and scrutinized the fine print. The idea of a mortgage with a 1% rate seems, on its face, too good to be true. Brandi says she did know she'd eventually have to make higher payments, but she planned to move before that happened. Exactly how Hoover described the mechanics of the loan, or what she thought he meant, is impossible to know for sure now. Hoover declined to speak with Money, and his firm sent an e-mail saying that it couldn't comment on a client but that "ultimately, it is the consumer that makes the choice they feel is best."

But based on the documents Brandi showed us for her loan—and documents Money has seen for other option ARMS—it is easy to see how a person could be confused. A payment schedule is shown on the federally mandated truth-in-lending form, but it is based on minimum payments and a steady interest rate, rather than the variable rate the Quams are charged. An "adjustable-rate note" first says the Quams will be charged a yearly rate of 1%. The next subsection says that rate "may" change almost immediately. The first payment coupons show only the minimum, negatively amortizing payment.

A spokeswoman for the original lender, BankUnited of Miami Lakes, Fla., said she couldn't specifically comment on Brandi's loan. But she said that borrowers aren't approved unless their "credit score will support the fully indexed rate." All borrowers, she added, acknowledge receipt of numerous documents disclosing every aspect of the loan, including a four-page form that describes the terms "in plain English" and warns borrowers of the possibility of negative amortization.

Keep in mind, complex loans like option ARMs are new to most people, and they are radically different from 15- and 30-year fixed-rate loans. Consumer advocates say that the truth-in-lending disclosure rules are outdated and that borrowers like the Quams are being asked to climb a steep learning curve—with their homes at stake. "The disclosures on adjustable-rate mortgages have never been any good, and option ARMs are particularly terrible," says Jack Guttentag, professor emeritus of finance at the University of Pennsylvania's Wharton School.

In any case, the loans are popular. In the first half of 2006, option ARMs were 15% of mortgage originations, reports the Mortgage Bankers Association. In theory, the loan can be a useful tool for people with irregular income, such as entrepreneurs. But low payments are the rule, not the exception. Today more than 80% of borrowers in securitized option ARMs pay less than their interest charges, according to Fitch Ratings. Their loan balances are rising. That might not be so bad in a rising market, but it's potentially a disaster in a falling one.

It's obvious that a lot of homeowners could have used better advice about how to find an affordable loan. But good advice has gotten harder to come by in the mortgage game. That's because the person across the desk or on the other end of the telephone getting you a mortgage probably doesn't work for the bank that's putting up the money. He may not care if you can pay. "Consumers thought that when they qualified for a loan, that meant they had a reasonable prospect to repay the loan unless some type of illness or catastrophe hit the family," says Michael Calhoun, president of the Center for Responsible Lending. "That is no longer the case."

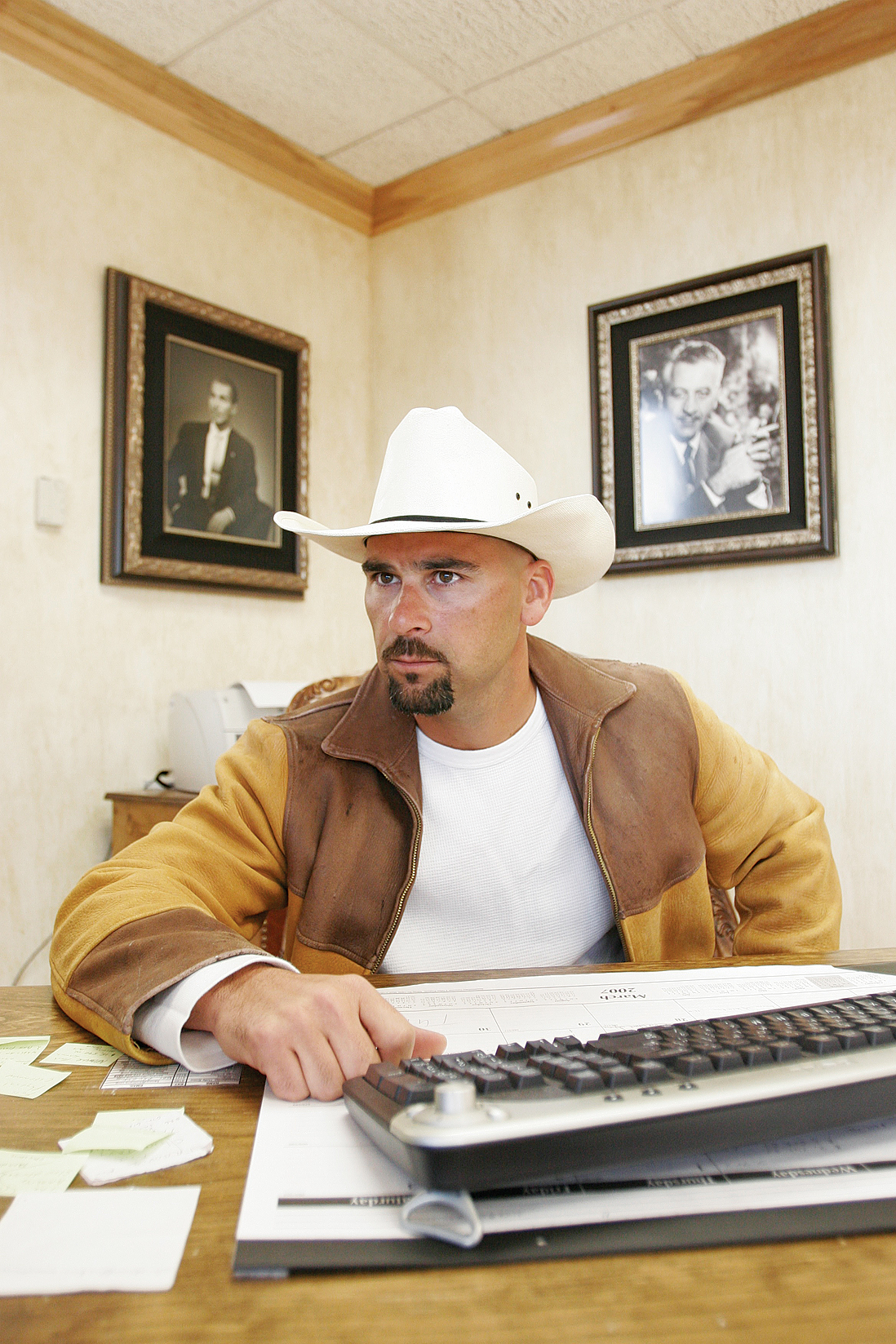

Would you get your mortgage from this man?

Morning commuters in Boston, Chicago and Phoenix are slapped awake by the voice of a pugnacious Texan shouting out of the radio. "When your mortgage payment goes up 400 bucks a month, you can dislocate your jaw and swallow it like a snake eatin' an egg," the voice says. "Or spend another seven grand and have some predator redo your mortgage. Unacceptable." The voice belongs to Jon Shibley, 39, the president of Lenox Financial Mortgage. Over 13 years he's built his business from a one-man shop in Atlanta into a 200-employee company that arranges mortgages and refinancings in 24 states.

Up until the 1980s, when the savings-and-loan crisis brought the old system crashing down, getting a mortgage typically meant sitting down with a loan officer from a local lender, which cared a lot about your ability to pay. Today about 70% of mortgages are originated by a mortgage broker. It's an intense, fast-moving business and suits the hypercharged Shibley just fine. Shibley meditates 20 minutes a day but also claims that he will occasionally burn himself or immerse his body in ice water—"a shock to the system," he calls it, that keeps him engaged. Shibley doesn't rely on word-of-mouth or community roots. He drives his business with in-your-face advertising. These days, as his commercials show, his sales targets include borrowers looking to escape onerous payment hikes on their variable-rate mortgages. "People don't know who to call," he says. "That's why my marketing philosophy has been so successful."

For better and for worse, the new mortgage sales machine made it much easier to get a loan. And if a mortgage option was mathematically possible, a broker made sure you knew about it. He or she could get you a low annual rate, help you avoid a down payment or find you a super-low initial monthly payment. Shibley's particular pitch is "no closing costs," which looks to be an easy sell to borrowers suddenly short on cash. "This industry is a disaster," he says. All these mortgage options can make sense in certain circumstances and hurt you in others. (You may actually prefer to pay closing costs, for example, if that gets you a lower rate and you plan to stay in the loan long enough to work off the costs.) The tricky part is figuring out which loan works for you.

A good mortgage broker can help you do that, and Shibley says that's what his people do. But not all brokers will. Brokers can be paid more if they can convince you to pay a higher rate than you qualify for, or borrow more money than you need. And they resist efforts by lawmakers to give them a fiduciary obligation to act in the borrower's best interest. "We do not solely represent the consumer," says George Hanzimanolis, president-elect of the National Association of Mortgage Brokers.

In short, it's best to shop around—and it's easy enough to do that on a basic fixed-rate mortgage. It's a lot harder to comparison-shop loans with payment options and variable rates, which is why brokers love to sell them. With option ARMs, borrowers tend to focus on the introductory rate and minimum payment, and to ignore the higher rate down the road. For the broker that higher rate could mean the difference between a $3,000 commission and one several times as large. "Option ARMs are not a license to steal, but once a customer asks for it, I know I'm going to make four times as much," says Jim Moore, a Grand Rapids broker who writes about his business at miamibeach411.com, speaking by cell phone. "It's what puts me down here at Best Buy buying a 40-inch flat screen."

Even then there are usually limits to how much your broker can get out of you. After all, a mortgage is based on the value of your house. But maybe there's a way around that too.

Price estimates made to order

Last summer Daniel Kim was feeling pinched. So when Kim, now 27, of San Leandro, Calif. got a call from a mortgage company, he was intrigued. The loan officer, Mia Yi of ALG Capital, sold Kim on refinancing, putting him an additional $81,000 in debt on his house. Kim says he was surprised he could borrow more. He had bought the two-bedroom the previous year for $560,000 with no money down, and everything he had read said the market in his area was cooling. But after Yi produced an appraisal in November that said his house was worth $642,000, Kim signed. "I was excited," he says, "that my house had appreciated that much."

Appraising the value of a house has never been an exact science. But the $4-billion-a-year appraisal industry provides a crucial reality check for the system. Banks need an appraisal to make a loan. Regulators and mortgage investors require it to insure against fraud. Consumers rely on appraisals to give them some measure of confidence they aren't paying too much. In refinancings, the appraisal is the only thing that tells a consumer what a house is worth and how much he can borrow.

So perhaps it's not surprising that appraisers have come under pressure from some of the people selling mortgages. Money has obtained more than 100 e-mails and faxes sent by loan officers to appraisers across the country. The language varies from asking if a predetermined value was possible to promising more business if a number could be hit. "Many homeowners are finding out that the equity they were led to believe they had in their house is not actually there," says John Taylor, president of the National Community Reinvestment Coalition.

According to an appraiser Money hired, Kim's house is worth only $580,000 and was at the time he refinanced the house. Yes, different appraisers often have different takes. In Kim's case the appraisers disagree about whether an enclosed porch counts as part of the total square footage. But ALG's Yi strongly suggested to appraisers what the answer ought to be. In an e-mail she sent to numerous appraisers, Yi said she needed "a value of $650,000 or more. Please let me know ASAP with max value." Five days later Paul Chasteen, an appraiser in Discovery Bay, produced the appraisal that led to Kim's $642,000 mortgage, less than Yi wanted but enough to do a deal. ALG got him loans for the full appraised value. The result: Kim now owes $62,000 more than his house may be worth. Kim put the money from the refinancing into a dry-cleaning business and paying off a car loan. He can't move without foreclosing. "It's not a good feeling," he says.

Yi declined to comment. ALG owner Crystal Palomino said two appraisers (from the same firm) reviewed the value, as did the funding bank. Chasteen says he and his fellow appraisers are under the gun because as many as 10 competitors may get the same order. Referring to that pressure, Chasteen says, "Is there a problem out there? You bet there is." He adds, though, that he resists and that in Kim's case pressure wasn't an issue. "I never push values," he says.

Appraiser Ray Miller of Lyndon Station, Wis. also says he doesn't inflate values but complains that he is asked to do so daily. Miller says he doesn't always give the preferred answer, which hurts business. "If I don't hit the number they are asking for, I almost never hear from that loan officer again," he says. "But if you don't accept these orders at all, you won't have any business."

Brokers sometimes ask for a "comp check." They don't ask for a target price, but get a number of appraisers to guess what a property is worth, sight unseen, before ordering. "Appraisers who do comp checks know that they have to inflate values to get the order and get paid," says Pamela Crowley, a former appraiser who recently launched a site to catalogue lending abuses, MortgageFraudWatchList.org.

Hanzimanolis of NAMB says appraisal pressure isn't a big problem. His organization amended its code of ethics last year to prohibit members from squeezing appraisers. "I don't see how anybody but the appraiser is responsible for an inflated or fraudulent appraisal," he says.

A number of states, including Colorado, are mulling laws that would make it clearly illegal to pressure appraisers. Jonathan Miller (no relation to Ray), owner of New York City's Miller Samuel and one of the nation's most prominent appraisers, argues that such laws are sorely needed. "Under the current system," he says, "there is really no point to a mortgage appraisal anymore." You might expect that those ultimately on the hook if a borrower fails to pay would take an interest in making sure that the collateral was really worth its appraised value. But until the past few months, you'd have been wrong.

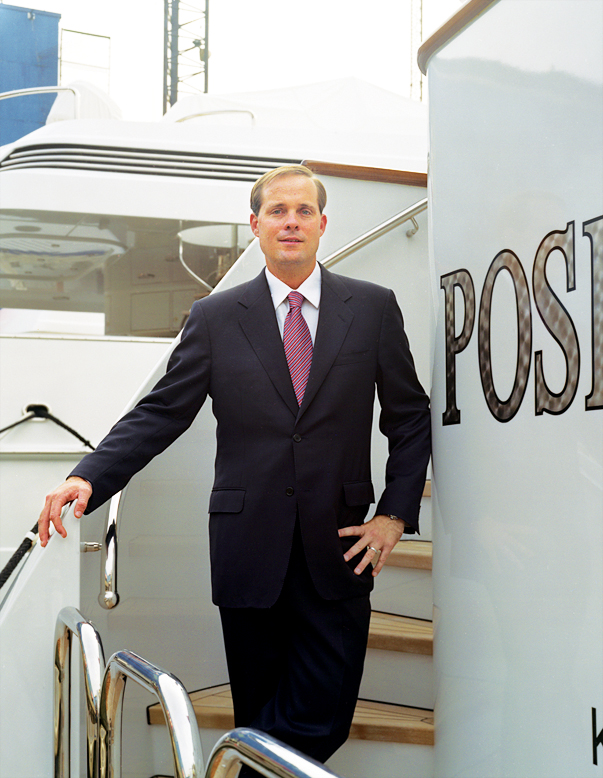

How to get rich trading "idiot" loans

The housing boom was good to John Devaney. Really good. He owns a Rolls-Royce, a Gulfstream Jet, a 12,000-square-foot mansion in Key Biscayne and a 143-foot yacht, as well as a few Renoirs and a valuable 1823 reproduction of the Declaration of Independence. Devaney's not a developer, and he's certainly not a flipper. The 36-year-old CEO of United Capital Markets is a bond trader. And one of his specialties is buying and selling bonds that are backed by the mortgage payments of ordinary homeowners. Option ARMs? Devaney loves 'em. "The consumer has to be an idiot to take on those loans," he says. "But it has been one of our best-performing investments."

Devaney's not out to get people into bad loans—or into good ones. He just makes bets on how many people will repay and when. Still, the $5.7 trillion mortgage-backed-securities market had a key role in today's housing mess. "The broker and the lender and everybody else in between is part of a factory that's producing bond securities for Wall Street," said attorney and consumer advocate Irv Acklesberg in testimony before a Senate committee recently. On the other hand, the fact that Devaney and other investors are willing to own mortgages may also be one of the reasons you could afford your house.

Banks have been selling off their mortgages to the bond market since the 1970s. Bond investors get the borrowers' monthly payments and the promise that they will be paid back, while banks get immediate cash and the chance to unload some risk. All this makes it easier for them to make new loans—good news for most borrowers. The trouble is, Wall Street's rocket scientists keep finding more sophisticated ways to repackage and resell mortgages. As a result, lenders stopped worrying so much about credit standards and learned to love risky loans.

Look, for example, at the financial Frankenstein's monster known as the collateralized debt obligation, or CDO. Brought to life in the 1990s, the CDO helped solve a knotty problem for lenders. They were often left holding a small amount of loans that were too dodgy to sell to investors at an attractive price. But what if you grouped the payments from all those risky mortgages together, along with some other investments, and you sold some investors the right to be the first ones to get paid? This would look like a relatively safe investment, and so—voilà!—you've transformed a risky loan into a triple-A rated security. Other investors would be farther back in line and might not get paid if things went badly. But you could offer those investors very high yields, so that hedge funds and pension funds would roll the dice.

This set the whole mortgage-bond sector on fire. Banks rushed to make mortgages—any kind of mortgages. Lousy credit? No problem. Can't prove your income? No problem. Can't pay more than 1% now? No problem.

Now a lot of that lending looks foolish. Mortgage delinquencies among so-called subprime borrowers have risen to 13%, the highest in at least 10 years. The market for the lowest-credit-quality mortgage bonds has tanked. And investors in CDOs may be in for a rude shock. "Some of the investors who bought CDOs certainly took on more risk than they thought," says John Weicher, a former assistant secretary of housing now at the Hudson Institute. But Devaney, who told a crowd of investors that the riskiest mortgage bonds looked "awful" before the crash, says he thinks he'll be buying. "I don't believe the carnage and fallout will be as bad as people think," he says.

Whether or not big investors come out okay, the damage is done for many homeowners. "The system allowed banks to create unsustainable loans that are going to haunt borrowers for years to come," says Allen Fishbein, director of credit and housing policy at the Consumer Federation of America. "Unlike the bank, the borrower has no way to lay off the risk."

What comes next? The pullback. Investors will be more selective about where they put their money, and banks will be more cautious in their lending. That's basically healthy. But the risk is that this will happen so fast that we'll see a vicious circle develop: Falling home prices mean less credit, and less credit means fewer buyers and, hence, falling home prices. That could make a housing recovery that much harder to come by. For the Quams, one can't come soon enough. "I worked so hard to be a homeowner, and now my dumb decision with this loan may take it all away," says Brandi. "We are newlyweds, bleeding money like crazy, and there are no Band-Aids."

Read Next: Money 101: Buying a Home