Your Rich Neighbor May Cut Spending More Sharply in Retirement Than You Do

- Retire With Money: Take Care in Picking an Advisor

- Retire With Money: Relax, You Don't Have to Get Everything Right

- This Tax Trick Could Be Incredibly Useful in 2017

- Retire With Money: Don't Let Trump-Mania Derail Your Retirement Plan

- Two Congressmen Are Trying to Kill a Program That Helps People Save for Retirement

Wealthy households reduce their spending by a greater percentage in retirement than do ordinary Americans, new data from J.P. Morgan shows.

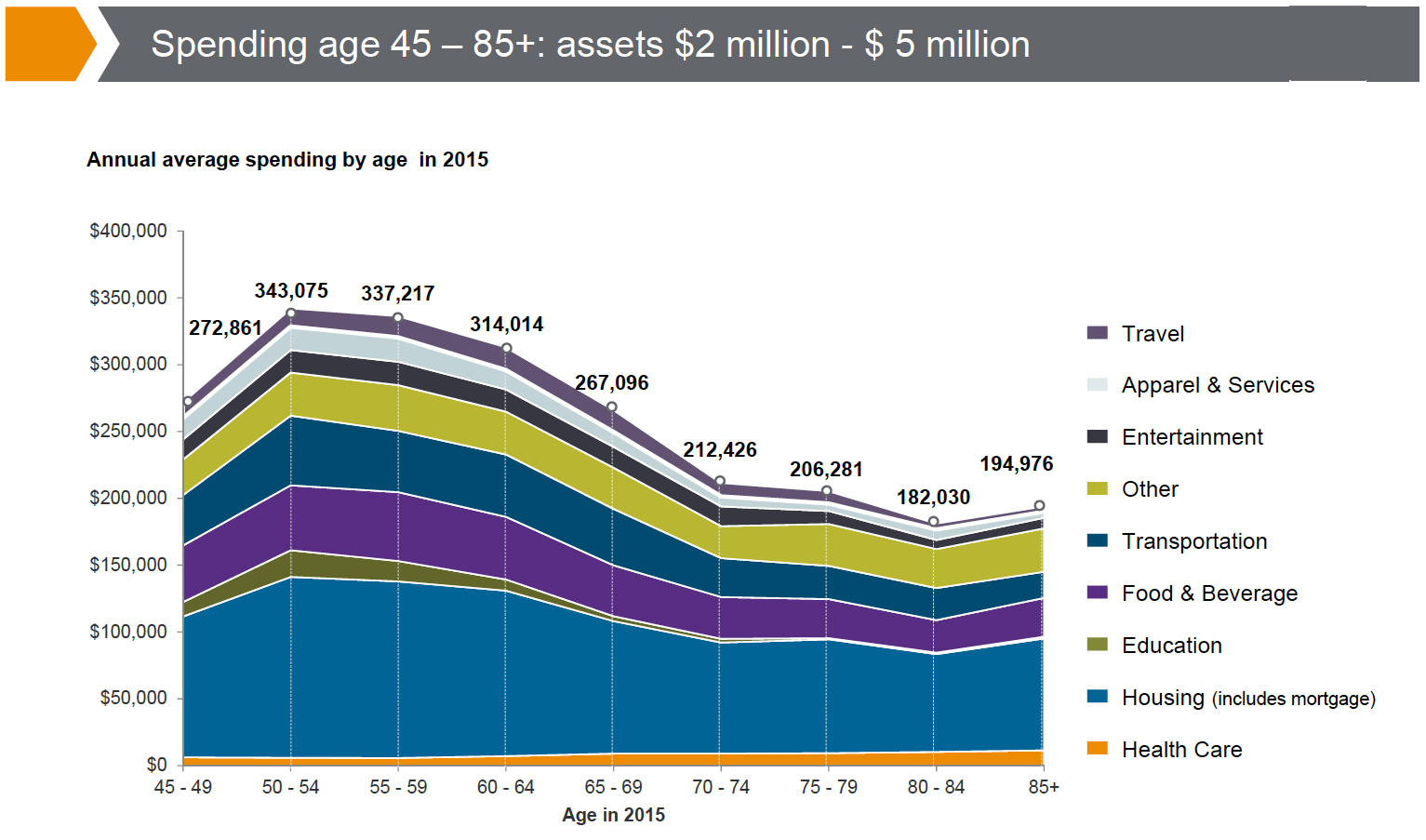

Among households with assets of $2 to $5 million, average annual spending between ages 80 and 85 is nearly 30% lower than for people with similar assets between ages 60 to 65, the bank says. Households with assets in this range have their highest earnings in their late 50s, at an average $350,000.

The spending decline in retirement is similar for households with financial assets of $1 to $2 million and also $500,000 to $1 million—with peak earnings of $250,000 and $200,000, respectively.

By contrast, the typical household in Chase's overall dataset has annual income of around $55,000—close to the national median—and average retirement spending drops only 20%. For these households, financial assets average just $50,000.

"For lower-income households, there's less ability to reduce spending, since a larger percentage of their income is going to essentials," says Katherine Roy, chief retirement strategist at J.P. Morgan, who led the study. Wealthier households have more discretionary income, so it's easier to trim in retirement. But what's surprising is by how much affluent people reduce their spending, when they probably don’t need to financially, she says.

In many cases, well-off seniors may be spending less as they slow down and simplify in later life. For higher-income families, especially, spending falls sharply for discretionary categories such as entertainment, food and beverage, and travel. "If you own a vacation home, you may give it up or visit less later in retirement," says Roy.

Here's J.P.Morgan's breakdown of spending trends for households with $2 to $5 million in assets:

Other research has identified a similar decline in retirement spending, especially for wealthier retirees. A Journal of Financial Planning study found that affluent seniors spend less than half their incomes in retirement. And David Blanchett, head of retirement research at Morningstar, has identified a so-called retirement spending smile—a decline in spending during early retirement that spikes up later in life.

Those studies were largely based on economic simulations. But the J.P.Morgan study analyzes actual transactions of 5.4 million households who spent a significant portion of their incomes through Chase bank or its credit cards. This group included 120,000 households with $500,000 to $5 million in assets. (The data was anonymized to protect privacy.)

At every income level, spending reached its highest point in midlife—typically around the ages of 50-54—when earnings also tend to peak. This is the life stage when many households are spending heavily on college tuition, paying down mortgages and often maintaining more than one car.

As families move into their late 50s and 60s, spending steadily declines, then starts to fall sharply in the late 60s and 70s. By age 80, expenditures tend to plateau at a lower level.

But not all spending declines in retirement. Health care expenditures typically rise at a rate that exceeds inflation. For households with $1 to $2 million in assets, medical spending has historically risen 6% a year between the ages of 65 t0 90, says Sharon Carson, retirement strategist at J.P Morgan. (The analysis did not include long-term care costs.)

Fast-rising health care costs can seriously dent the portfolios of even affluent retirees. A recent study by Fidelity found that a typical 65-year-old couple is likely to spend $260,000 on medical costs over the course of retirement. If the couple also had to cover long-term care expenses, that would add another $130,000 to their bills, Fidelity research shows.

To avoid a shortfall in later life, pre-retirees should budget for health care spending increases of 7% a year, says Roy. For your other spending, it’s reasonable to assume a 1.5% annual increase to keep pace with inflation.

Read next: Medicare Open Enrollment 2016: What You Need to Know

You can also hold down expenses by choosing the most cost-effective health coverage. For who get their coverage from an employer, open enrollment has begun at many companies, so check out Money's advice on choosing a workplace plan. If you have a marketplace plan, Obamacare enrollment begins Nov. 1. And if you're already on Medicare, your open enrollment began Oct. 15 and runs through Dec. 7, 2016, so start comparison shopping now.

And for retirees at all spending levels, it's a smart strategy to keep up the exercise, follow a sensible diet, and stay engaged in activities you enjoy. That way, you'll enjoy a happier and healthier life in retirement.