4 Big Investing Trends You Can Bet On for the Next Several Years

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

Exchange-traded funds are beloved for the ease and speed with which they can be bought and sold. But the real value in ETFs is helping you take advantage of big, sweeping market trends that unfold not over months but years.

You can find certain eternal truths in investing: Stay the course. Don’t buy on impulse. Use your computer for research, unless you’re in the bathtub. Most important, however, is this: Markets look to the future, not the past. And successful investing requires looking far into the future.

For insights, we turned to leading fund managers and market sages to determine the big trends that will guide stocks higher over the next decade. Their thoughts follow, along with recommendations for the best exchange-traded funds you can buy to ride these themes.

1. Foreign Stocks Are Due for a Comeback

If you’ve invested abroad over the past decade, you’ve lagged the S&P 500 index badly. Sacre bleu! In the past 10 years U.S. equities have gained an average of 6.7% annually. During that same stretch the MSCI EAFE index of foreign companies based in the developed world has lost 1.6% a year, as Europe and Japan have been struggling to grow.

Time to give up? Just the opposite. A decade is an unusually long period for international stocks to lag U.S. shares, which means the coming decade is likely to be much better than the last. “You really can’t exclude international much longer,” says Sam Stovall, chief investment strategist for the equity research firm CFRA.

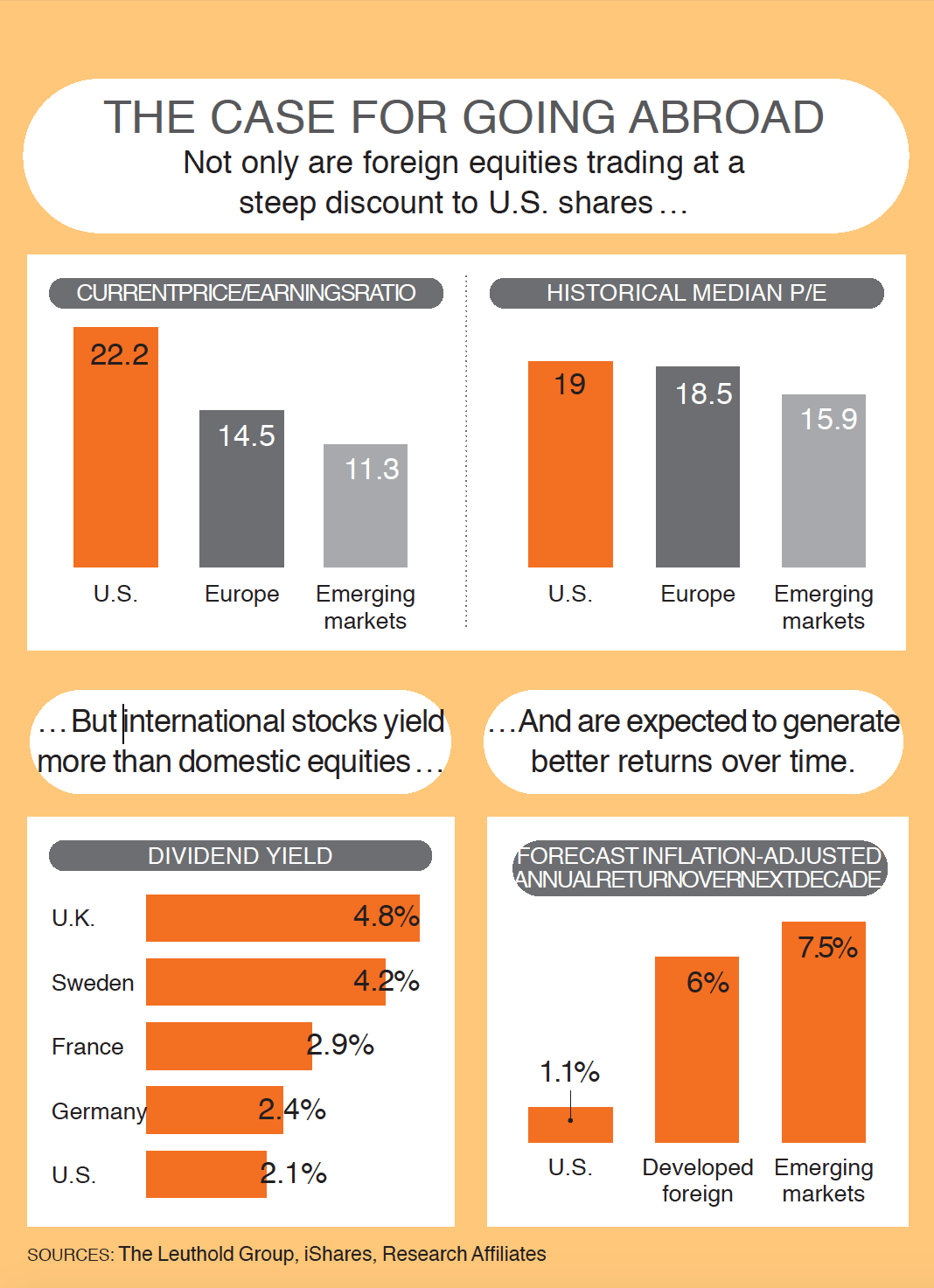

There are four main reasons to believe foreign stocks will bounce back. The first is valuations. U.S. and foreign stocks have historically traded on par with one another. But after nearly eight years of a bull market in the U.S. and lousy returns overseas, foreign shares now trade at a 15% discount to domestic equities. This is a big reason Research Affiliates, a respected research firm in Newport Beach, Calif., projects that foreign stocks will gain nearly 6% a year after inflation for the next decade. That’s five percentage points better than what the firm expects U.S. stocks to return.

Moreover, there’s “reversion to the mean,” which is a fancy way of saying that eventually, broad investment categories tend to return to their long-term averages. Though the MSCI EAFE index has lost ground over the past decade, foreign stocks have gained an average of 7.2% a year in the past 40 years.

The next reason is the strengthening U.S. dollar. When the dollar rises in value, returns from overseas stocks for U.S. investors decline. Suppose your Uncle Charlie, a U.S. expatriate, sent you 1,000 euros every year. At the end of 2014 you could have cashed in your 1,000 euros for $1,379, because one euro was worth $1.379. In December 2016 your 1,000 euros would have gotten you just $1,060, because the euro had fallen to $1.06.

Eventually, though, this disadvantage will turn into an advantage. That’s because a weaker euro means goods sold by European companies will be cheaper abroad, spurring growth in the eurozone. And as European profits bounce back faster than U.S. earnings this year, stocks there should fare well also.

Finally, there’s the emerging markets. Many stocks in the developing markets got clobbered when oil and other commodity prices collapsed in 2015, says Steve Janachowski, CEO of Brouwer & Janachowski, a Tiburon, Calif., financial planning firm. The stocks bounced back by 9% in 2016.

Wealth is spreading in emerging economies, so high-quality companies that cater to the growing middle class should see excellent growth in the next decade. In many cases it is companies in developed international countries that serve emerging markets consumers. “You’re getting in at a low starting point,” Janachowski says.

Your best ETF options

If you already have a modest dose of international equities in your portfolio, increasing that percentage could make sense for the next decade. Research by Vanguard shows that keeping 40% of your stock portfolio in foreign shares offers the best balance of risk, return, and diversification.

If you don’t want to constantly worry about what percentage of your equity portfolio to keep in international shares, consider a global fund like Vanguard Total World ETF (VT). You’ll get a sampling of the entire world’s stock markets—including the U.S.—for just 0.14% in expenses a year. The fund currently has about 45% of its assets in international stocks, and seven percentage points of that

is in the emerging markets.

If you simply want international exposure, it’s hard to argue with Vanguard All-World ex-U.S. ETF (VEU), which charges just 0.13% a year. In addition to investing about 15% directly in emerging-markets stocks, this Vanguard fund has as its biggest holding Nestlé, the Swiss multinational that generates more than half its sales in the developing world.

2. Inflation Rises From the Dead

If you remember the 1970s and early 1980s, inflation probably holds a big place in your closet of anxieties, along with those photos of you at the disco. While inflation has been deader than King Tut more recently—the consumer price index (CPI) has advanced just 1.8% a year on average over the past decade, vs. the historical average of 3%—it’s not unreasonable to think it could rise from the grave in the next decade. Lewis Altfest, chief investment officer for Altfest Personal Wealth Management, thinks inflation could return to 3% to 4% in the next couple of years.

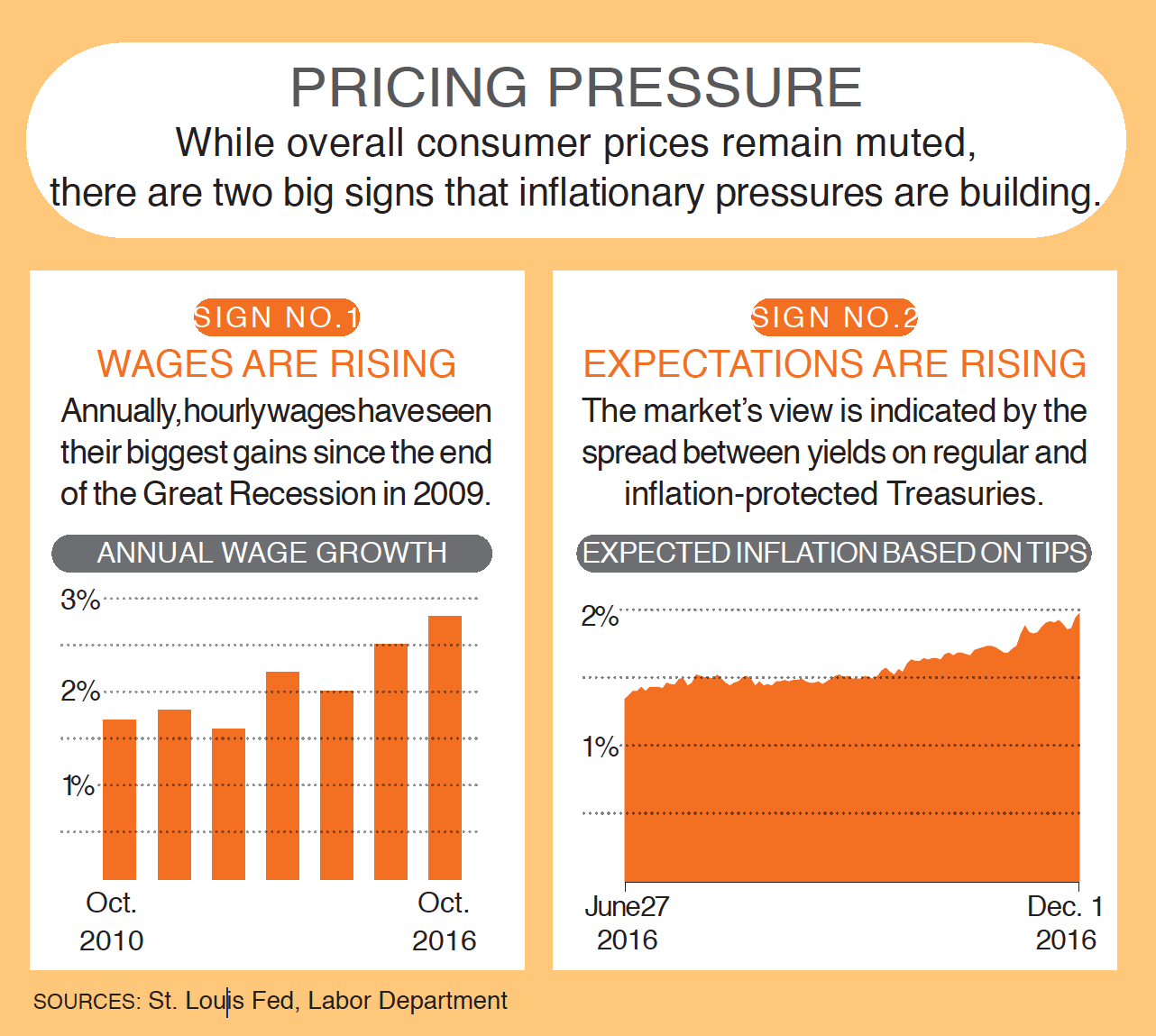

Why? For starters, inflation has been in hibernation lately because prices tend to flatten or fall during a recession, and fall they did in the Great Recession of 2008. In fact, the CPI fell from December 2008 to October 2009. But inflation isn’t just about consumer prices. Normally, when the unemployment rate falls as the job market improves, workers start demanding—and getting—pay raises. By and large, U.S. workers have gotten only nominal wage increases for the past decade. But over the past 12 months, average hourly wages grew 2.8%, the fastest rate since 2009, as the nation’s unemployment rate fell to 4.9%. That’s roughly what economists consider “full employment.”

Add to this the impact of the presidential election. Donald Trump has pledged to spend about $1 trillion to rebuild the nation’s infrastructure. He also promises to lower taxes and renegotiate trade deals such as NAFTA. “All three probably mean a higher inflation environment going forward,” says Conor Muldoon, a portfolio manager for Causeway Capital Management.

Your best ETF options

With inflation on the rise, attention naturally turns to Treasury inflation-protected securities, or TIPS. These government bonds can add to their principal every six months, depending on the increase in the CPI. The current yield on TIPS implies that investors expect a 10-year inflation rate of 1.9%, which is about where inflation stood over the past 10 years. This means that if inflation advances faster than that over the next decade, you would do better in TIPS than traditional Treasury bonds of similar maturities. “They are reasonably priced and a good value,” says Janachowski.

A good choice: Schwab U.S. TIPS ETF (SCHP), which is the cheapest TIPS fund, with a 0.07% expense ratio. A word of caution, though: When the government adds to the principal value of TIPS, it’s taxable as income. So in most cases, you will want to keep your TIPS fund in a tax-deferred account such as an IRA.

3. Health Care Spending Stays Strong

“A long-term trend? It’s health care. Nothing else is close,” says Dan Wiener, editor of the Independent Adviser for Vanguard Investors. U.S. health care spending rose half-a-trillion dollars, to $3 trillion, from 2009 to 2014, according to the latest data from the Department of Health and Human Services. And spending continues to grow: PwC’s Health Research Institute projects medical costs to climb 6.5% in 2017, the same rate as in 2016.

And, of course, health-spending growth isn’t confined to America. A rising middle class in developing economies abroad, particularly in China, augurs continued growth in medical spending. “The wealthier a country gets, health care spending as a percentage of GDP rises,” says Richard Schmidt, a portfolio manager for Harding Loevner. Health expenditures in the emerging markets, in fact, overtook spending in Germany, France, Italy, Spain, and the U.K. in 2010.

Plus, the number of people age 65 and older is expected to hit 604 million, or about 10.8% of the global population, by 2019, according to Deloitte. As people grow older, they need more medical services. Funds that focus on health stocks are down about 8% over the past year, partly due to uncertainty about how President-elect Trump plans to dismantle Obamacare. “You’re looking at a sector trading at a 20% discount to its long-term relative price-to-earnings ratio,” Stovall says.

Your best ETF options

Health care is a broad, deep industry whose components range from giant pharmaceutical companies such as Merck to small innovators like Cytokinetics, which is developing therapies for diseases that affect muscle function. You can capture that range of businesses through a single broad-based portfolio like Vanguard Health Care ETF (VHT).

This low-cost index fund, which charges a mere 0.09% of assets annually, has beaten a majority of its peers over the past one, three, and five years. In addition to its large stake in big drugmakers—investments in Johnson & Johnson, Pfizer, and Merck make up nearly a quarter of the fund—Vanguard Health Care holds about 22% of its assets in biotech stocks, the fastest-growing part of the sector.

Despite many ups and downs, biotech is entering an exciting phase. This group of health care stocks is finally beginning to take advantage of the mapping of the human genome. Personalized medicine—matching medicine with your genetic set—is now a reality. Illumina, one company in the Vanguard ETF, can now sequence a human genome for $1,000. The Human Genome Project cost $10 billion.

If you have a greater appetite for risk taking—along with an extremely long time horizon to recover from prolonged bouts of volatility—consider a fund that focuses mostly on biotechs such as SPDR S&P Biotech ETF (XBI).

In addition to promising but profitless startups, SPDR S&P Biotech will give you a dose of several big companies like Gilead Sciences, which has a market value of $100 billion thanks to its treatments for HIV and hepatitis C. Fees: a modest 0.35% a year.

4. Low-Cost Funds Drive Higher Returns

“It’s a theme that could thrive and thrive and thrive,” says Jim Lowell, editor of the Fidelity Investor newsletter, of the continuing focus on low fund costs. And it’s one that’s catching on: Investors yanked a net $193.4 billion from actively managed mutual funds in 2016 through October, while plowing $186.9 billion into low-cost index funds.

The mathematics of low-cost investing is simple: The less you pay your fund company, the more you keep for yourself. Consider $10,000 invested in two different funds that each earn a gross market return of 7%. Investment A takes 0.5% in expenses, while Investment B takes 1.5%. After 30 years, Investment A will be worth $66,100. Investment B? $49,800—more than $16,000 less.

And it’s not just index funds, or even low-cost actively managed funds, that will keep gaining investors’ attention. “My sense is the investment advisory business is seeing some real price competition,” Lowell says.

Low costs will become even more important if coming years see returns from stocks and bonds that are below the long-term averages, as Vanguard’s Fran Kinniry and other pros expect.

Your best ETF options

If you’re a broadly diversified investor, you’ve got plenty of low-cost options, including those on our Money 50 recommended list of funds and ETFs.

While Vanguard is synonymous with low-cost indexing, you can find many cheaper exchange-traded funds these days from iShares and Schwab. Consider the lowest-cost ETFs on the market: Schwab U.S. Broad Market ETF (SCHB), with an expense ratio of just 0.03%; Schwab U.S. Aggregate Bond ETF (SCHZ), charging 0.04%; and iShares Core S&P 500 ETF (IVV), which costs a mere 0.04% a year. These funds will give you broad exposure at a minor cost.