3 Smart Investments When Interest Rates Are Rising

Of the 500,000 or so earthquakes detected each year, only about 100 cause any damage. Still, it makes sense to look around when you hear the ground rumbling. Similarly, rising interest rates aren't the end of the world, but when the Federal Reserve starts lifting rates, you should at least check if your portfolio is strong enough to withstand some shaking.

The Fed caused a minor tremor in December 2015, when it raised a key short-term rate by a quarter of a percentage point. Two other small increases have since followed, the most recent one in March. "Our belief is there will be two, maybe three rate hikes this year," says Stephen Wood, chief market strategist at Russell Investments.

Understand that the Fed sets only short rates, which affect yields on money funds and CDs. It doesn't set longer-term rates, such as what 10-year Treasury notes pay—the market does that. "While the underlying economy is strong enough to support higher rates, it's not likely for long rates to move in lockstep," says Andy McCormick, head of the U.S. taxable bond team at T. Rowe Price. He feels that long rates won't move up as much.

Translation: There's no need for tectonic shifts in your portfolio.

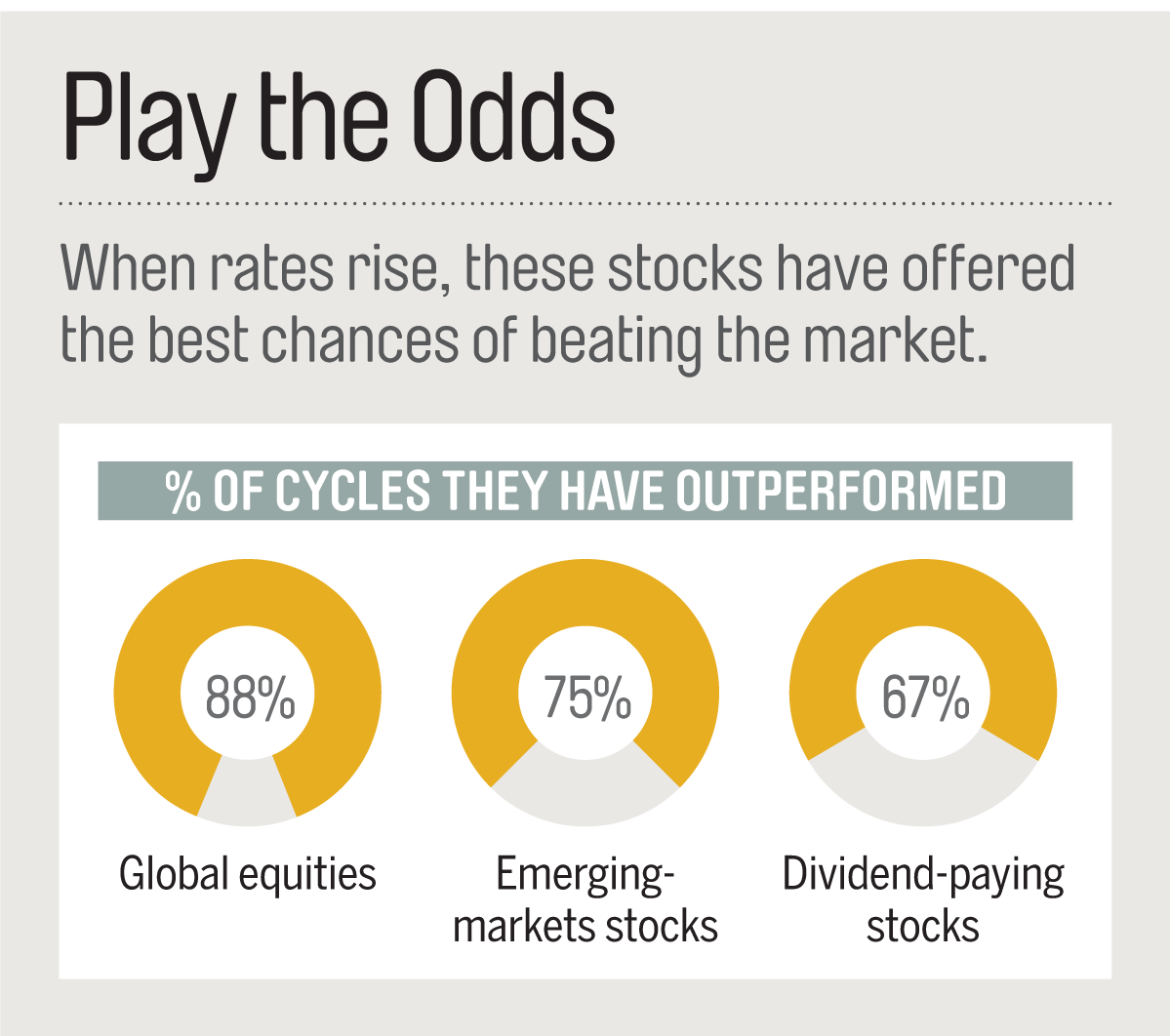

What Does This Mean for Investors?

Rising rates put fixed-income funds at risk, since the older bonds they own may become worth less relative to newer, higher-yielding bonds. But that's not true for all types of debt. Similarly, while higher rates could splash some cold water on stock market euphoria, not all equities may be hurt.

• Foreign Funds

Higher rates in the U.S. tap the brakes on growth, which hurts domestic equities. They also attract foreign investments, which can push up the value of the dollar. And a strengthening buck automatically reduces the gains of Americans investing abroad.

But the Fed has done everything except put up billboards saying it will raise rates, so the currency market may have already built future rate hikes into the dollar's lofty value. In fact, the dollar has already eased a bit this year.

This is an opportunity for foreign equities, especially if the strong dollar flattens or sells off while rates overseas stay at zero to promote growth. "Europe is coming out of the doldrums, and things are starting to turn around," says planner Steve Janachowski.

• Floating-Rate Funds

Conventional wisdom says stick with short-term bonds because their prices fall less than longer-dated debt when rates rise. But short rates are climbing faster than long-term yields.

This is an ideal time to look to short bonds with yields that "float" with the market, like bank loan funds that invest in adjustable-rate loans, McCormick says. T. Rowe Price Floating Rate (PRFRX) currently yields 4.11%.

• Real Estate Funds

Even with two or three Fed rate hikes this year, investors will still be lusting for yield. Real estate funds, which have barely moved in the past 12 months, currently yield 4.16%—twice the yields of the S&P 500 and 10-year T-note rate. Vanguard REIT Index Fund (VGSIX) yields 4.52% and charges just 0.26%.