This 35-Year-Old Mother Is Saving $85,000 a Year in New York City and Plans to Retire in 5 Years. Here’s How

Jamila Souffrant has learned to embrace the journey, whether that’s her 90-minute, one-way commute from Brooklyn to New Jersey or her path to financial independence.

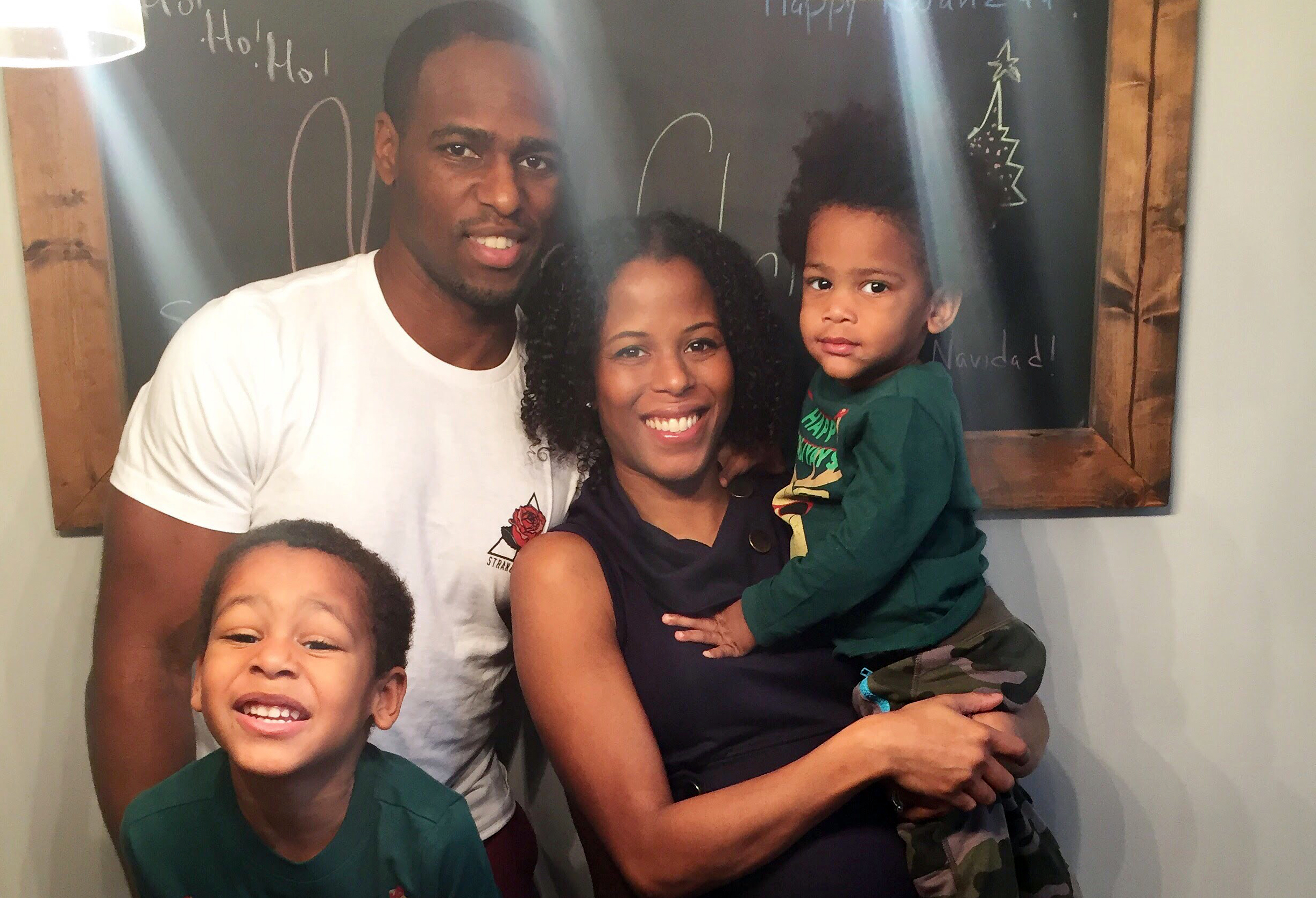

The 35-year-old commercial real estate executive and mom of two boys—with a third child, a girl, due any day now—hopes to reach FIRE by age 40. That’s an acronym for financial independence, retire early, a mantra that’s being adopted by a growing number of millennials. But even if Souffrant doesn’t reach her goal by her target age, she knows she will have accomplished plenty along the way.

“Once you start, you don’t know the twists and turns along the way that will make your life better,” she says.

Souffrant first learned of early financial independence through podcasts she listened to on her long commute, such as Radical Personal Finance and The Mad Fientist. The concept struck a chord: She likes her job but isn’t passionate about it. And the commute can be soul-sucking: the 90-minute drive home to Brooklyn from Morris County, N.J., occasionally stretches to three or even four hours in bad traffic. “This wasn’t what I wanted to do with the rest of my life,” she says.

In 2016, Souffrant started a blog, Journey to Launch, to keep herself accountable to her goal. That year, she and her husband, Woody, also 35, managed to save $85,000 — in one of the world’s most expensive cities, with two young children. Here’s how she did it.

The Spouse Pitch

Souffrant knew she and her husband would have to up their savings game considerably in order for her to be able to stop working in five years, even if Woody stayed at his job. If he were to join her in early retirement, the couple would either have to move to a lower-cost city, or slash their expenses even further, in order to live solely off their investments. But Woody enjoys his job as a high school gym teacher and wants to keep working, so the couple is budgeting his income—and workplace health insurance—into their projections for what Souffrant says might more accurately be described as their "partial financial independence" in five years.

Woody was contributing to his retirement account, but socking away only about 4% or 6% of his pay. Souffrant wanted to boost that savings rate up to 50%. But before she sat Woody down to make the ask, she ran some spread sheets showing how much money the couple would have at various ages if they saved a certain amount, assuming a certain market return.

Then, when the two sat down to talk about it, she showed him the numbers. “I immediately got nervous,” Woody recalls on a podcast the two taped together.

But Souffrant won him over through her passion and preparation. Plus, she agreed to honor his wishes. For example, Woody might one day like to own a luxury car—a big no-no among FIRE followers, who see automobiles as big, depreciating money suck—and she says she’d be happy for him to buy one if their budget allows.

Automatic Pre-Tax Savings

Woody began slowly in his goal to boost his savings rate to 50% from around 5% of his pay. He started by increasing his contribution rate by one or two percentage points per month. Instead of nagging him to go quicker, Souffrant enthusiastically praised his progress. After a few months, he abandoned the gradual approach and bumped his rate straight up to 50%.

That meant maxing out both of his pre-tax savings vehicles: as a New York City public school employee, he is eligible to contribute to both a 403(b) account and a 457 account for government workers. He put the maximum allowed by the Internal Revenue Service, or $18,000, into both, and Souffrant put $18,000 into her 401(k). (The maximum for 2018 is $18,500.)

Woody boosted his income too, working coaching jobs after school and banking the extra savings. Souffrant started pulling in some money from her blog and a related consulting gig helping people take control of their finances.

Cut the Big Three

Roughly 62% of the average American’s annual spending goes toward just three expense categories: housing, food and transportation, according to the Bureau of Labor Statistics. Trimming these expenses can give you the most savings bang for your buck.

Woody used to spend hundreds of dollars a month leasing a fancy car, but he gave that up and bought an economical ride outright. The couple bought their home, a single family home in South Brooklyn, on a short sale. They used some proceeds from the sale of their one-bedroom in Downtown Brooklyn to renovate their new place.

The couple also cut back on their one indulgence, going out to eat for Mexican and Caribbean food, whittling their monthly restaurant budget in half.

They also save big on childcare expenses. Souffrant’s aunt lives in a separate, basement apartment in their house and cares for her two boys. She lives rent-free in exchange for a lower salary than she would receive on the open market.

Souffrant doesn’t plan to retire to become a stay-at-home mother—“not that there’s anything wrong with that,” she notes. Instead she’d like to work full-time on her Journey to Launch business, which also includes a podcast series.

In the ideal scenario, the couple won't touch their savings after Souffrant quits her job. Instead, they'd live off Woody's income and income from Journey to Launch. They also net about $645 a month from an apartment they own in a fancier neighborhood of Brooklyn—a studio that Souffrant bought in her early 20s—that they rent out, a tactic that a lot of FIRE followers say is clutch.

She wants to help others start down the path to financial independence. “There are so many wins along the way,” she says.