This Chart Shows How Quickly You Can Save for a Down Payment on Your First Home

Saving for a down payment on a first home is never easy. But it may not take as long as you think.

A recent survey from the National Association of Realtors found that among millennials — who now represent the largest group of home buyers in the country — a majority of those who bought a house last year had been saving for less than year.

How did they save so quickly?

For one thing, they bought their homes with relatively little down. The median down payment for buyers younger than 37 was just 7% of the value of the house. While that's more than the 3.5% down payment required on loans insured by the Federal Housing Administration (FHA), it's significantly less than the the 16% or more down payments made by Boomer buyers.

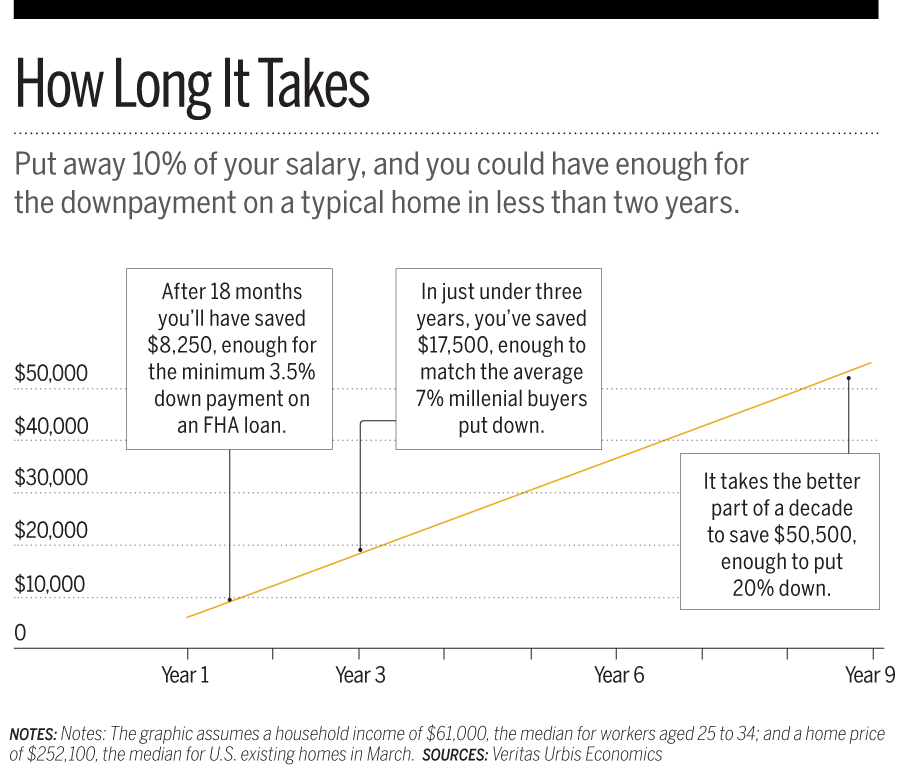

In fact, when you consider how much you really need to put down, you may be able to cobble together enough to purchase your first home in just a few years or less, assuming you earn a middle-class salary and are willing to buy a moderately-priced home — one close to the $252,000 median for existing single-family homes, according Federal Reserve data.

Putting the 20% Down Payment Rule Into Perspective

For many home buyers, a 20% down payment has long been the rule of thumb. The notion was reinforced during the global financial crisis a decade ago, when home buyers got into trouble after purchasing property with little or no money down — on the assumption that rising prices would reap them a quick investment profit.

While you still need 20% down to get the cheapest possible mortgage, many housing experts concede that it's often unrealistic for young first-time buyers who, unlike older bidders who already own a home, can't count on any equity built up in a previous house.

"Putting 20% down is ideal, but it's not always practical," says Ralph McLaughlin, chief economist at Veritas Urbis Economics, a real estate consultant. "Most first-time home buyers don't put anywhere near 20% down."

In fact, the federal government and states have a range of programs designed to help young and less-wealthy buyers purchase homes with smaller down payments. The best known program, from the FHA, insures loans on home purchases with as little as 3.5% down.

Many states and towns also have their own programs, which typically offer assistance in the form of a grant or interest-free loan to be repaid when the home is sold.

While there are often restrictions based on income and home value, there are hundreds of options available, says Rob Chrane, chief executive of Down Payment Resource which tracks the programs. (The site makes money by licensing its software to lenders but is free for individuals to use.)

The Pros and Cons of Buying a Home With Less Than 20% Down

Buying a home with a small down payment does have its downsides. FHA loans require borrowers to take out insurance against default, which can add anywhere from 0.3 to 1.5 percentage points to your interest rate, according to Bankrate.

The good news: Once the equity you've built in the house reaches 20% of your home's value, you can refinance to a loan without insurance.

Of course, all this assumes you can afford to buy a home in the first place.

Buying mid-priced $250,000 home should mean total housing costs of $1,800 to $1,900 a month, including taxes, insurance and a 30-year fixed mortgage at today's interest rates. That monthly burden ought to just fit within the budget of a millennial with a median salary of $61,000 based on Census data.

If, however, you live in an expensive city like San Francisco or New York, appropriate homes may cost two or three times the national median, with monthly mortgage costs that are also double or triple. There is little point in cobbling together a down payment if your salary can't cover the mortgage payments.

That said, for young people in most areas of the country, the dream of home ownership may not be as far off as you think.