The Ultimate Guide to Doing Your Taxes in 2019: What Changed, How to Save and More

- $1,400 Checks and More: 6 Ways You May Benefit From the New Stimulus Package

- What the Democrats Winning Georgia Means for Your Wallet

- You Have Less Than a Month to Qualify for This Special Pandemic Tax Deduction

- Joe Biden Is the President-Elect. Here's What It Means for Your Wallet

- Coverage for Pre-Existing Conditions Is at Stake Nov. 3. Here's Where Trump and Biden Stand

- What the Democrats Winning Georgia Means for Your Wallet

- Joe Biden Is the President-Elect. Here's What It Means for Your Wallet

- H&R Block Wants to Put Your Tax Refund on an Amazon Gift Card. Here's Why That's a Terrible Idea

- Super Rich People Aren't as Super Rich as They Once Were

- MacKenzie Bezos’s $36 Billion Divorce Settlement Makes Her the Fourth-Richest Woman in the World

Tax day is fast approaching. This year, thanks to the 2017 Tax Cuts and Jobs Act, your tax return—not to mention the amount of your refund—could be a lot different. The law, which represents the tax code's largest overhaul in a generation, is designed to both lower what you pay and make filing easier.

But that's not true for everyone.

Read on find what you need to know, no matter what kind of tax payer you are.

You're Middle Class.

What Changed?

Most of us would like a tax cut. The new law attempts to deliver that in several ways. One is new, lower rates for several middle-class tax brackets. For instance, workers who earn up to $82,500 in taxable income will now pay a top rate of 22%, compared with 25% under the old rules. Perhaps an even bigger change, however, is a dramatic increase in the amount of money taxpayers who don't itemize their returns are allowed to exclude from their taxable income in the first place. This sum, known as the standard deduction, nearly doubles, to $24,000 from $13,000 for couples and to $12,000 from $6,500 for singles. The change means most middle-class taxpayers will avoid owing any income tax at all on thousands of additional dollars that they earn.

In addition to lowering what you owe, lawmakers also tried to make filing easier by making good on a long-term Republican campaign pledge to simplify tax forms—even to the point where they could fit on a postcard. The result is that old forms like the two-page 1040 and single-page 1040EZ have been replaced with a new version that takes up just half a page, front and back.

What You'll Save

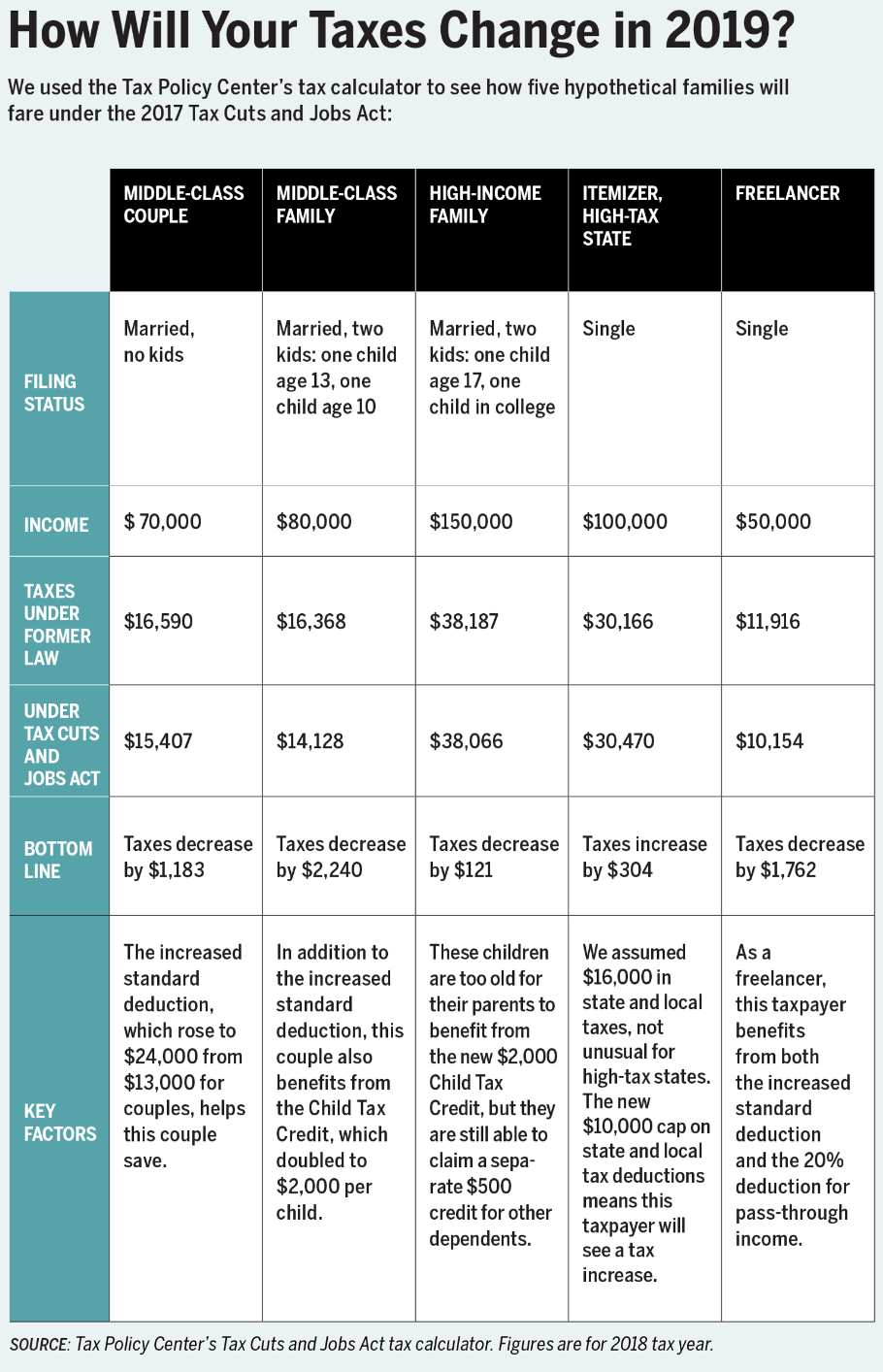

The doubled standard deduction and lower rates should translate into a tax cut for most middle-income Americans. Those earning from $49,000 to $86,000 will pay an average $930 less under the Tax Cuts and Jobs Act than under previous tax law, according to the Tax Policy Center, a Washington, D.C., think tank. Still, a lot depends on your individual situation. (See table at the bottom of this table.)

One big caveat: The individual provisions of the Tax Cuts and Jobs Act are only temporary. By 2026, those savings start to phase out.

The Limits of Simplicity

Tax experts haven't necessarily been enthused with the new tax postcard. That's because while it reduces the number of lines on the IRS's flagship tax form, the provisions of the tax code they dealt with haven't gone away. Taxpayers who receive additional income or owe the alternative minimum tax, for instance, must now consult one or more of six new schedules.

An even bigger issue: These days only a small minority still fills out tax forms with paper and pen, according to the IRS. "This is 2019," says Eric Toder, codirector of the Tax Policy Center.

The vast majority of filers who use modern tax software (find out if you qualify for free tax filing) should experience no change at all.

You Itemize

What Changed?

Among those due for big changes are middle- and upper-middle-class earners who are used to claiming deductions for their property taxes and other expenses. This year, roughly 18 million taxpayers are expected to itemize, down from 46 million last year, according to the Joint Committee on Taxation.

A key reason for this, of course, is the new, more generous standard deduction. But it's not all good news. The new law also curtails a number of individual deductions, making them potentially less valuable. One of the biggest—and most politically controversial—changes is a new $10,000 cap on the previously unlimited amount taxpayers could deduct in state and local taxes.

Residents of high-tax states including California, New York, and Maryland will be hardest hit.

Wealthy homeowners will also lose a tax break. Under the new rules, taxpayers will be allowed to deduct interest paid on mortgages of up to $750,000, which is down from the previous cap of $1 million. Much like the cap on state and local taxes, that's likely to most hurt residents in urban and coastal areas, where real estate values are the highest.

But be aware: The new cap applies only to mortgages taken out after Dec. 14, 2017. So if you bought before then, the old, higher cap remains in effect.

Do a Dry Run

That millions of Americans no longer need to itemize, at least until the law begins to phase out in 2026, is a big plus. But it comes with a caveat. There's no way to know for sure whether it still makes sense for you to itemize without tallying up the deductions you could potentially claim and comparing the result with taking the standard deduction.

In other words, you still have to do most of the work, according to Cindy Hockenberry, director of tax research at the National Association of Tax Professionals. Otherwise "you could be leaving money on the table and shortchanging yourself," she says. "No one wants that."

Who Pays More?

While the new rules should mean a tax cut for most Americans, residents of high-tax coastal states with hefty mortgages are among the minority who could fall through the cracks. Roughly 9.4% of taxpayers in Maryland will end up owing an average of $1,490 more than under the old rules, while 8.6% of Californians will pay an average $2,510 more for 2018, according to the Tax Policy Center.

You've Got Kids

What Changed?

The enlarged standard deduction is a big boon for taxpayers. But to make it possible, policymakers had to rejigger many other parts of the tax code, including some that have long benefited parents. The result is a complicated set of tradeoffs that should leave most—but not all—families better off.

To offset the cost of expanding the standard deduction, one of the bill's most expensive provisions, Congress eliminated another longtime perk: the $4,050 personal exemption that taxpayers could previously claim for themselves, a spouse, and each dependent. Because taxpayers could claim an exemption for each child, simply eliminating the provision would have meant tilting the benefits of the tax code away from parents.

To fix this, Congress sweetened another perk targeted at families—doubling the value of the Child Tax Credit to $2,000 from $1,000 and dramatically raising the income threshold at which it begins to phase out, to $400,000 for couples from $110,000, ensuring that many more families will be able to take it. The change "will benefit families across the income spectrum," says Tax Foundation analyst Erica York.

How Families Fare

A married couple with two small children who earn $80,000 and don't itemize will end up owing about $2,240 less in 2019, according to the Tax Policy Center's tax calculator. With a third child, their savings would increase to nearly $2,620.

The New Credit's Limits

Some tax experts have complained the new Child Tax Credit isn't as generous to low-income families as it might have been. While the old $1,000 version was refundable (with certain restrictions), only $1,400 of the new credit is. That means families without $2,000 of income tax liability per child won't be able to claim the full amount.

Kids' Ages Matter

Under the old rules you could claim an exemption for each child under age 19, as well as any child age 19 to 24 who was also a student. By contrast, the new, expanded Child Tax Credit is available only for kids age 16 and under. To address this discrepancy, Congress created yet another new perk: a $500 nonrefundable tax credit for any dependent who isn't eligible for the Child Tax Credit.

You're a Retiree

What Changed?

The Tax Cuts and Jobs Act didn't take direct aim at retirees, so don't expect any change to, say, the taxation of your Social Security benefits or your required minimum distributions. Some of the law's provisions, however, disproportionately affect older adults. Perhaps the biggest is the medical deduction. Nearly 9 million Americans deducted medical expenses in 2015, and nearly three-quarters of them were older than 50, according to an analysis by the AARP Public Policy Institute.

For 2018, tax law lowered the threshold for writing off your medical expenses to 7.5% of your adjusted gross income, from 10%. But that lower level expired last year, and for 2019, it's going back up to 10% for taxpayers of all ages in order to write off qualifying medical expenses.

Know Your Costs

Don't assume that you'll never be able to claim this deduction. Make sure you're familiar with all the procedures and services that can qualify for a medical write-off. You can find them in IRS Publication 502. Qualifying home improvements like, say, a wheelchair ramp, are an area that many retirees frequently overlook.

Bunch Your Costs

If you don't consistently incur high enough medical expenses in a given year to write them off, consider bunching your spending so that you can at least take the deduction one year. That means, for example, scheduling qualifying elective surgery, the purchase of new hearing aids, and a home improvement for the same year.

You Work for Yourself

What Changed?

Boosting the economy was one of tax reform's key goals. As a result, freelancers and small-business owners are some of the law's biggest winners. The biggest perk is a new 20% deduction on so-called pass-through or qualified business income available to anyone who is the owner of an LLC or an S corporation, a partner, a sole proprietor, or a gig-economy worker.

The deduction, which is available even to workers who also take the standard deduction, means a single freelancer with no kids making $50,000 will save about $1,750 under the new rules, according to the Tax Policy Center's calculator. That's nearly $700 more than for a similar wage earner. Wealthier taxpayers, such as business owners, could save tens of thousands.

Look for a 1099

If you get only a W-2, the deduction for pass-through income likely doesn't apply to you. But if you get one or more 1099 tax forms—say, if you moonlight as an Uber driver—you are probably eligible, according to tax pros.

Those who cannot claim the deduction, however, are hobbyists. The IRS distinguishes a hobby from a business using nine criteria, such as record keeping and intent for profitability. Mark Jaeger, director of tax development at TaxAct, says a good rule of thumb to follow is that if it's something you've engaged in and made money in over the years continually, the IRS might be more inclined to view it as a business.

The Service Exception

Many wealthy professionals face restrictions. Businesspeople in fields characterized as a "specified service"—including doctors, lawyers, and accountants, as well as entertainers and consultants—may not be able to claim the full deduction. People in these fields who have business income higher than $157,500 ($315,000 if married and filing jointly) are subject to limits on how much of the deduction they can claim.