A Simple Plan to Stop the Next Financial Crisis

- Here's Why Citigroup Is Shelling Out $7 Billion

- Jack Bogle, Who Revolutionized the Way Millions of Americans Save and Invest, Dies at Age 89

- Why Trouble in China is Hitting Your 401(k)

- Why China's Currency Has Been Knocking Down U.S. Stocks

- Jack Bogle Explains How the Index Fund Won With Investors

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

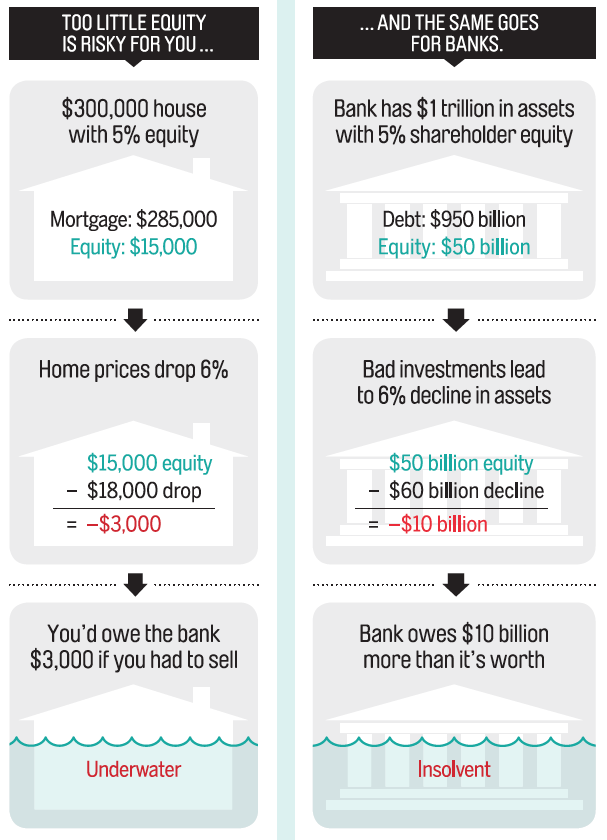

Here's one thing every homeowner knows: The less equity you have in your house, the more likely you are to get in financial trouble.

This was easy to forget for a time in the mid-2000s, when house prices were climbing. But when real estate prices reversed, many borrowers who had put little or no money down quickly found themselves "underwater," owing more on their houses than they could sell them for. People who had stuck to the old-fashioned 20% down-payment rule of thumb, on the other hand, had a cushion. Their house had to lose at least 20% of its value before they were stuck in a mortgage they couldn't get out of.

Anat Admati, a professor at Stanford University's graduate school of business, and German economist Martin Hellwig think the exact same lesson ought to be applied to banks.

Monday marks the sixth anniversary of the Lehman Brothers' bankruptcy, the trigger event (if not necessarily the cause) of the worst of the global financial crisis. As part of an occasional series, I've been looking at different proposals to prevent the next panic. One obvious step is to regulate how banks lend out money, to crack down on predatory loans. Admati and Hellwig come at the problem from another direction — one that's particularly apropos on the Lehman anniversary — by proposing tougher rules on how banks get their money in the first place.

They argue that banks should borrow less, relative to their assets. After all, what turned a bubble in real estate prices into a full-on financial panic was not just the toxic loans banks gambled on, but the fact that they too were playing with borrowed money.

In a nutshell, Admati and Hellwig say that 20% to 30% of the money a bank puts to work should be funded from shareholders' pockets, instead of from debt. Currently, that number for big banks — their equity or "capital," in bankers' jargon — is more in the neighborhood of 5% to 6%. In other words, about 95% of banks' assets (which includes the mortgages, business loans and other investments they hold) are matched on the other side of the balance sheet by money banks owe (to everyone from depositors to bondholders.) And that means, roughly, that if the value of a bank's assets falls by more than 6%, it now owes more than it is worth.

Admati's and Hellwig's idea is getting attention. Admati has been the subject of a long profile by Binyamin Applebaum in the New York Times. Top Federal Reserve officials are citing her, and Applebaum says she's lunched with Barack Obama at the White House. But the proposal has admirers on both sides of the ideological divide. Economist John Cochrane, no fan of Democratic banking reforms like Dodd-Frank, has praised Admati. And Republican Sen. David Vitter is co-sponsoring legislation requiring 15% capital with Democratic Sen. Sherrod Brown.

My Money colleague Kim Clark interviewed Admati at length back in 2013 about her book with Hellwig, The Bankers' New Clothes. You can read the interview here.

I said in the headline that this plan is simple — and that's true in the sense that it's elegant. Instead of getting into the weeds of defining tricky concepts like "Too Big to Fail," it puts a big, bright number on how much capital a bank has to hold to be considered safe. (Defining "capital" can in fact be contentious and complicated, but demanding a lot of it makes it harder to game.)

The tricky part is that it's not so simple for people who don't know banking to get why capital or equity is so important, or even what it is. As Admati frequently points out, banks have benefited from the misconception that higher capital requirements means banks would have to keep 20% or 30% of their money locked up in a vault, instead of lending it out to businesses or homeowners.

In fact, making banks "hold more capital" actually means they have to borrow less. In their book, Admati and Hellwig show that this is almost exactly like a homeowner making sure to build up equity in her house. This graphic published with Kim Clark's Money interview with Admati shows how it works:

To raise more capital, banks wouldn't hold back lending. Rather, they'd tap their shareholders, either by issuing new stock or just by cutting the dividends they pay out of earnings, letting profits build up on the balance sheet. (They can still lend that money out if they choose — the point is, it wasn't borrowed from someone else and won't have to be paid back in a crisis.) This would be unwelcome news to many investors in banks, who often invest in large part to get those dividends.

Recently, I spoke with Brian Rogers, a fund manager at T. Rowe Price who invests a lot in banks, and he was satisfied that banks had already done enough to clean up their balance sheets and raise capital. Admati and Hellwig would doubtless say that investors' confidence in banks now has a lot to do with the fact that the government bails the industry out when it gets in trouble.

Making banks less attractive to some stockholders, and limiting their ability to take advantage of debt when it's attractive, could make them less eager to lend, raising interest rates.

In their book, Admati and Hellwig argue this isn't necessarily the case — some investors might prefer to hold stock in less-risky banks. But even if there is a cost to safety, by now we have a pretty good idea of how expensive — for everyone — the alternative can be.