The One Thing You Have to Know to Invest on Your Own

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

With the 4th of July on the way, the editors here at Money.com asked me to think about what it takes to become an independent investor.

I'll take "independent" to mean something that most people with a 401(k) or an individual retirement account can realistically do. I'm not talking about sitting at your desk all day trading your own portfolio of stocks. In fact, the way I think about independence, you'll want to automate about 99% of the investment decisions in your portfolio — specifically, which individual stocks and bonds to hold. The independence that matters has nothing to do with security selection. It's about cutting out costly middlemen, from advisers who help you select investments, to the managers who pick the securities inside the mutual funds you may hold.

The rewards to doing this are significant. A high-cost mutual fund may shave 1% or more off of your investments each year, which can easily add up to six figures in fees and foregone gains over a lifetime as an investor. Eliminating layers of management also means you are less exposed to the quirky risks someone else might take with your money.

You don't need a lot of time or expertise to pick these middleman-free investments. You can build a portfolio that holds a diversified slice of stocks and bonds with just three index mutual funds, portfolios that mimic the composition of the overall market at very low cost. If stocks rise 8% in a year, you'll earn 8% or very close to it. You very likely have index options in your 401(k) plan—if not, say something to your HR manager!—and index funds are easy to buy in an IRA.

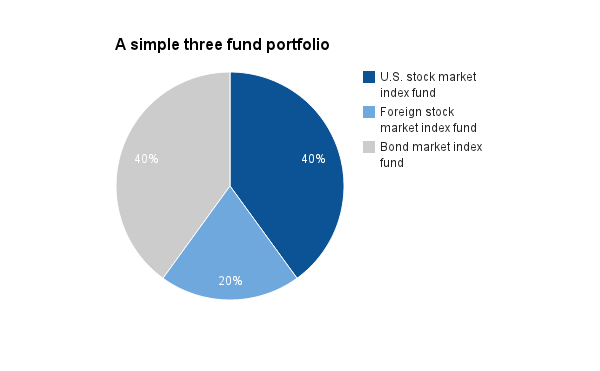

Below is what that portfolio might look like. You can adjust the split depending on you appetite for risk, but the one below is a good starting point for many long-term investors saving for retirement. (The less you can stand to lose, the more you'd add to the bond fund.)

In contrast to typical funds, this portfolio will cost you less than 0.1% of assets per year, and will get with three easy decisions exposure to literally thousands of stocks. You can choose index funds from our Money 50 list of recommended funds.

It's easy to say that anyone can do this, of course. But I think a lot of people lean on investment middlemen because they aren't sure they know enough about investing to do it themselves, and even if they want to learn, they aren't sure which knowledge really matters. There's so much you could dive into: stock sectors, "P/E" ratios, the January effect, EPS growth, upside earnings surprises, etc., and etc.

So here's the one thing I think you have to understand to be a competent, on-you-own investor: Where the return on your investments really comes from. And the answer is that, for stocks, it comes from two sources. You own businesses, and you are taking a risk to do so.

Beginners are often introduced to the market with the old saying, "buy low and sell high." This isn't wrong (doing it the other way sure won't feel good), but it's not at all helpful. It makes investing sound a like a game of wits against other investors — first you figure out when a stock is too low, and then sell it when somebody else is willing to buy it for more than its worth. That's hard, and you have to learn a lot about companies, accounting and human psychology to even attempt it. The whole edifice of the middleman money management business is built on the fact that most people believe they can't do this themselves, or don't want to.

But to be a buy-and-hold index investor, you can throw out "buy low/sell high" and the game-playing thinking that tends to go with it. This isn't about finding a greater fool to buy your stock further down the road. Owning stocks gives you a claim on the earnings of companies. As an owner, you make money over time either because you are being paid a dividend out of profits, or because profits are being reinvested in the business to make it more valuable. Index funds give you a share in the future profits of the America's, or the world's, public companies. It's almost as simple as that. Almost.

The other, crucial part of the equation is that the earnings of companies are uncertain and so are the cash flows shareholders will get. Stock investors get no promises that a company will ever earn enough to produce a dividend. Investors typically bake that risk into the market price of stocks, so that they can hope to be compensated with a higher return than they'd get on bonds. Historically, stocks have earned about 4.5 percentage points per year above bonds. Stock investors have on average been paid for risk — but that doesn't mean you'll always get paid for risk. Case in point: The nearly 50% loss investors took on blue chip stocks in the wake of the financial crisis.

If you get that, you have the baseline knowledge you need to build a diversified portfolio and stick with it. The potential for loss is built into stock investing and you only make money if you are willing to live that. The rest is (usually expensive) fiddling around the edges.