How 2% Explains the World

Nervous investors looking for safe holdings have driven benchmark Treasury yields close to 2% again. These ultralow interest rates don't just make the bond market a tough place to earn money. They signal what could lie ahead for your whole portfolio, and the economy, in the years to come.

Warren Buffett made a commonsense call in early 2009. Bonds were the new bubble, the famed investor said, comparable to the recent dotcom and housing manias. The yield on a 10-year Treasury, a standard benchmark for the market, had fallen to 3%, less than half the previous three-decade average of 7.4%. Bond yields fall when investors pile in and push prices higher. Conversely, investors stood to lose money if bond interest rates moved back up to normal. At 3%, where else could rates go but up?

Flash-forward six years. Treasury yields are …2.1%, and it turns out sideways and even down are real possibilities for rates. That's proved to be a hard lesson. In 2011, Bill Gross, then manager of Pimco Total Return, the planet's then-biggest bond fund, sold all of the fund's Treasuries on a bet that rates would rise. Gross ended up with his worst year relative to his peers. One day this past October, the price of a 30-year Treasury quickly and briefly shot up 5% in value. That huge rally, by bond standards, was probably amplified when hedge fund managers who had bet against Treasuries had to race to reverse themselves.

All told, if you stuck to a plain-vanilla intermediate-term bond index fund, you earned an annualized return of 5.8% over five years. Cash made almost nothing in that time.

Even more striking than those numbers is that some vivid crash scenarios failed to materialize. The Federal Reserve's aggressive monetary easing, for one, didn't stoke runaway inflation, which would have forced up yields. Yet as Bonnie Baha, head of developed-market bonds at the fund company DoubleLine, points out, "Every single day of every single year for the past five years you could have turned on CNBC and someone would have said, 'Rates are going to rise, rates are going to rise.'"

That's because many investors remain mentally anchored to the inflationary 1970s and early 1980s, when rates hit double digits, Baha thinks. "People are pattern-driven, storytelling creatures," she says.

Of course, it would be just as dangerous to tell yourself a story in which recent returns forecast the future. A 2.1% yield on Treasuries is extremely low. Thin payouts have pushed investors to take on more risk. And managers like Baha and the others you'll meet in this story are trying to navigate a market—and a global economy—that's not like any other they've seen.

Talk to the pros who spend long days studying yield curves and default rates, and you learn some things that matter even if you aren't trying to time this inscrutable bond market. While the Dow Jones average or Apple share prices capture the headlines, the bond yield can be a window on what's happening in the economy and what you can expect in the future for your whole portfolio. Nothing in the picture is certain, and a lot of it isn't pretty. But if you're saving to retire, build a business, or send a kid to college, you'll want to take a closer look at this 2% world.

The "No" Fund

Thomas Atteberry run the $6 billion FPA New Income Fund out of an office on Los Angeles's Westside. An odd fact about the bond world is that many of the top managers, including Pimco and DoubleLine, are located in Southern California. But if FPA's location is near to the heart of things, its views on bonds are way off the beaten track.

FPA's website features a picture of a child drawing the one-word graffito "No" on a brick wall. Since before the financial crisis, Atteberry has mostly been saying no to the bond market. He's kept New Income's "duration"—a measure of how much a fund can lose on its bonds if rates rise—very low, making it one of the more consistently bearish general-purpose bond funds.

By way of explaining his position, Atteberry, dressed business-casual in jeans and a striped dress shirt, prints out a historical chart of rates on long-term bonds. "I find pictures help a lot," he says. He points to the troughs, and highlights, yes, a pattern. It's hard to miss. "Only a handful of times do you get something like [today's] number—actually only one," he says. He's drawing attention to the years around World War II, the one other long period when interest rates bounced around near 2% before they then climbed for 25 years.

It's probably helpful to pause for some bond market basics. How can someone be "bearish" or "bullish" on bonds? After all, a bond tells you from the get-go what you should expect to earn. It represents a loan from investors, whether to a company or a government, and is supposed to pay a fixed rate of return until maturity. At that point the issuer pays you back the principal—that is, the bond's face value. So why worry about losing money?

Part of the answer is that until the bond matures, it can be bought and sold in the vast global bond market, which at $108 trillion in value is twice the size of the world's stock markets. As rates change moment to moment—based on anything from expectations about inflation to minute shifts in Fed policy—the value of a bond adjusts so that the yield for a prospective buyer matches the new rate. Say you own a Treasury paying a coupon of 2.1%; if rates rise to 3%, which they touched in 2013, you have to cut your asking price for the bond until its effective yield equals 3%. If you're one of the relatively few investors who own individual bonds and hold to maturity, you may be indifferent to these fluctuations. But in mutual and exchange-traded funds, sharp movements in rates can translate into significant capital gains or losses.

One of New Income's goals, which is unusual for a fund, is to never show a loss over a 12-month period. Today's 2.1% yield is too little reward for the risk of going negative, says Atteberry. To avoid that, he has been holding mostly bonds that mature within three years. That's brought the fund's duration, or rate sensitivity, to 1.4, which roughly means that for every percentage point rates rise, the fund's portfolio value would drop 1.4%. By comparison, an index fund tracking the Barclays Aggregate index has a duration of 5.6. Over the past five years, Atteberry's conservatism has earned his investors a paltry 1.8% annualized total return—about even with inflation.

"Investors are willing to buy anything with a yield to it, in many respects because the Fed asked them to go do it." —Thomas Atteberry

It takes a strong worldview to hold on to that kind of contrarian bet, and FPA certainly has one. Robert Rodriguez, who ran New Income with Atteberry until 2010 and remains a managing partner at the firm, is a harsh, even angry, critic of government spending and Fed policy. ( Read a Money interview with Rodriguez in 2011 here.) He correctly warned of a housing-driven credit crisis before 2008, and the fund made money that year, while most bond funds fell. But Rodriguez also predicted that the government response to the crisis could trigger inflation, and he has said the federal debt load will cause rates to spike. So far none of that has happened.

Atteberry shares with Rodriguez a belief that the Fed may ultimately stoke a bubble. Right now, though, he isn't talking about inflation. Atteberry pulls more charts up on his computer. Economic inequality has held down income growth for most. The bottom 90% of Americans have essentially no savings. That restrains spending and, typically, inflation.

That actually makes low yields look a bit better. (If inflation is mild, a small yield goes further.) "But it also makes the economy look worse," says Atteberry, and that's bad news for another part of the market, corporate bonds with low, or "junk," credit ratings. These bonds' higher yields often protect them when Treasury rates rise, but a slow economy raises the risk of defaults.

Atteberry owns some junk, but his low-growth, low-yield outlook means "the marketplace is not offering much," he says. He sums it up: "When I was paid to take risk, I took it. I don't get paid to take that risk today." Until rates rise, FPA New Income investors are going to live with low returns and wait for better yields.

The Big Question of QE

Lurking behind any discussion of where bond prices are headed is the unusual role of the Federal Reserve in the markets since 2008. After the collapse of Bear Stearns and Lehman Brothers, the Fed cut the short-term interest rate it controls to essentially zero to keep the economy alive. Rates have stayed there ever since. The central bank went even further, buying up trillions of dollars' worth of longer-maturity Treasuries, as well as bonds backed by mortgages, in a program called "quantitative easing."

Economists and historians will debate how well QE worked. But it looks as if the Fed's buying helped push down interest rates on Treasuries, encouraging investors to seek higher returns in riskier stuff like corporate bonds and perhaps stocks. Lower corporate bond rates helped companies shore up their balance sheets, and the signal from the Fed may have made investors more optimistic.

In October, though, the Fed announced it had finally stopped buying up new bonds, the beginning of the end of the QE era. For bond investors now, the worry is this: Was QE a short-term, artificial sugar high for the markets? And if so, without it will longer-term rates come roaring back up?

The difficulty with the "artificial" argument is that there are a lot of reasons besides the whims of Fed chair Janet Yellen and her predecessor, Ben Bernanke, for long-term rates to be low. "I used to be really concerned about the U.S. rates and the Treasury market because I was thinking too small," says Elaine Stokes, a co-manager, with Dan Fuss and Matt Eagan, of Loomis Sayles Bond, which is on the Money 50 list of recommended portfolios. Stokes is no Treasury bull: She thinks rates are bound to rise. But Stokes says some big global trends could keep a lid on how high interest rates go. "Transitions take a long time, and this is not like any of the rate cycles we've seen in the past 30 years," she says.

Jobs are finally coming back in the U.S., but Europe and Japan still have huge economic problems. Because weak growth and low rates generally go together, and investors expect European and Japanese policymakers to cue up their own versions of QE, some overseas rates have fallen even more sharply than Treasuries. The 10-year German government bond, for example, yields only 0.6%. That essentially exports low rates to the U.S., as foreign investors buy up Treasuries. "Our 2% or 3% looks cheap next to Japan and Europe," says Stokes.

At the same time, America is aging. "We're a month from the last baby boomer turning 50," notes Stokes, speaking in her Boston office. "That's going to change things." With more people retiring and the workforce growing more slowly, companies don't need to invest as much in factories and machines. According to a theory gaining favor among economists, this means less demand for borrowing, holding down rates. Japan, where the trend is worse (the workforce is actually shrinking), hasn't cracked 2% on government bond yields since 1999.

"Europe and Japan are holding everything down. It doesn't look like that's going away soon." —Elaine Stokes

Unlike FPA, Loomis Sayles Bond is willing to place bets that can lose money—sometimes a lot of money. In 2008 it fell by more than 20%. (It up made that loss the next year.) But Stokes echoes Atteberry's concern that there's not a lot of compelling value left in the bond market.

QE has helped draw investors into lower-quality corporates. Loomis Sayles Bond rode that wave, earning more than 8% annualized over the past five years. Now, Stokes says, that has largely played out. And the lower yields also make the bonds vulnerable if rates rise. "In every area where we're invested," says Stokes, "it feels a little bit stretched."

Irrational Gloominess?

In January, Yale economist Robert Shiller, who shared the Nobel Prize in economics in 2013, is publishing the third edition of his classic book Irrational Exuberance. Some might take this as an ominous sign. The first version came out in 2000, and it made the case that stock valuations looked awfully high, and that people seemed too optimistic about tech stocks. You know what happened next. The second edition, published in 2005, had a new chapter about the unusually high price of real estate. This new edition adds a chapter on—you guessed it—bonds.

In a phone interview, Shiller demurs from applying the B-word to bonds. "It doesn't clearly fit my definition of 'bubble,'" he says. "It doesn't seem to be enthusiastic. It doesn't seem to be built on expectations of rapid increases in bond prices." In the unlikely event you meet anyone at the proverbial cocktail party talking about bond funds, he's probably complaining about the lousy yields, not talking about the killing he expects to make.

Still … Shiller does point to one similarity between today's low yields and past bubbly episodes. Bubbles are a result of a psychological feedback loop: As asset prices go up, people come up with stories to explain why, which helps push prices higher, reinforcing the story, and so on. In the tech boom the story was of a new era of dotcom-fueled growth. The rationalizations about housing prices centered on cheap mortgages and financial "innovations."

With bonds, too, says Shiller, "there are theories that have been amplified by the price performance." The low-rate story driving bond prices, however, is a gloomy one. If inequality, troubles in Europe and Asia, and bad demographics weren't worries enough, you can even add robots. "There's a suggestion that computers are going to create a more unequal world, and that this is inhibiting people's spending plans," says Shiller. Instead consumers try to save more, bidding up the prices of assets.

The idea of an economy that never quite gets back to prosperity has been labeled "secular stagnation" and the "new normal"—the latter term popularized by Bill Gross, before he made his surprising turn away from Treasuries. (Gross recently left Pimco for Janus; he declined to be interviewed for this story. Here is a 2010 interview with Money in which he discussed his "new normal" view. )

The "new normal" story is at least partly built into today's bond prices. Shiller also points out that his research with Wharton economist Jeremy Siegel has shown that bond investors are pretty bad at anticipating inflation. Forget fever dreams of ′70s-style price hikes—a return to 3% inflation would render Treasuries a money loser in real terms. (Inflation is below 2%.) That doesn't seem like such a high bar to clear. It's what some economists think a healthy economy would look like.

That said, the slow-growth, mild-inflation scenario remains compelling. The last time rates were this low, a spike followed—but that coincided with postwar expansion, Cold War defense spending, and the baby boom. Maybe that was the anomaly.

The assumption of continued low rates has probably been even more important, says Shiller, in driving up stock prices. With yields on bonds so meager, investors may have shifted money into stocks in hopes of getting a better return. In early versions of his new edition of Irrational Exuberance, Shiller described today's bull market as the "post-subprime boom."

"But I changed it at the last minute," he says. Now Shiller calls this era "the new normal boom."

Investing in a Low-Yield World

Bond managers have been employing a baffling array of tactics to make the best of this market: Atteberry holds bonds backed by auto loans and airplanes. DoubleLine says it's finding value in mortgages on commercial buildings. Julien Scholnick of Western Asset Management in Pasadena likes long-maturity Treasuries, which should do well if the recovery is followed by slow growth. Stokes' fund even owns some stocks.

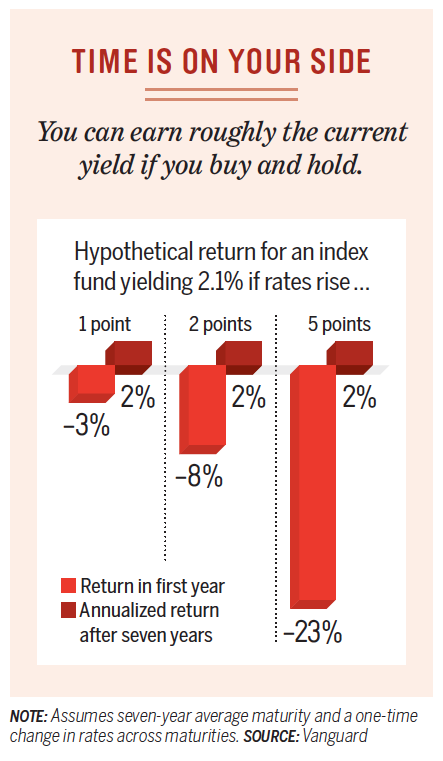

If you hold bonds as part of, say, a 401(k) plan, the most important thing you can do is understand your risk. A decline in the value of a fund that's the safe part of your retirement portfolio could come as a shock, and for money you may need soon, a short-term bond fund makes sense. But over the longer run a shift up in rates can also help make up for what you lost, and the current yield on bonds gives you a strong clue about what to expect.

Say you own a diversified bond fund. Assume the yield is about 2% when you buy it, and the fund's average bond matures in seven years. According to numbers from Vanguard, a sudden two-point jump in rates would cause the fund to lose about 8%. As its bonds paid out higher yields, however, your annualized return after seven years would be likely to level off to just about 2%.

Of course, this hypothetical assumes an indexlike, consistent portfolio, which you might not get in an actively managed bond fund. Brent Burns, president of the investment adviser Asset Dedication, says the low-rate environment is pushing some managers to take bigger bets. And the wagers can be risky, even in Treasuries. The 30-year bond went up over 25% in 2014, notes Gibson Smith, chief investment officer for bonds at Janus. That also means "it could have been negative 25%—that type of volatility," says Smith.

The real risk with bonds today, however, is not losses. It's that the returns stay frustratingly low.

Ben Inker, co-head of asset allocation at GMO, a Boston fund manager, lays out two scenarios, one he calls "purgatory" and the other "hell." In purgatory, economic growth picks up and rates are headed for a spike. Bond prices will fall, and stocks might too. But after that you pick up better yield.

"Investors are finding it hard to get used to such a low yield. But they’re going to find it hard to get used to slow growth—or what we at Pimco call the new normal." —Bill Gross, in a 2010 Money interview

In hell, secular stagnation is a reality. Your bonds don't lose money, because rates stay low. And today's stock prices, oddly, might make sense too. Here's why: When the price of stocks is high relative to past earnings, future returns tend to be lower. Today the P/E ratio for stocks, as Shiller measures it, is expensive at 27. (The average is 17.) So stock returns may be on the low side. You still may be willing to take that deal, however, if you are earning only 2% on your bonds.

That may help explain why stocks have recently shot up. If so, that's a one-time adjustment. Hell is not just a low-bond-yield world. It's a low-total-return world—and the economy is lousy too.

That would be bad news for savers, especially younger ones. In the hell scenario, a typical portfolio earns 3.4% after inflation instead of the 4.7% Inker assumes you'd have gotten in the past. "Let's say you turned 25 in 2009 and started saving," he says. "You end up accumulating 25% less by retirement."

Inker stresses he doesn't know which scenario we're headed for. The one constant is that in neither are there lots of opportunities to make money with low risk. "This is a frustrating environment for us as investors," admits Inker. "It is less clear what the right thing to do is than throughout almost the rest of history." The trouble with bonds, it turns out, is bigger than unpalatable yields. And it's the trouble with an economy that is taking a long time to find its true normal.