Where to Find Real Stock Bargains Now

- The Dow Just Hit a Record for the 23rd Time This Year — but Hold the Applause

- As COVID-19 Vaccine News Boosts the Stock Market, Here Are the Biggest Winners (and Losers)

- Trump's Positive COVID-19 Test Is Rattling Markets. Where Are Stocks Headed Next?

- Protests Are Raging in America's Biggest Cities. So Why Is the Stock Market up?

- Coronavirus Continues to Tank the Stock Market. Here's Why — and What To Do About It

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

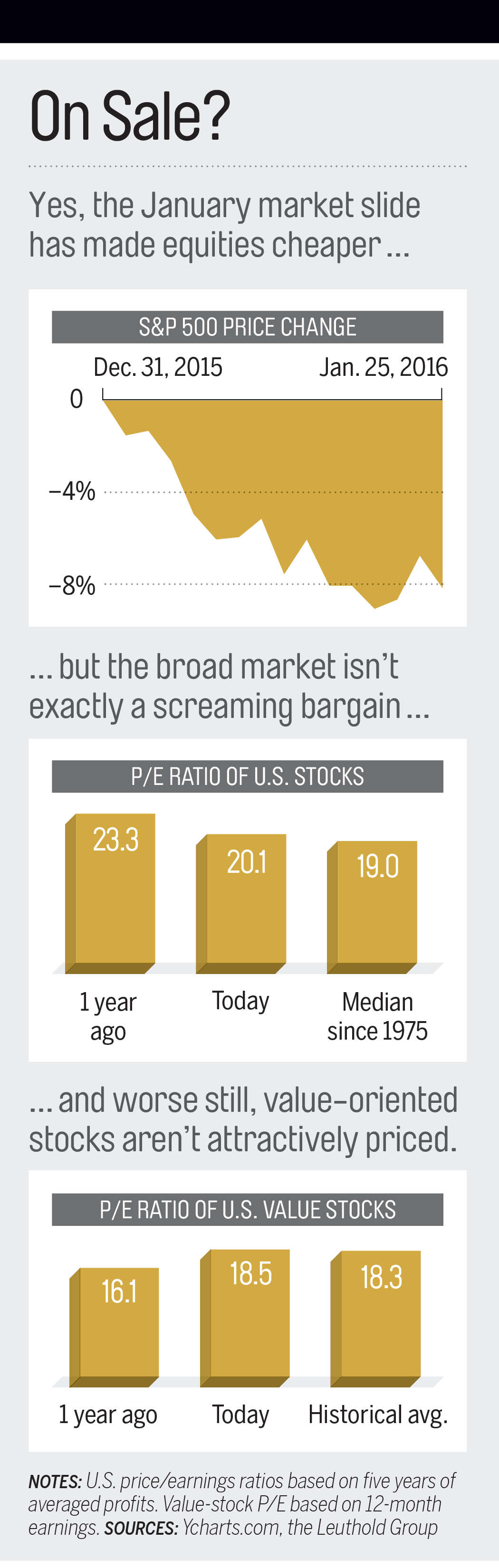

The January market slide certainly marked down a lot of prices: Blue-chip stocks were off nearly 10% from their 2015 highs, the mark of a correction; small-company shares have lost more than 20%, which is technically a bear market; and oil prices have been cut in half, signifying a holy mess.

Just because something is discounted, though, doesn't make it a great deal. As Warren Buffett likes to say, "Price is what you pay; value is what you get." And despite how scary the pullback was — the Dow plunged nearly 2,000 points from Dec. 29 to Jan. 20 — the price/earnings ratio of U.S. stocks is still 5% higher than the median since 1975, based on five years of averaged profits (see chart).

Historically, betting on beaten-down equities has proved to be a smart move, as so-called value stocks have outpaced shares of faster-growing companies three-fifths of the time since 1928.

But as seasoned investors like Buffett will tell you, bargain hunting requires finding shares that are genuinely undervalued relative to fundamentals such as earnings. Then you must have the patience to reap the rewards. Here are four strategies to help navigate today's cheap-looking but tricky market.

Actively Search for Bargains

Simply buying the broad market after the pullback won't ensure winning returns, says Daniel Hughes, vice president at Vaughan Nelson Investment Management. Even value-stock indexes are trading at higher-than-historical valuations. "You can't just look like your benchmark," Hughes says.

One alternative is to seek out bargain-hunting fund managers who are willing to stray from the herd. A 2015 study from researchers at Notre Dame and Rutgers found that managers who took big index-deviating bets — and held their stocks for at least two years — beat the market by two percentage points a year.

A value-minded fund that fits the bill is Oakmark Select . Oakmark's team of managers, led by William Nygren, certainly pays attention to value: Shares in the fund's portfolio trade at an average P/E of about 15 based on forecasted 2016 profits, which is lower than for value stocks as a group.

But the fund's managers also give themselves the freedom to bet on stocks outside the classic value mold. These are companies like software giant Oracle , which despite fast growth trade at reasonable valuations. In a decade in which the average value-stock fund has returned 4.5% annually, Oakmark has returned 5.4%.

Energize Your Portfolio

Common sense would tell you that the best way to find real bargains is to focus on the most-out-of-favor areas of the market. That certainly worked after the financial crisis, when beleaguered bank stocks rebounded — and trounced the broad market by 50 percentage points over the next seven years.

The problem, of course, was few investors were brave enough to bet on banks in 2009 while the mortgage crisis was still unfolding.

Today nothing is scarier than energy. It was only two years ago that crude oil was trading at more than $100 a barrel and energy companies were posting near-record profits. But those high prices drove innovation, and new developments such as fracking added to supplies just as demand from energy-thirsty emerging-market economies such as China began to slow. That one-two punch pushed oil prices below $30, dragging energy stocks down 40%.

Oil may still be in for a bouncy ride in the coming months. But investing is about the long term — think decades, not years. Eventually prices will rebound, but you have to buy before they do.

Keep in mind that global demand for oil has merely slowed, not shrunk. Meanwhile, Americans are sopping up cheap gasoline: Last year, car sales set a record, with gas-guzzling pickups leading the way. This type of behavior will help suck up oversupply, says William Blair portfolio manager Brian Singer. "People will produce less oil and use more of it, and eventually prices will find an equilibrium," says Singer, who puts oil at $45 in the next two to four years.

While you're waiting, you can minimize risks in a couple of ways. For starters, focus on low-cost sector funds, like iShares North American Natural Resources ETF . This portfolio, which is on our Money 50 list of recommended mutual and exchange-traded funds, owns more than 90 energy stocks, ranging from drillers to oil-services firms to pipeline operators. This way, you don't have to guess which group will recover the fastest.

A smart way to bet on oil's recovery — with greater chance for growth — is not through a sector fund but with a regional portfolio. So-called frontier-market funds invest in small but fast-growing economies, many of which are tied to oil production. For instance, iShares MSCI Frontier 100 ETF holds nearly 23% of its assets in companies based in oil-rich Kuwait and another 11% in Nigeria.

Overall, less than 10% of the fund is directly in energy. The bulk of the fund is invested in financial, telecom, and consumer companies whose customers will benefit from rising oil prices. The result: an average earnings growth rate of 14%, vs. 8% for energy funds.

The ride can still be wild. Shares of this ETF are down more than 21% over the past year, vs. a 37% decline for the average energy stock sector fund. However, over the past three years, Frontier 100 has lost 2% annually, vs. the 16% decline for energy funds.

Focus on Quality Too

Betting on beaten-down stocks is generally regarded as a conservative strategy, since it involves buying shares that are already down. But it's not without risks. For starters, there's the market itself. While most economists don't think the U.S. economy is headed for a recession this year, stock declines are often seen as a leading indicator of economic trouble. And at around 75 months, this expansion is the third longest since World War II.

If the economy is indeed slowing, bargain hunters may face another bout of pain. Recent research by Russell Investments found that value stocks typically lag in the 12 months prior to a recession's trough. It's only after the economy starts expanding that value tends to leap ahead.

So how do you ride out a possible storm while still adhering to this strategy? Go with undervalued shares of high-quality companies. Quality stocks — shares of businesses with attributes such as strong but steady profit growth and relatively little debt — tend to outperform in the long run with less of the volatility associated with lousy economies.

A good way to capture these stocks is through a fund such as PowerShares S&P 500 High Quality ETF , which is on the Money 50 list. Among the fund's top holdings are Walmart and Union Pacific , whose shares are down more than 20% since 2015.

Over the past five years, SPHQ has lost about 25% less than the market in months when stocks have fallen. Yet during that same stretch, the fund has beaten 99% of its peers.

Seek Bargains in Another Way

If you embrace value investing, you have to be in it for the long haul. While bargain hunting wins out over time, this strategy can lag for years. In fact, value stocks have trailed shares of fast-growing companies by two percentage points annually over the past decade.

This doesn't mean you should turn your back on value, especially now that the strategy itself has been beaten down for so long. But you can make the wait more tolerable by trimming your investment fees, which are a drag on returns.

The average large value-stock fund charges 1.11% of assets in fees a year, according to Morningstar. Yet in recent years there has been a profusion of low-cost index funds and ETFs that give you exposure to various aspects of value.

In the Money 50, a good example is PowerShares FTSE RAFI U.S. 1000 , which charges just 0.39% a year. It offers exposure to the broad market but keeps larger stakes in value-oriented shares. Over the past decade the ETF has returned 6.7% annually, which is 2.2 percentage points better than the typical value fund.