Is debt relief legit?

You may have heard it called "credit card forgiveness" — here's what it actually is, and whether it's right for you.

If you're carrying five-figure unsecured debt and the minimum-payment treadmill isn't moving the balance, debt relief is one of a handful of real options. Below is what these programs actually do, what they won't do, how the FTC regulates them, and the providers we've vetted for 2026.

How debt relief actually works

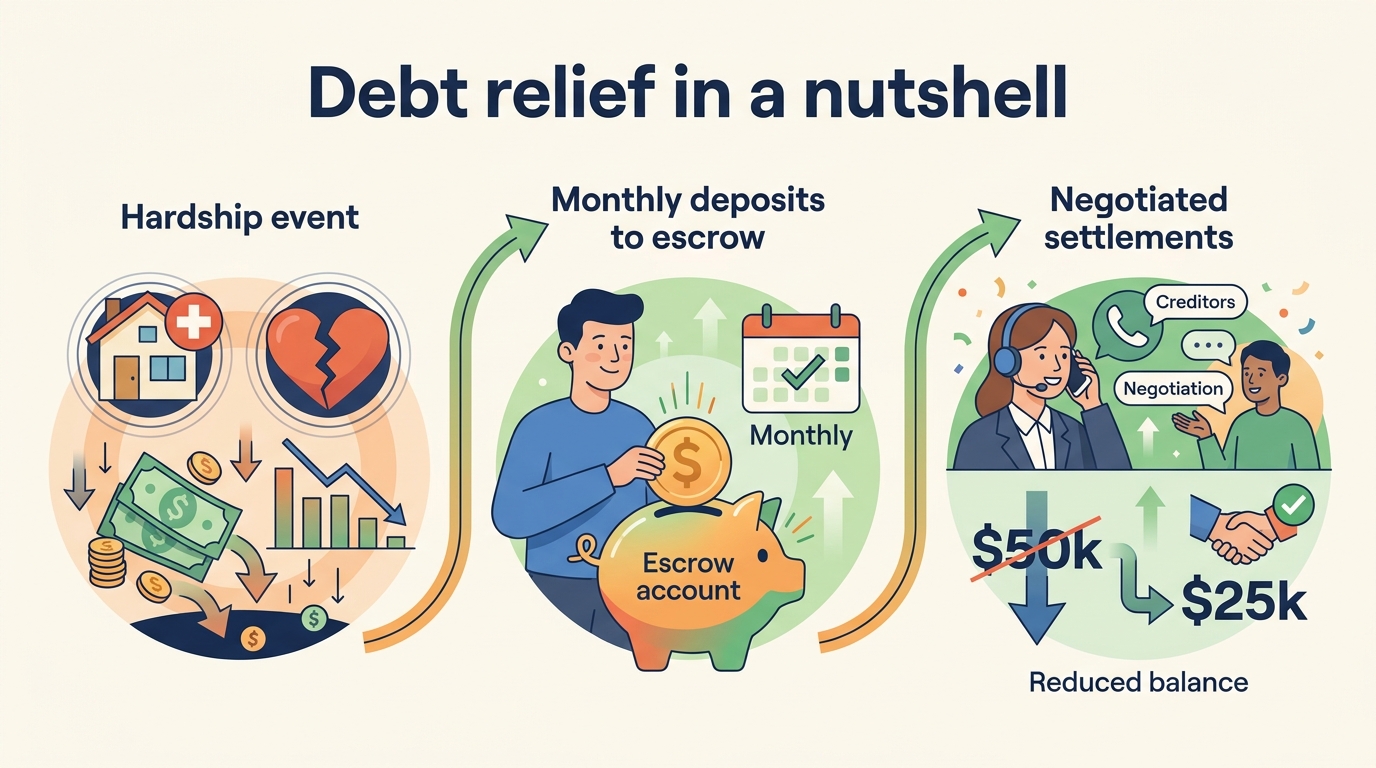

Most people don't end up in a debt relief program because they overspent on a vacation. The trigger is usually a hardship event — job loss, a medical bill that ran past insurance, a divorce, a small business that didn't make it. Balances grow, minimum payments climb past what the household can carry, and the interest math takes over.

The mechanics of the program itself are straightforward. You stop paying your creditors directly and start depositing a single fixed monthly payment into a dedicated escrow account in your name. As that balance grows, the relief company contacts each creditor and negotiates a reduced lump-sum payoff — typically when an account is far enough delinquent that the creditor would rather settle than sell the debt or take you to court. The company pays each negotiated settlement out of your escrow, then takes its fee from the savings.

Most programs run 24 to 48 months from start to last settled account. Faster programs are usually the result of larger monthly deposits, not better negotiation.

What keeps the industry honest is one specific federal rule. The FTC's Telemarketing Sales Rule, amended in 2010, prohibits any for-profit debt relief company from collecting a fee until a debt has actually been settled and the consumer has made at least one payment under the new arrangement. That's the entire reason "no upfront fees" became the industry standard. It's also the single fastest way to identify a scam: any company that asks for a deposit, retainer, or service fee before negotiating a single account is operating outside the law.

Compare Top Debt Relief Companies

Freedom Debt Relief

- ✓Fast & easy online registration with 24/7 customer assistance

- ✓Free, no-obligation evaluation

- ✓Low monthly payments with no upfront fees

- ✓A+ rating from the BBB

Free consultation · No upfront fees

National Debt Relief

- ✓Fast and easy application process

- ✓No upfront fees

- ✓Free consultation, 100% confidential

- ✓Become debt-free in 24 to 48 months

Free consultation · No upfront fees

JG Wentworth

- ✓100% FREE initial consultation

- ✓Customized options to fit your needs

- ✓One affordable monthly program payment

- ✓33+ years experience in financial services

Free consultation · No upfront fees

What it does — and what it doesn't

What it can do

- ✓Reduce the principal owed on enrolled debts — settlements typically land at 40% to 60% of the enrolled balance, before the relief company's fee

- ✓Consolidate negotiations across multiple creditors into a single monthly payment to escrow

- ✓End the cycle of collection calls once accounts are placed under the program

- ✓Provide a documented alternative to bankruptcy when bankruptcy isn't the right fit

What it won't do

- ✕Protect your credit score during the program — expect a meaningful drop, with recovery starting once accounts are settled

- ✕Touch federal student loans (not eligible — federal repayment plans and forgiveness programs are the alternative)

- ✕Eliminate secured debts like mortgages and auto loans (the collateral is the issue, not the balance)

- ✕Stop a creditor from suing you mid-program — only a bankruptcy filing creates an automatic legal stay