Here's Why Carl Icahn Wants Apple to Buy Back Shares

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

Investor Carl Icahn has sent an open letter to Apple's CEO, Tim Cook, with lots of nice things to say about the iPhone 6 and the Apple Watch. But also this: He'd like shareholders to get paid, please, and faster.

Icahn controls 53 million shares of Apple, worth $5.3 billion, which gives him about a 0.9% ownership in the company. In his letter, Icahn lays out his reasons that Apple should repurchase its own shares.

The basic logic of a share repurchase is that it returns some of a company's cash back to its owners. Unlike a dividend, in which a company just writes a check to shareholders, the return of cash is indirect. (Icahn is careful to say that he won't sell his shares to Apple if the company makes what's called a tender offer to buy shares.)

But by reducing the number of shares outstanding among which a company's earnings and assets have to divided, a buybacks can make each share of a stock worth more. That's assuming, of course, that investors think giving money back to shareholders is the wisest use of the company's cash. A buyback can backfire if it leaves a company unable to invest in future growth.

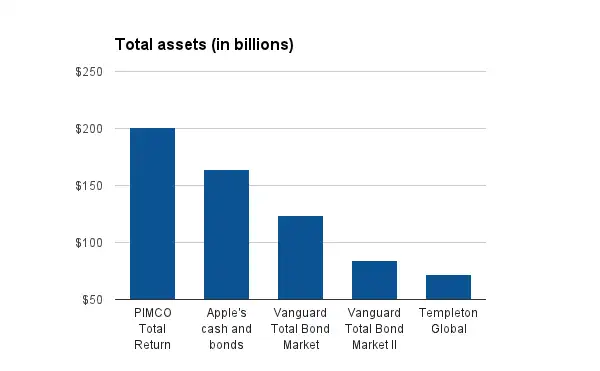

Apple has a lot of cash. Or, technically, cash plus other short-and long-term investments. The point is that this is money not currently tied up in Apple's business, but sitting in a portfolio. The Icahn argument, essentially, is that no one needs Apple's expertise as a de facto fund manager. As Money wrote back in June, add up Apple's $164 billion portfolio and it's bigger than any U.S. bond mutual fund beside the giant PIMCO Total Return.

Icahn argues that all this comparatively low-returning cash is a drag on Apple's shareholder return, and that some investors are less willing to hold the stock as result. He points out that if you subtract Apple's net cash, it trades at a price/earnings ratio of just 8, a significant bargain at a time when the average S&P stocks is priced at 15 times earnings.

Icahn is what's known on Wall Street as an "activist" — a big investor who comes into a company and starts demanding changes aimed at increasing the share price.

As we explained recently, such investors (who used to go by less friendly names like "raiders") have become a powerful force in corporate America, and not always with happy results.

Few companies have a giant cash cushion like Apple. Activists often push companies to increase value to shareholders by splitting up, selling off assets, merging or loading up on debt. This may increase the share price — though not always — but it can also mean lost jobs and the disappearance of once-great companies.

Icahn's less than 1% stake might not seem like much, but Icahn is deft at using his position to rally other investors to his side. He's public about what he wants for a very good reason — when he comes into a stock and starts talking about ways the company could enrich shareholders, other investors follow. That alone can help boost the share price, as well as building a constituency for the changes he's demanding.

Indeed, in the time since Icahn disclosed his position in Apple, Cook has pledged to return $130 billion in capital, in the form of dividends and repurchases by the end of next year. Icahn's mostly won this argument. His letter is a nudge to Cook to keep it moving.