3 Signs That You Should Be Dumping Your Stocks

- 5 Biggest Trends That Will Affect Your Money in 2018

- How to Bet on Amazon Without Actually Buying Its Insanely Expensive Stock

- Dividend Stocks No Longer Pay. Here's a Better Way to Invest

- Busting the Myth That Gold Is a Good Investment

- How You Can Hang Onto a Small Company That Grows Up To Be a Big Winner

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

In most cases, you shouldn't listen to those little voices in your head, especially when they tell you to sell long-term holdings. But "with valuations where they are, and with the world in the condition it's in, I don't know any investor who isn't asking whether they shouldn't move at least a portion of their assets outside of the stock market," says Fidelity Investor editor Jim Lowell.

If you're investing for goals that are more than a decade away, the answer to that question is a definite "no." But there are times when it's perfectly reasonable to take some chips off the table. Here are a few of them:

• If you haven't touched your account in years. Let's say you put $60,000 in the Vanguard Total Stock Market Index fund (VTSMX) and $40,000 in Vanguard Total Bond Market Index (VBMFX) eight years ago, having decided back then that a 60% stock/40% bond mix was appropriate for your goals. You then spent the next eight years in a cave in Nepal.

Upon your return, your portfolio shifted to 80% stocks/ 20% bonds. At this point, it's time to rebalance, or sell enough from your stock fund to replenish your bond stake to get back to your original 60/40 approach. You may lose something in future gains, but you'll be at a risk level that keeps you from waking up at night shouting, "I'm ruined!"

As a rule, rebalance when your mix shifts by 10 percentage points or more.

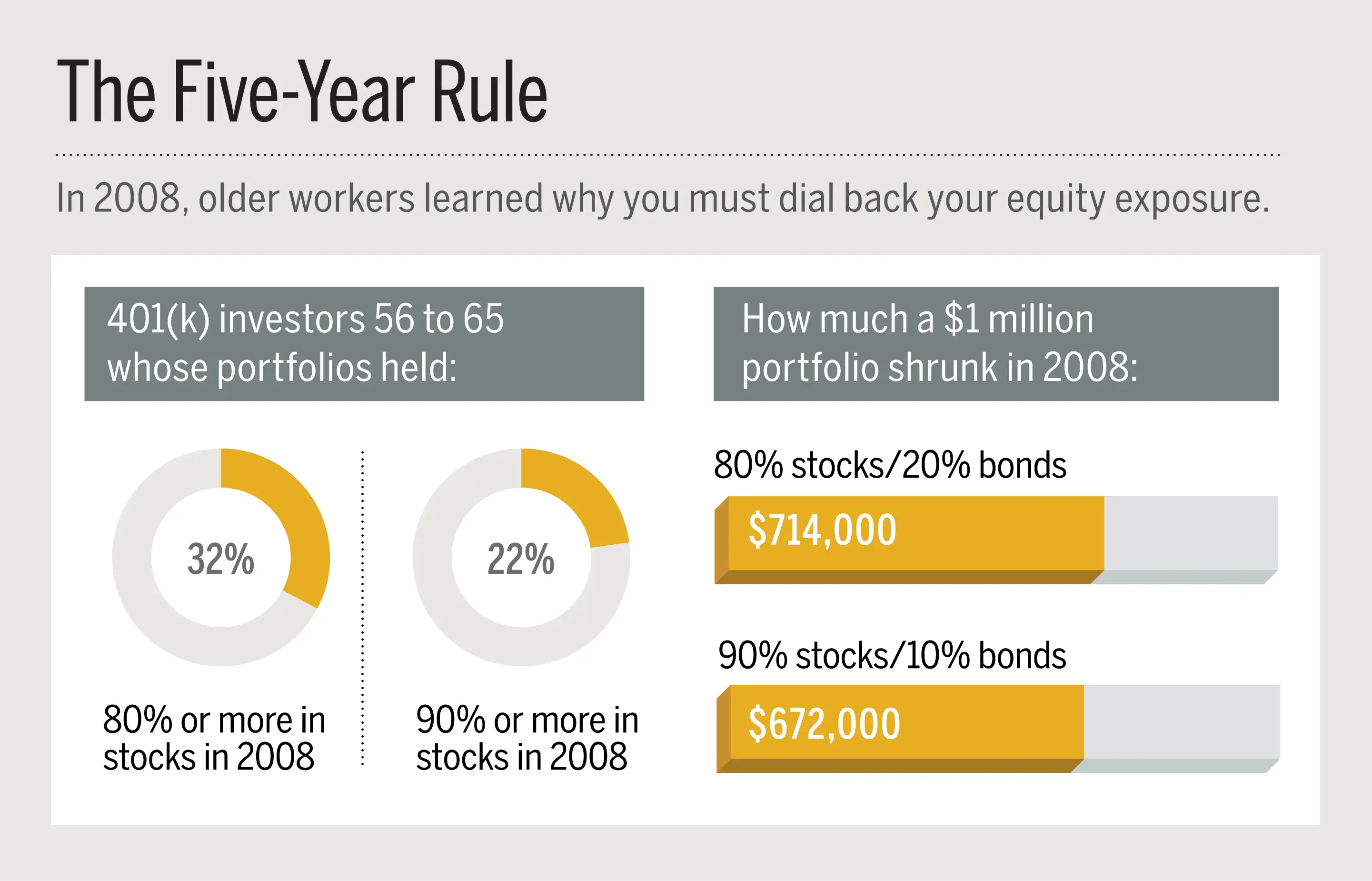

• If you're within five years of hitting a goal. Another reason to take chips off the table: You're closing in on your goals.

Let's say you need $2 million to retire comfortably, and five years out, you're at, say, $1.9 million. If you're 80% in stocks, you can probably cut your exposure and still make your goal.

Even if you're not that close, you still must take your foot off the pedal. Don't and you'll fall further back in a downturn, with too little time to recover.

• If you're fearful, but don't fall into these camps. It never makes sense to sell in a panic. But you don't have to quit stocks altogether. A well-diversified portfolio holds different types of equities, including unloved shares. "Lower prices are one way to mitigate investment risks," Lowell says.

So go with "deep value" funds that invest only in extremely low-priced stocks (that are likely to lose less in a pullback) and that let their cash levels rise if they can't find good shares to buy.

One good example: American Beacon Bridgeway Large Cap Value (BWLIX), which holds more cash than its peers but still ranks in the top 10% of its category over the past five years.

The worst reason to sell? Some friend tells you to.

"Going to cash is one of the holy grails of the investment bible," Lowell says. "But there's no Holy Grail in the real Bible, and any claim I've seen about going to cash and getting back in hasn't been true, either."