Is a Continuing Care Retirement Community Right for You?

As you think about an ideal home for an older relative, or for yourself later in life, what seems most appealing?

Nearly 90% of people 65 and older surveyed by AARP said they would like to "age in place." And yet the hard truth is that a beloved house in a familiar community can become both physically impractical and socially isolating over time.

Another way you or your relative might get comfort, connections, and continuity is, surprisingly, by moving to a new spot: a so-called continuing-care retirement community (CCRC). These developments couple attractive condo-like living units with fancy communal dining rooms, add-ons like tricked-out gyms, and busy rosters of activities to keep residents engaged. They also deliver peace of mind by including facilities the prospects hope they won't need: assisted-living and skilled-nursing units on the same campus.

CCRCs can mean fewer worries for adult children as well as residents by eliminating a scramble for care after an acute health problem, says Lisa McCracken, a senior vice president at Ziegler, an investment bank that specializes in not-for-profit senior housing. And for the fewest financial worries down the road—assuming, that is, you have the cash now—you can essentially prepay for whatever future care you end up needing.

"The CCRC concept is the most dependable way for people to provide for their own old age," says Jack Cumming, the director of research for the National Continuing Care Residents' Association, an advocacy group for CCRC residents. But, warns Cumming, himself a resident of a California CCRC at age 80, "there are few standards or regulatory safeguards that a prospective resident can look to as assurance that a particular CCRC is all that the marketing staff presents it to be."

That's no small thing given the huge commitment that's involved, both financially and in terms of leaving your current home. Here are key questions.

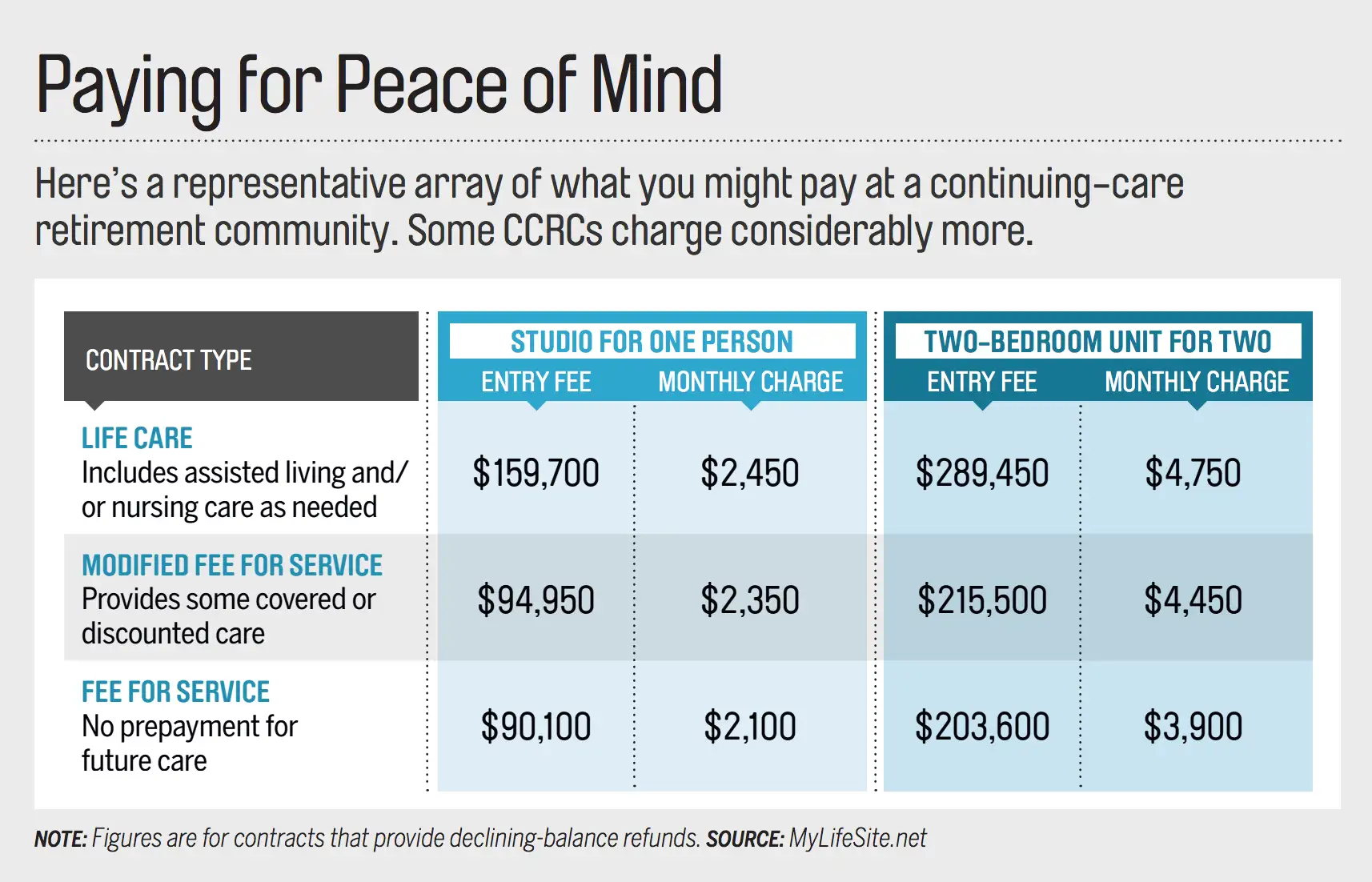

What do you get at a CCRC?

At the core of every CCRC is independent living in cottages or apartments. Each community includes at least one level of care, such as assisted living, and many provide a full range of assisted-living, memory-care, and skilled-nursing services. Residents segue to more care when needed. For couples, one spouse may move to a care unit while the other stays in independent living.

You'll typically be charged an entry fee. And there are monthly charges that usually include most activities and some meals in the dining rooms.

There are nearly 2,000 CCRCs, up 7.5% over the past 10 years, with a total of about 600,000 living units, according to Ziegler. Another 92 CCRCs are in the pipeline to open by 2019. You can locate CCRCs at LeadingAge.org, the website of an advocacy group that represents more than 6,000 senior-care nonprofits, and MyLifeSite.net, developed by a financial planner.

What will it cost you?

As you might suspect, this all-in-one living doesn't come cheap. Entry fees can range from the low-to mid-six figures, with monthly charges from $2,000 to more than $4,000. Costs vary widely among communities. And at any individual CCRC, you'll pay more—sometimes a lot more—if you select a larger independent-living unit or opt to prepay for more care.

Want to shield your future finances and your family from the costs of assisted-living or nursing care you might need as you get older? Opt for a life-care, or Type A, contract that will cover care on the campus as needed. This is the "gold standard," says Cumming, and so will require the largest entry fee. Type A can be especially smart for couples, who may sometimes have different needs.

To keep costs down, you can prepay for less care. A Type B, or modified fee-for-service, arrangement includes a set allotment—say, 30, 60, or 90 days—of covered or discounted care. If you have a long-term-care insurance policy, you could opt to pay even less for a Type C, or fee-for-service, contract. With that one, you are typically guaranteed access to future care but must pay the going rate at the time.

In one common design, a declining portion of the entry fee is refunded if a resident leaves or dies within a few years of moving in. For a much higher fee, you may be able to lock in a permanent refund for the resident or heirs of, say, 50% or 90%.

Can you afford to consider a CCRC? Many people cover the entry fee with the proceeds of a home sale. You'll need to compare the monthly charges with what you are paying now for housing and for whatever food and activity costs you might no longer face. Hiring a financial advisor for a one-time consultation might help. One resource is garrettplanningnetwork.com, whose members charge hourly fees; you might pay $200 an hour.

Is it a great fit for you now?

In evaluating a community, spend time on the campus; many CCRCs even offer overnight stays to prospective residents. Does the meal schedule work for you? Are you pleased with the food quality and selection? Peruse the list of activities and try out a few. What transportation is available if you're ready to give up the car?

The median move-in age at CCRCs is 81, and nearly two-thirds of new residents are single, according to a study by Love & Company, a marketing firm that specializes in retirement communities. Are you comfortable with the age range and mix of residents? Can you envision wanting to build friendships with the people you meet?

To emphasize that CCRCs are not depressing old-folks' homes, the industry has launched a push to rebrand as life-plan communities. "These are more about the living side of things than the care side," says Katie Sloan, president of CCRC association LeadingAge.

Is the CCRC a good fit philosophically? Eight in 10 are nonprofits, and many are run by religious organizations. Are you comfortable with the group's mission and inclusiveness? Check if the board of directors includes residents as voting members, a sign that management values resident input.

How well will it take care of you in the future?

Check out the assisted-living or nursing facilities or, at the very least, send your adult kids for a tour. Beyond the general feel of the facility, focus on the staff vibe: grumpy or engaged? Ask independent residents if they have spent time in the care units for an injury or illness or visited friends there.

If a CCRC has a skilled-nursing unit, look up its rating at Medicare.gov. Though not a perfect assessment, a five-star rating should boost your confidence. Brad Breeding, cofounder of MyLifeSite.net, also recommends asking the state long-term-care ombudsman if there are any complaints on file. (You can locate LTC ombudsmen at theconsumervoice.org/get_help.)

Is the CCRC financially solid?

If a CCRC isn't on solid footing, you'll run the risk of big monthly-fee hikes, a reduction in the quality of services or care, and delayed refunds. A financial adviser, CPA, or actuary might be able to help you make sense of a community's audited financial statements; you might ask an elder-care lawyer to recommend someone. Careful vetting is crucial because there is no federal oversight of CCRCs, and state regulation varies.

At MyLifeSite.net you can download a sample report that includes recommended levels of profitability, debt, and liquidity measures. CARF International, which runs an accreditation program for CCRCs, has free guides for consumers (carf.org/resources/retirementliving).

Empty units are a drag on a CCRC's finances, so look for an occupancy rate of at least 90%. As a benchmark, the current 92% average occupancy rate for nonprofits is nearly six percentage points above the rate at for-profit CCRCs, according to Ziegler. A waiting list to get in is a good sign too.

Ask if your upfront payment is being set aside as reserves for future care. "You don't want to hear that entry fees are primarily being used to cover day-to-day operational costs," says Breeding. He says a CCRC's transparency in answering your questions is an important signal. One red flag that should prompt further questions: any annual fee increases in the past five years that exceeded 3% or so.

Granted, this is all a lot of work. But if you find a CCRC that's the right fit, you may reap a valuable payoff: a vibrant life today and fewer worries for the future.