As investors, we all get things wrong from time to time. Just ask Irving Fisher, the once famous (now infamous) economist who declared in 1929 that equities would keep racing ahead, since the stock market had reached what he called “a permanently high plateau.” Eight days later the market plunged, setting off a series of declines, culminating in Black Tuesday—and, of course, the Great Depression.

While Fisher’s market call is now part of Wall Street lore, he’s hardly alone in making bad assumptions about stocks. At the end of last year, for example, most investors assumed that the tax cuts passed in Washington would fuel another round of risk taking on Wall Street, pushing the bull market ever higher.

Clearly, that hasn’t happened yet. Meanwhile, several things that investors assumed wouldn’t take place—like the return of worrisome levels of inflation or volatility—are starting to materialize.

This isn’t necessarily a big deal, so long as you adapt your thinking and strategy to reflect the new market reality. Investing success doesn’t require -prescience; it takes a willingness to acknowledge miscalculations and to make tactical adjustments accordingly.

1. Volatility Roars Back

The assumption

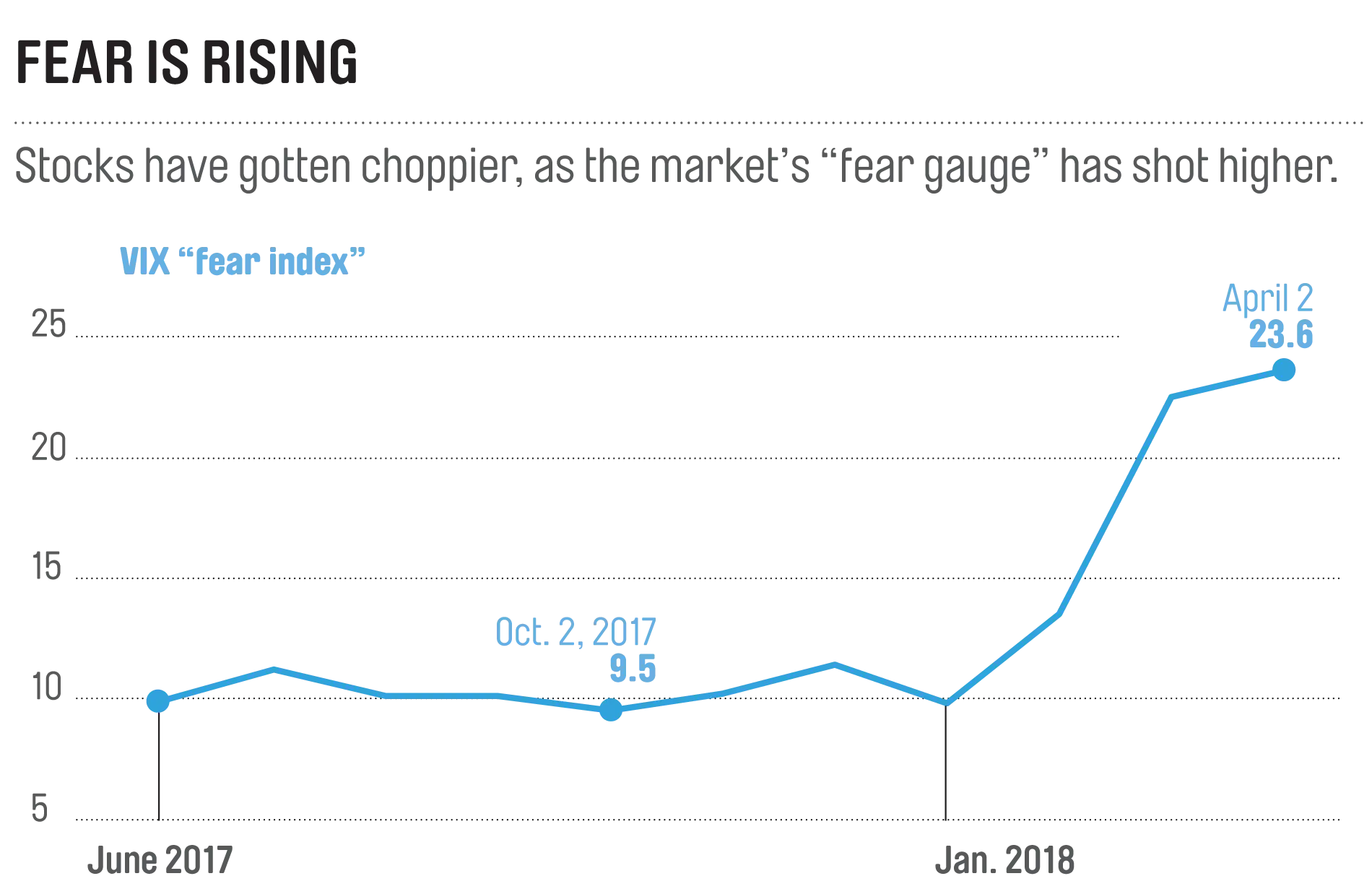

Fear isn’t what usually kills a bull market; it’s often the lack of fear, or that sense of comfort and confidence that leads investors to forget how risky investing can be.

Well, in 2017 investors were about as complacent as they’ve ever been. At the end of last year, the market witnessed 14 of the 20 lowest days in the history of the CBOE volatility index (or VIX), the so-called fear index that gauges investor anxiety. With an average reading of about 11 last year, it was only a matter of time before the VIX ticked back up to its long-term average of 19.

But while many market watchers argued that volatility was sure to pick up, few predicted market fears would jump to levels not seen since the recession of 2007–09, the global financial panic, or the tech wreck of 2000–02.

The reality

In just the first three months of 2018, the S&P 500 index experienced more daily swings of 1% or greater than in any year since 2009, according to DataTrek Research.

Blame the aging bull market, which is about three months away from becoming the longest rally in history. After a nine-year run, stocks have become historically expensive and are as overvalued as they’ve been since before the dotcom bubble.

A conservative way to gauge the level of froth in the market is to measure stocks’ price/earnings ratio, using 10 years of averaged corporate profits. The S&P 500’s Shiller P/E (named after Nobel Prize–winning economist Robert Shiller, who popularized its use) has just climbed above 31. That’s nearly double the historical median of 16.

As a result, investors are now “acting out of a position of fear instead of greed,” says Brad McMillan, chief investment officer at Commonwealth Financial Network.

This anxiety is shaking the market every time a new issue—whether it be talk of tariffs, rising inflation, a geopolitical crisis, or

a controversy at a company with a widely held stock like Facebook—hits the news. Individual investors are simply reacting day to day, and have yanked a net $56 billion out of U.S. equity mutual funds in the first three months of the year.

What you can do

Don’t panic just because Wall Street is starting to show some signs of consternation. As the saying goes, “bull markets like to climb a wall of worry.” Instead, use rising volatility as an opportunity to reevaluate how much risk you want in your portfolio, says Joseph Heider, president of Cirrus Wealth Management.

If you can handle a 10% or larger fall in the short term—such as the correction the market experienced in late February—then it’s fine to stay heavily weighted to stocks and keep buying as the market dips; you’ll gain more shares that way.

If such a drop is too discomforting, then consider dialing back your exposure to equities. This is a step many older investors failed to take before the global financial panic. At the end of 2007, nearly one-third of 401(k) investors in their sixties held more than 80% of their nest eggs in stocks—just in time for the 2008 market crash that erased 37% of the value of those equity portfolios.

Also, investors of all ages should consider using rising volatility to embrace low-volatility investing. “Low-vol” stock funds are filled with Steady Eddie–type stocks that tend to lose less when the markets fall (but gain less when stocks climb).

Low-volatility investing tends to be embraced in times of fear, but this strategy has actually outperformed the broad market over long stretches. Research Affiliates found that low-volatility U.S. stocks have outpaced domestic equities by more than 1.5 percentage points a year over the past 20 years. Meanwhile, low-volatility foreign stocks have beaten international equities by more than four points a year.

On our Money 50 recommended list, consider iShares Edge MSCI Min. Vol. USA ETF (USMV) for domestic exposure and iShares Edge MSCI Min. Vol. EAFE ETF (EFAV) for steady foreign stocks.

2. Inflation Fears Emerge

The assumption

Inflation, or rising prices on goods and services, hasn’t been a real threat to investors for more than a quarter-century. In fact, for the past decade, the Federal Reserve has been fighting to keep the opposite force—deflation—from wrecking the economy in the aftermath of the global financial crisis.

But with business activity finally picking up steam, the consensus forecast has been for a “modest increase” in inflation—modest being the operative word. A survey of economists late last year by the Federal Reserve Bank of Philadelphia found that forecasters were

banking on consumer prices rising at an annual pace of 2.2% this year, up from 2.1% in December.

The reality

In the first week of February, stocks plunged 9% after average hourly earnings for workers grew 2.9%. Not only was that the biggest annual jump in pay since 2009, it was also seen as an omen for overall inflation, since wages are still one of the largest input costs for companies. Then, in March, the consumer price index (CPI), the most-watched gauge of inflation, jumped 2.4%.

Still, inflationary fears remain muddled. Some economists, for instance, believe bad weather affected those wage growth figures, as a high number of snow closings may have impacted hourly employees in the workforce earlier this year. That, in turn, may have overweighted the salaries of higher-paid workers in the government data, says McMillan. By the end of March, some of those inflation fears were quelled, as wage growth decelerated to around 2.7% over the prior year.

On the other hand, another gauge of inflation, which measures the wholesale prices that manufacturers pay, has been heating up faster than the CPI. The producer price index (PPI) has risen 3% over the past year, a big jump from the prior year. And what makes this worrisome is that the PPI is seen as a leading indicator of consumer prices, since manufacturers get squeezed first and then must decide if they will try to pass the rising costs of materials such as steel and oil on to consumers.

What you can do

The threat of inflation shouldn’t necessarily scare you as an investor. Inflation is heating up, but it’s by no means historically high. Since 1926, inflation has averaged around 3%, and the CPI remains below that threshold.

Even if you think the CPI will soon hit that 3% mark, though, and interest rates will rise to reflect that, keep something in mind: The S&P 500 has returned about 10% annually during times of rising rates, according to Bank of America.

Nevertheless, it’s smart to consider inflation hedges before rising prices become a real threat and those inflation-protected assets become truly expensive.

David Blanchett, head of retirement research for Morningstar, notes that Treasury Inflation-Protected Securities (TIPS) are a hedge against unexpected inflation, since the underlying value of these bonds moves upward as the consumer price index increases. And that, in turn, boosts your actual interest payments.

Right now, the break-even rate for 10-year TIPS is about 2.2%. That means if inflation rises more than 2.2% for the next decade, you’re better off in TIPS than traditional bonds. In the Money 50, look at the Vanguard Inflation-Protected Securities Fund (VIPSX), which has beaten 80% of its peers over the past 15 years.

As for stocks, research from Charles Schwab finds that as inflation rises, the price investors are willing to pay for equities falls. Historically, the market’s P/E ratio has been 17.6 when inflation grows 2% to 3%. But when it climbs to 3% to 4%, the P/E drops to 16.

This is why investors should also focus their attention on low-P/E stocks. You can find them in Vanguard Value ETF (VTV) and PowerShares FTSE RAFI U.S. 1000 ETF (PRF), which are both on the Money 50. The average stock in both funds trades at a P/E ratio of 14.5.

3. The Fed Moves Faster

The assumption

The Fed has been slowly raising interest rates since December 2015—really slowly. Over the past 2½ years, the central bank has lifted rates by a modest 1.5 percentage points. In prior eras, policymakers might have boosted rates more than that in a single meeting.

Contrary to popular belief, the markets don’t necessarily mind rising rates. After all, higher yields are a sign of a growing economy. It becomes problematic only if rates row faster than expected. You don’t want to “be caught off guard,” says David Joy, chief market strategist at Ameriprise Financial.

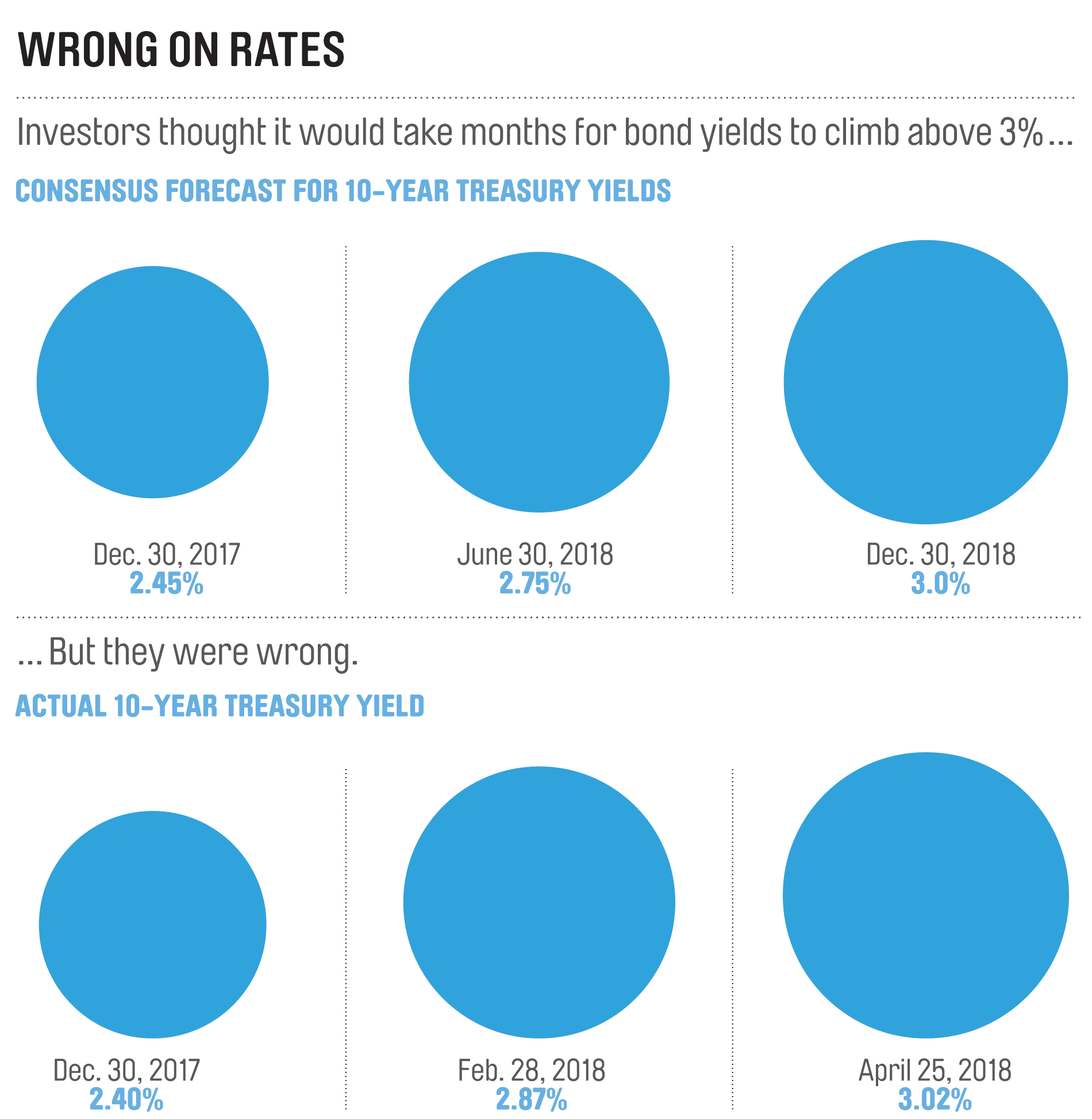

Heading into this year, most prognosticators expected the Fed to lift rates another three times, at a quarter of a percentage point per hike, bringing a key short-term rate to 2.25% by the end of the year.

The reality

The threat of higher-than-expected inflation now raises the real possibility of four hikes this year. It’s not just economists who think that. In their March meeting, Fed governors indicated a fourth hike was within the realm of possibility.

But a potentially bigger interest rate question comes from the Fed’s balance sheet. To help stimulate the economy, the Fed didn’t just lower short-term rates; it purchased huge amounts of short- and longer-term Treasuries and government-backed securities to keep yields in general low. Now that the economy can stand on its own, the Fed is unwinding its $4 trillion portfolio, which could boost the supply of bonds on the market—driving prices down and yields up. “It’s going to take years” for it all to unwind, says Joy.

This selling may have contributed to the fact that yields on 10-year Treasury notes reached 3% in late April, several months before investors assumed that would happen.

What you can do

With the fed helping to boost short- and long-term rates, investors need to be mindful of interest rate risk. Many strategists suggest focusing on shorter-term debt that will come due sooner and that can be reinvested at higher yields.

On the Money 50 list, turn to a short-term fund such as Vanguard Short-Term Bond ETF (BSV). Or focus on intermediate-term funds that own relatively shorter-term securities, such as Dodge & Cox Income (DODIX) or Loomis Sayles Bond (LSBRX).

4. Stocks Lose Some Juice

The assumption

It’s easy to understand why so many market watchers thought stocks were bound to rise in 2018. Not only did Congress just pass the Tax Cuts and Jobs Act of 2017 in late December—lowering personal income tax brackets while slashing the top corporate rate from 35% to 21%—but corporate earnings were set to grow by nearly 20% this year. Among the most bullish forecasts: The wealth management firm Canaccord Genuity predicted the S&P 500 would gain 16% this year.

The reality

The tax cuts have been signed into law, and profit growth for the S&P 500 got off to a roaring start in the first quarter—earnings were up more than 23%. Yet the S&P 500 has been flat.

What happened? Call it a classic case of that old saying: “Buy the rumor and sell the news.” The stock market is forward-looking. Last year, the anticipation of tax cuts to come—which would allow companies to repatriate billions of foreign profits back to the U.S.—helped the market return nearly 22%. But now that lower taxes and higher profits are baked into the cake, stocks are at a level that’s “hard to surpass, but easy to disappoint,” says James Paulsen, chief investment strategist for the Leuthold Group.

Without a new carrot propelling the market forward, it will take better-than-expected corporate performance to pique interest.

What you can do

Reassess your international exposure. U.S. equities have been the hands-down leader of the global markets as of late. Over the past five years, the S&P 500 has returned nearly 13% annually, which is more than double the returns of foreign shares.

That means if you haven’t been rebalancing, you may have less exposure abroad than you once did. For example, if you started off five years ago with 20% of your stock portfolio overseas, you’d now have only 15% in international equities owing to the market’s recent moves.

Yet many strategists believe that with foreign shares so much cheaper now—the Shiller P/E for foreign stocks is about half that for domestic equities—investors should hold one-third or more of their equity exposure overseas.

Because the fastest growth is found in emerging economies such as China’s, think about foreign funds with exposure to both developed markets and emerging economies. Take the Money 50’s Vanguard Total International Stock ETF (VXUS). Nearly 20% of this ETF’s assets are held in emerging-market shares, with about half that exposure held in China and India.

5. Tech Slows Down

The assumption

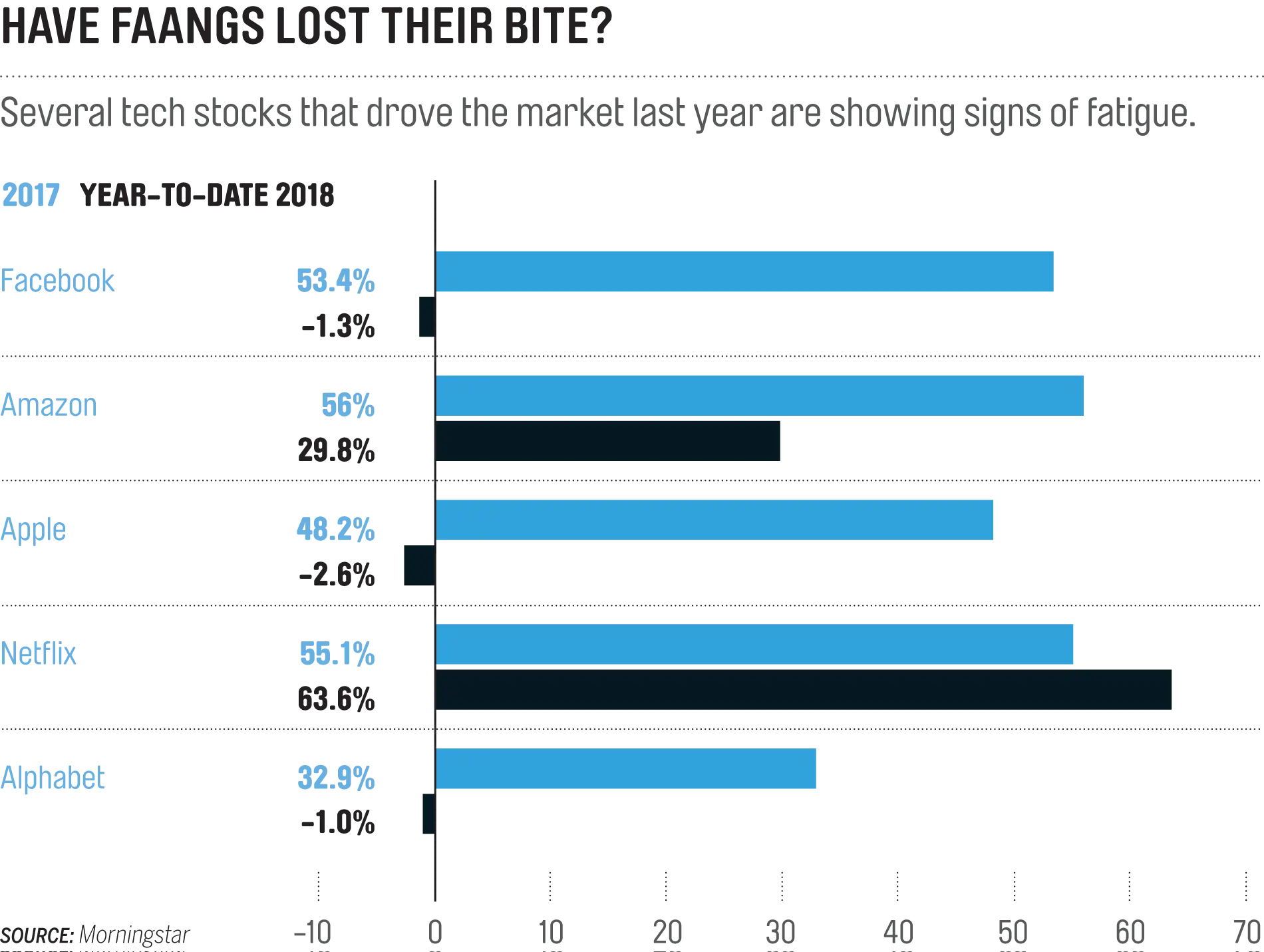

For years, it paid to be aggressive in the stock market. And nowhere did this strategy pay off more than with the so-called FAANG stocks—Facebook (FB), Amazon (AMZN), Apple (AAPL), Netflix (NFLX), and Google-parent company Alphabet (GOOGL).

Accounting for about one-eighth of the total market value of the S&P 500, these five stocks returned an average of 47% in 2017. Few analysts forecast such outsize gains for 2018. But few assumed many of these stocks would struggle.

The reality

Many FAANGs, including Apple and Alphabet, are struggling more than the broad market, signaling that market leadership could be shifting.

Facebook is probably the most prominent example. Its shares are down slightly for the year, as the social media giant is embroiled in a scandal related to an analytics firm’s having used Facebook data inappropriately to try to sway voters in the 2016 presidential election.

And while Amazon shares are up, the e-commerce giant finds itself mired in a public feud with President Trump, who has been critical of the company’s tax rate and shipping arrangement with the U.S. Postal Service. This may stem from bad blood between Trump and Amazon CEO Jeff Bezos, who also owns the Washington Post, but it points to the risk that tech leaders may face more regulations.

These issues highlight some of the weaknesses in tech’s armor, says Peter Boockvar, chief investment officer at Bleakley Advisory Group.

What you can do

Despite the backlash, don’t jettison your exposure to FAANGs altogether. These are the most influential names in technology, a sector that typically performs well when interest rates are rising, like now.

But diversify your tech exposure with a broader sector fund like the Vanguard Information Technology ETF (VGT), which still gives you exposure to FAANGs but balances that with less-volatile older tech names like Microsoft (MSFT) and Intel (INTC).