How to Pick the Best Health Care Plan During Open Enrollment

As health care gets more costly, your open-enrollment decisions become ever more critical. Workers at large companies will pay 5% more, on average, on insurance premiums in 2017, says the National Business Group on Health (NBGH).

You'll probably shell out in other ways too. Average in-network deductibles rose a whopping 50% for PPO plans in 2016, while primary-care co-pays were up 25%. Rising drug costs are another pain point: "The idea that you don't have to worry about costs because you have health insurance is ridiculous," says Doug Hirsch, CEO of GoodRx, which tracks drug pricing.

Make the right choice during this year's open enrollment and you could actually cut your costs, notes Jody Dietel, chief compliance officer at benefits administrator WageWorks. But the wrong choices could leave you paying thousands of dollars more than necessary for the care you need.

Pick Your Plan

Nearly 70% of firms offer at least two policies, according to the Society for Human Resource Management, making the plan itself your most important decision. Start here:

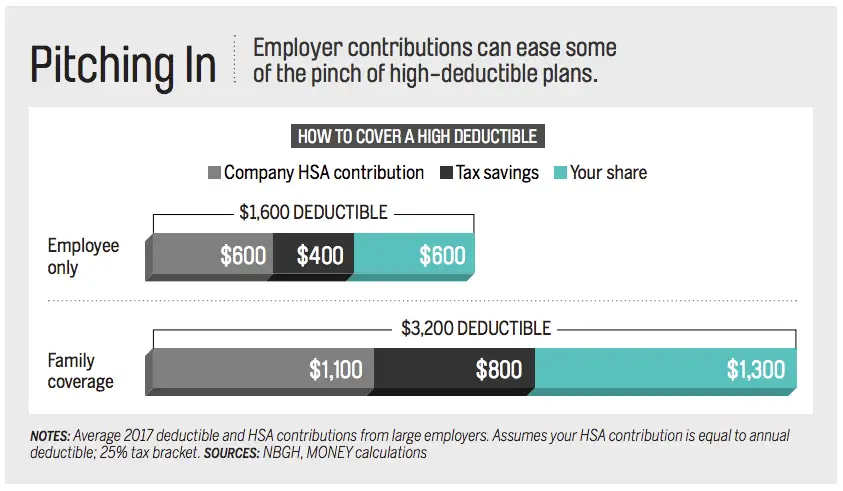

Aim high. For next year, the NBGH finds, 84% of large companies will offer a high-deductible plan—one with a deductible of at least $1,300 for individuals ($2,600 for a family), although it could be much higher. "If you're really healthy or really sick, it's the plan to be on," says SHRM's Sylvia Francis.

If you're in good health, the case is clear. You save on your annual premium. (In 2016, employees paid $1,352 for HMOs, on average, and $1,377 for PPOs, SHRM found, but $1,067 for high-deductible plans.) And your employer may put money into a health savings account paired with these plans; large companies will pitch in an average $600 for individuals and $1,100 for families in 2017. With the tax break you get for contributions, that could add up to more than the difference in deductibles. (See graphic below.) And you may not spend much: Many in-network preventive services, from mammograms to colonoscopies, are covered at 100%.

Read next: The Downside of High Deductible Health Plans

A cheaper high-deductible plan can also be smart if you or your covered family members need high-priced medications or a lot of care, Francis says. You'd hit your deductible quickly, then face only co-pays and co-insurance until you hit the annual out-of-pocket limit ($6,550 for an individual, $13,100 for family coverage—slightly lower than for PPOs).

If your health needs fall somewhere in the middle, though, a more traditional plan might be better.

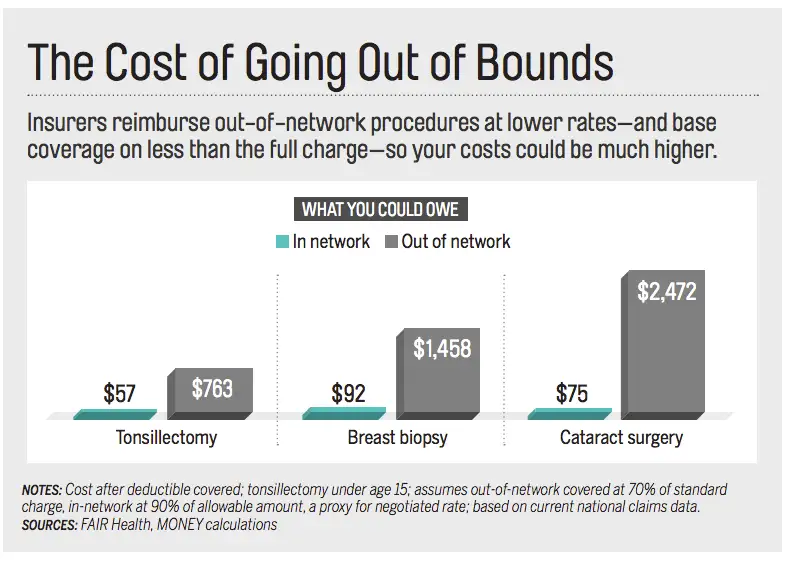

Check your network. While networks of doctors and hospitals haven't suffered the same drastic shrinkage on employer plans as on Obamacare offerings, staying in network is as essential as ever.

Eyeing an HMO? Your costs will be covered only if you get care from participating doctors and facilities, leaving you on the hook for the entire bill if you venture outside the network. A PPO is more flexible, but you'll still face higher costs and separate deductibles if you stray. "Out-of-network coverage is better than nothing, but you shouldn't just assume you'll only pay a little more," says Karen Pollitz, senior fellow with Kaiser Family Foundation.

Take a breast biopsy. A standard charge is $2,102 nationwide, according to FAIR Health, which provides health cost data—with insurers typically deeming $920 an "allowable amount." So an insurer may cover 90% of a pre-negotiated rate for in-network outpatient surgery, but just 70% of the allowable amount on out-of-network care. If you went out of network, you'd have to pay the remaining 30% ($276) plus the part that wasn't allowable: $1,458 in total.

Ask your doctor's office if it participates in each plan you're considering. Hospital procedures can be trickier, but if you're planning surgery, try to ascertain that both the facility and any professionals who would treat you are on the plan you're choosing.

Perform a drug test. If you regularly take prescriptions, check the "formulary"—the list of covered medications. Most plans divide drugs into tiers and cover each differently, so see what tier your drug is on—then read the Summary of Benefits and Coverage to see how much you'd pay at that tier. "As you go up in tiers, you're getting much less coverage," says GoodRx's Hirsch.

Read next: 5 Reasons Prescription Drug Prices Are So High in the U.S.

One problem for patients, he says, is an ongoing shift from a co-pay (a flat fee) to coinsurance (a percentage of a drug's cost). "Coinsurance leaves you with significantly higher costs," he says. If your drug costs are noticeably cheaper on one plan than on others, you may have a winner.

Split with your spouse. If you and your significant other both have jobs, it may pay to part ways for health coverage. "We're definitely seeing an uptick in spousal surcharges," says Julie A. Stone, a health care consultant with Willis Towers Watson. One in three companies charges extra ($100 a month, on average) to cover spouses who can get health benefits through their own employer.

Manage Your Costs

With medical costs up, stashing money in tax-advantaged savings plans is more crucial than ever.

Max out your HSA. If your plan features one, contribute at least enough to cover expected out-of-pocket costs. You'll get a sweeter tax break, though, by putting in the maximum—up to $3,400 for individuals (a $50 hike vs. 2016) and $6,750 for families (unchanged) for 2017, with another $1,000 if you're at least 55. The money grows and can be spent tax-free for qualified medical expenses years later.

Weigh an FSA. If your plan has a traditional deductible, many employers let you contribute to a flexible spending account via paycheck deductions—up to an expected $2,600 in 2017, vs. $2,550 in 2016. You can use this pretax money for a broad range of health costs not covered by insurance. One caveat: You must use FSA funds within the plan year, though your employer may let you carry up to $500 from one year to the next.

Double up. You can't put money in both an HSA and FSA for the same services—but you may be able to pair the accounts for greater tax benefits. One option, Dietel says, is to put cash in a "limited-purpose" FSA, which can be used for vision and dental expenses.

Prepare for Care

Open enrollment is also when employers announce new programs that will affect the cost and quality of your care. What to do now:

Seek excellence. For many treatments—bariatric surgery, transplants, fertility services, and increasingly knee, hip, or spine surgery, and cardiovascular or cancer care—almost one in five large employers say they will cover a greater share of the bill in 2017 if you get care at preferred facilities, dubbed Centers of Excellence. Planning any major procedures? Now's the time to see whether your company will cover more at these preferred sites.

Dial it in. Nine in 10 large employers are promoting "telehealth" services—remote video medical exams, available 24/7—up from 70% in 2016. You can save real money: An after-hours visit to the ER, for example, will run you $700 out of pocket on average, says NBGH chief executive Brian Marcotte, while you might pay $40 for a telehealth visit, depending on your plan. When you're running a fever on a Saturday evening, you don't want to waste time on your benefits website. Register with your telehealth service now, then bring home the information.

Be a joiner. Check to see if your firm gives you incentives for participating in health-risk assessments, weight-loss programs, and other wellness activities. More than three in 10 companies now do, KFF finds. Those programs offer an average of $130 to $140 for filling out a health-risk questionnaire or completing a physical screening. Just participating may not be enough, though: You may have to hit a particular target to collect company HSA contributions or other rewards.