Why Skimpy Bond Yields Are a Retirement Game Changer

- This Nobel Economist Spotted the Last Two Bubbles—Here's What He Says About the Bond Boom

- Here's What to Expect From the Bond Market in 2015

- Yes, Stocks Are Tanking -- But Here's What We Should Really Worry About

- What Does a Bond Fund Manager Actually Do?

- Here's What You Need to Know About the Pimco Stampede

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

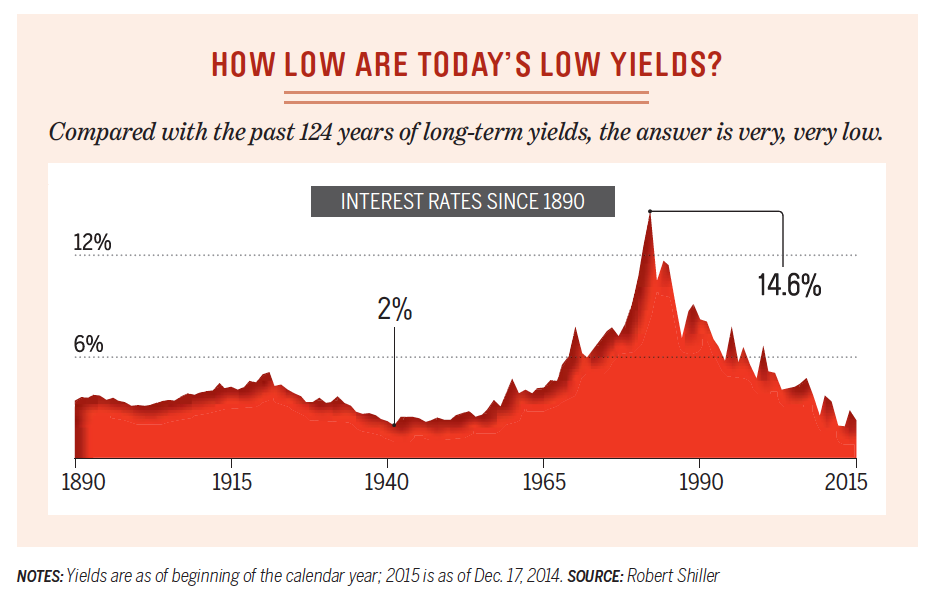

Yields on the benchmark 10-year Treasury slipped below 2% on Tuesday as bonds rallied. (Bond prices rise when yields, or interest rates, fall, and prices fall as rates rise.) Since the aftermath of the 2008 financial crisis, bond yields have bounced around near historic lows. That's had many investors worried about what would happen to their fixed-income investments when the seemingly inevitable rise in bond interest rates finally arrives.

But in fact, today's low yields could present a long-term challenge to retirement-oriented savers, even if interest rates stay low, and even if bonds today aren't overpriced. And investing mostly or entirely in equities won't immunize you from the problems of investing during a low-return era.

What happens if bond yields rise. First, let's consider what happens if the conventional wisdom is right, and bond yields do start to rise again. If you hold bonds in a mutual fund as part of, say, a 401(k) plan, the most important thing you can do is understand your risk when bond prices fall. A plain-vanilla, intermediate-term bond fund these days has a "duration" of about 5.5. That measure of interest-rate risk roughly means that if rates rose by one percentage point, the fund would fall 5.5% in value. (Your actual loss would be lower, since you'd still be getting paid interest on the bonds in the fund.)

A decline in the value of a fund that’s the safe part of your retirement portfolio could come as a shock, and for money you may need soon, a shorter-duration bond fund makes sense. But keep short-run bond fund losses in perspective: Over the longer run, a shift up in rates can also help make up for what you lost, and the current yield on bonds gives you a strong clue about what to expect.

Say you own a diversified bond fund. Assume the yield is about 2% when you buy it, and the fund’s average bond matures in seven years. According to numbers from Vanguard, a sudden two-point jump in rates—a huge spike—would cause the fund to lose about 8% in total. As its bonds paid out higher yields, however, your annualized return after seven years would still be likely to level off to just about 2%.

What happens if yields stay low. The real risk with bonds today, however, may not be losses in the short run. It’s that the returns will stay frustratingly low for a long time.

Ben Inker, co-head of asset allocation at GMO, a Boston fund manager, lays out two scenarios, one he calls “purgatory” and the other “hell.” In purgatory, rates are headed for a spike. Bond prices will fall, and stocks might too. But after that you pick up better yield and better returns.

In hell, interest rates stay low. Part of the reason it's hell is why interest rates stay low: The economy never gets back to its pre-2008 strength. With low growth prospects, there's less demand for capital, and many investors around the world are content to accept relatively low returns on cash and bonds.

Part of the reason yields have recently fallen below 2% is that bond investors still see some risk of this "secular stagnation" scenario.

Ironically, in hell, your bond investments don’t lose money, since there's no big rate spike. And today’s stock prices, oddly, might make sense too. Here’s why: When the price of stocks is high relative to long-run past earnings, future returns tend to be lower. Today the P/E ratio for stocks is expensive at 27. (The average is 17.) So stock returns may be on the low side. You still may be willing to take that deal, however, if you are earning only 2% on your bonds.

That may help explain why stocks have recently shot up. But if so, that’s a one-time adjustment. Hell is not just a low-bond-yield world. It’s a low-total-return world.

That would be bad news for savers, especially younger ones who will be putting much of their money into the market in the future. In the hell scenario, a typical portfolio earns 3.4% after inflation instead of the 4.7% Inker assumes you’d have gotten in the past. “Let’s say you turned 25 in 2009 and started saving,” he says. “You end up accumulating 25% less by retirement.”

Inker stresses he doesn’t know which scenario we’re headed for. The one constant is that in neither are there lots of opportunities to make money with low risk. “This is a frustrating environment for us as investors,” admits Inker. “It is less clear what the right thing to do is than throughout almost the rest of history.” The trouble with bonds, it turns out, is bigger than unpalatable yields. And it’s the trouble with an economy that is taking a long time to find its true normal.

This story is adapted from “How 2% Explains the World,” in the 2015 Investor’s Guide in the January-Feburary issue of Money.