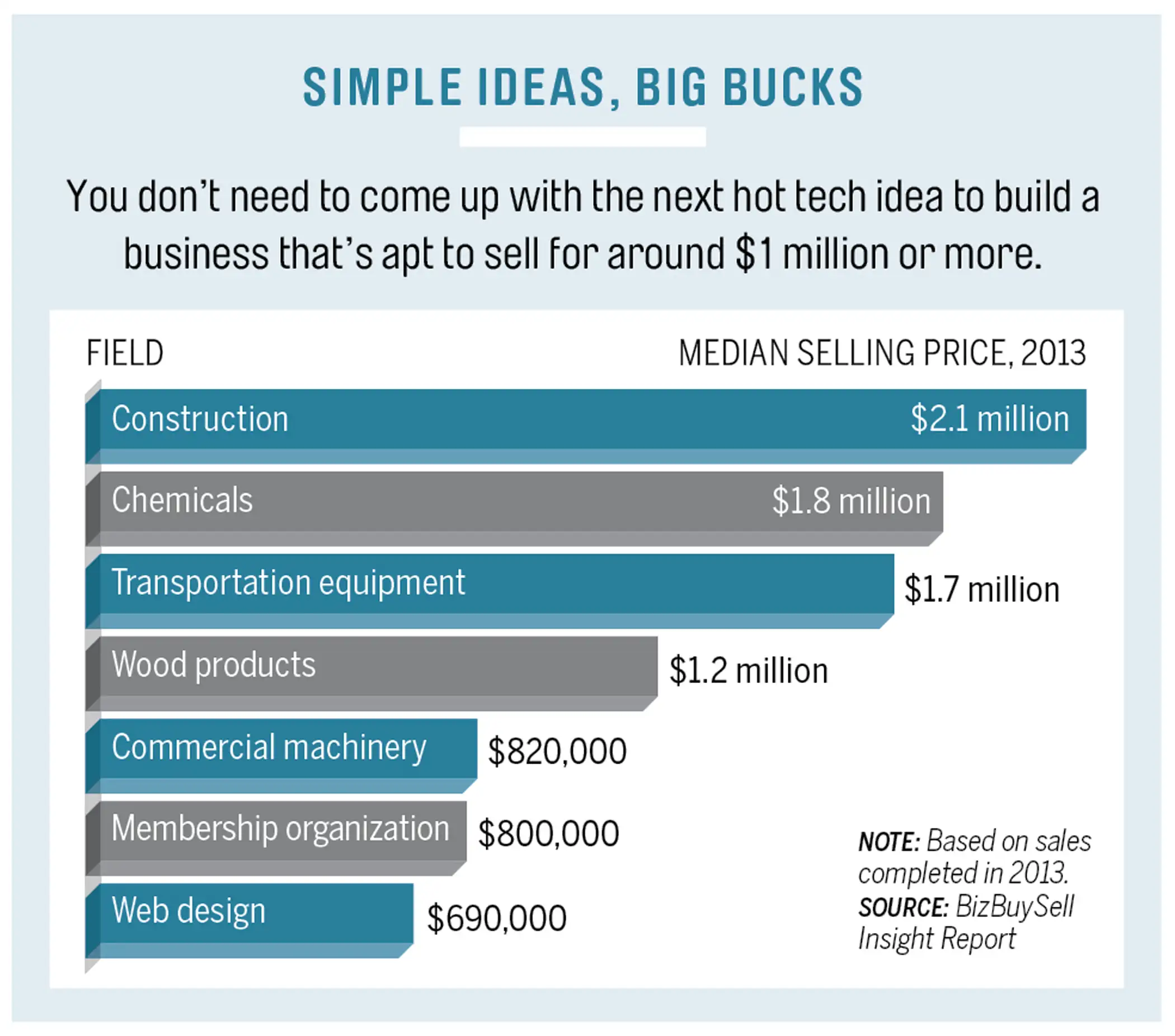

#6: Launch a (Boring) Business

A common path to seven-figure status is to start a business. In fact, about one in four millionaires run their own firms. They’ll tell you the secret to success isn’t the cachet of a big idea. Most seven-figure enterprises are pretty run-of-the-mill (see table). The key is managing your other C’s: cash flow, credit, customers, and incorporation. Handling those correctly will help you save as much as possible as you’re running the company while also making your firm appealing to potential buyers when it’s time to sell.

What to Do

Improve financing. With rates low and approval by big banks at a post-recession high, this is the best time in years to seek a small-business loan.

Tom Burtzlaff, 57, got a $175,000 SBA-backed loan a few years ago for startup financing for his tech-services franchise in Columbia, Md. The seven-year repayment schedule—longer than the usual three- to five-year bank loan—freed up cash to hire a technical manager “who helped the business quickly build a customer base and is still employed with us today,” he says.

Boost growth. Satisfied clients are a great marketing engine. Trouble is, “everyone says their clients love them, but who knows if it’s true,” says planner Mark Tepper, who works with entrepreneurs. There is a way. Even small outfits, at least those with more than a few clients, can turn to the Net Promoter Score (NPS), which measures what percentage of clients are likely to refer business to you or badmouth you. You can hire consultants to run the numbers or use a free Survey Monkey template.

If 20% of your clients are promoters and 10% are detractors, your NPS is 10, about where most firms run, says Bain & Co. The most efficient firms score 50 to 80. Boost your NPS to that level, and you’re likely to double your growth rate.

Keep more of your profits. Is your firm set up as a C corporation? You face double taxation—the company is taxed at corporate rates and you’re taxed on distributed profits. This becomes a real issue at sale.

If you’re eventually going to exit and don’t utilize C corp tax breaks, such as the deductibility of fringe benefits like disability, converting to an S corp makes sense.

But you must start early, says Ron Chernak of the FBB Group, a business broker in Colorado Springs. To keep the tax benefit, the IRS says you must wait 10 years to sell after conversion.

Say you cash out of a C corp in an asset sale of $1 million. At a combined federal and state corporate tax rate of 40%, the firm would owe $400,000 at sale, leaving $600,000 to distribute to shareholders, says Gary Seltzer, a CPA at SSA PC in Colorado Springs. If you’re in the highest federal bracket (20% for qualified dividend income) with a 7% state tax, you’d pay $162,000. You’ll also likely be hit with the 3.8% net investment income tax, for $22,800. Total taxes paid: $584,800.

In an S corp, the $1 million sale would pass through to shareholders and be taxed as ordinary income. Assuming the highest bracket, you’d pay $466,000. Total savings: $118,800.