#4: Play It Safe With Stocks As You Age

Conventional wisdom says you need a big dose of equities to get to $1 million by your sixties and to grow your money in retirement. That’s true. But what’s the point of getting near your goal if that same stance knocks you back before you retire? That’s the lesson investors learned in 2008, when two in five 56- to 65-year-olds held 70% or more of their savings in equities in a year when stocks sank nearly 40%.

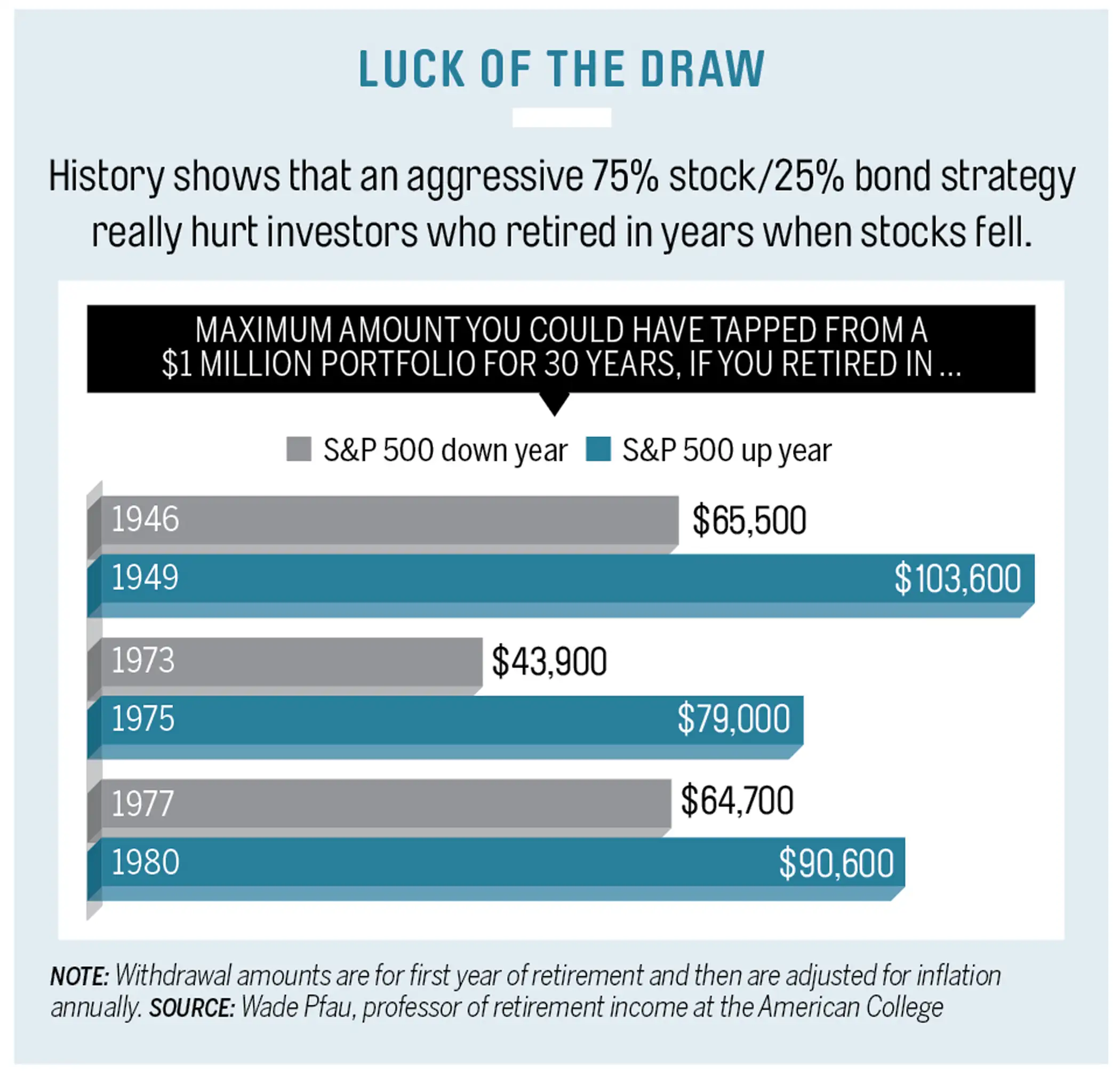

Stocks play a vital role on your path to $1 million, but researchers have identified a critical stage where you’re most vulnerable in the years just before and after you stop collecting a paycheck. As the chart below shows, the difference between success and failure can be as little as calling it quits and having to tap your nest egg in an up year—like 1975, when the S&P 500 soared 37%—or two years earlier, when stocks fell 15% in 1973, according to research by retirement income expert Wade Pfau.

Of course, no one can predict where the market will be a decade hence. But the fact we’re five years into this bull market and the Dow just hit a record 17,000 suggests stocks have more downside than upside in the near term.

What to Do

At retirement, play it safe with stocks. A strategy advocated by Pfau and financial adviser Michael Kitces turns the conventional wisdom of letting your portfolio get conservative on its head.

They recommend dropping your stake in stocks to 20% to 30% at retirement—to preserve what you’ve saved—and then gradually boosting it over time, say one point a year. The idea is low exposure to equities protects you in the first 10 years of retirement. And if returns are poor, you’ll want more equities later on to grow your money. They ran thousands of simulations and found this approach stands a better chance of lasting 30 years than a regular “glide path,” where stock exposure gradually falls.

This is counterintuitive, but it’s not so strange. Many target-date retirement funds now drop their equity stake to around 30% at retirement (though they don’t grow more aggressive later).

It is all part of a new wave of thinking that says risks aren’t just tied to the economic cycle. “It doesn’t make sense to talk about the riskiness of stocks unless you also talk about the age and earning power of the investor,” says investment adviser William Bernstein. In this case a retiree has the most money at stake and the least time to recover from losses, so caution is warranted.

Be aggressive with Social Security. Since you’re not being aggressive with your portfolio, you’ll want to compensate elsewhere. Unless you’re in bad health, most advisers recommend waiting as long as possible to receive Social Security benefits. The annual bump you get for waiting is equivalent to a guaranteed 8% investment return, something “almost impossible to beat” with your portfolio, says Bill Meyer, chief executive of Social Security Solutions.

Pharmacist Jeffrey Schein, 57, and his wife, Nancy, a nurse anesthetist, 57, of Smithtown, N.Y., agree. The Scheins, who hope to retire in their mid-sixties and have saved nearly $2 million, plan to put off Social Security until 70. “I have longevity in my family,” he says. “I want my money to last into my nineties.”