With These Two Moves, You Can Retire Well No Matter What the Market Does

This is the first in a three-part series on strategies for a worry-free retirement.

It has been a wild ride in the markets this year. But that goes with the territory. Based on history, stock investors can expect a decline of 10%—about what the S&P did this summer—once every seven months on average, says the investment firm Gerstein Fisher. So when it comes to your retirement, it's best not to focus on short-term ups and downs you can't control. Two things you can control: How much you save and how much of your return you keep in your pocket.

MOVE #1: Bust market risk with an automatic saving plan

When stocks take a sharp dive, like the 1,000 points the Dow briefly fell one day in August, attention turns to ways to hedge your bets, from gold to more exotic tools like “absolute return” funds. Yet a far better way to ensure a secure retirement in any market isn’t an investment per se, and it may be available for free from your HR department. See if your company’s 401(k) is one of the growing number of plans to offer automatic yearly increases in your contribution rates—currently about one-third do—and sign up for the option. If your company doesn’t do this yet, make a habit of escalating your savings on the date a cost-of-living raise usually kicks in or on a significant day like your birthday.

This deceptively simple step actually packs a powerful punch: More than 70% of employees who automatically increase their contributions are on track to a comfortable retirement, or almost there, says Rob Austin, director of retirement research at Aon Hewitt. (The firm defined success as saving 11 times salary by age 65.) That compares to an average of just 20% for all workers.

Automation makes saving less difficult... All forms of automated saving—whether you start with high contributions to a 401(k) right away or escalate gradually— help to reverse a behavioral quirk psychologists call loss aversion. It hurts to give up a dollar you have in hand and save it instead. Set the money aside before you see it, and you feel the sacrifice less keenly. Take it from Sahab Zanjanizadeh, 38, a software developer from Highland Heights, Ky., who has built up a $200,000 portfolio by maxing out his 401(k). “A lot of people adjust their savings to their lifestyle," he says. "I adjust my lifestyle to my savings."

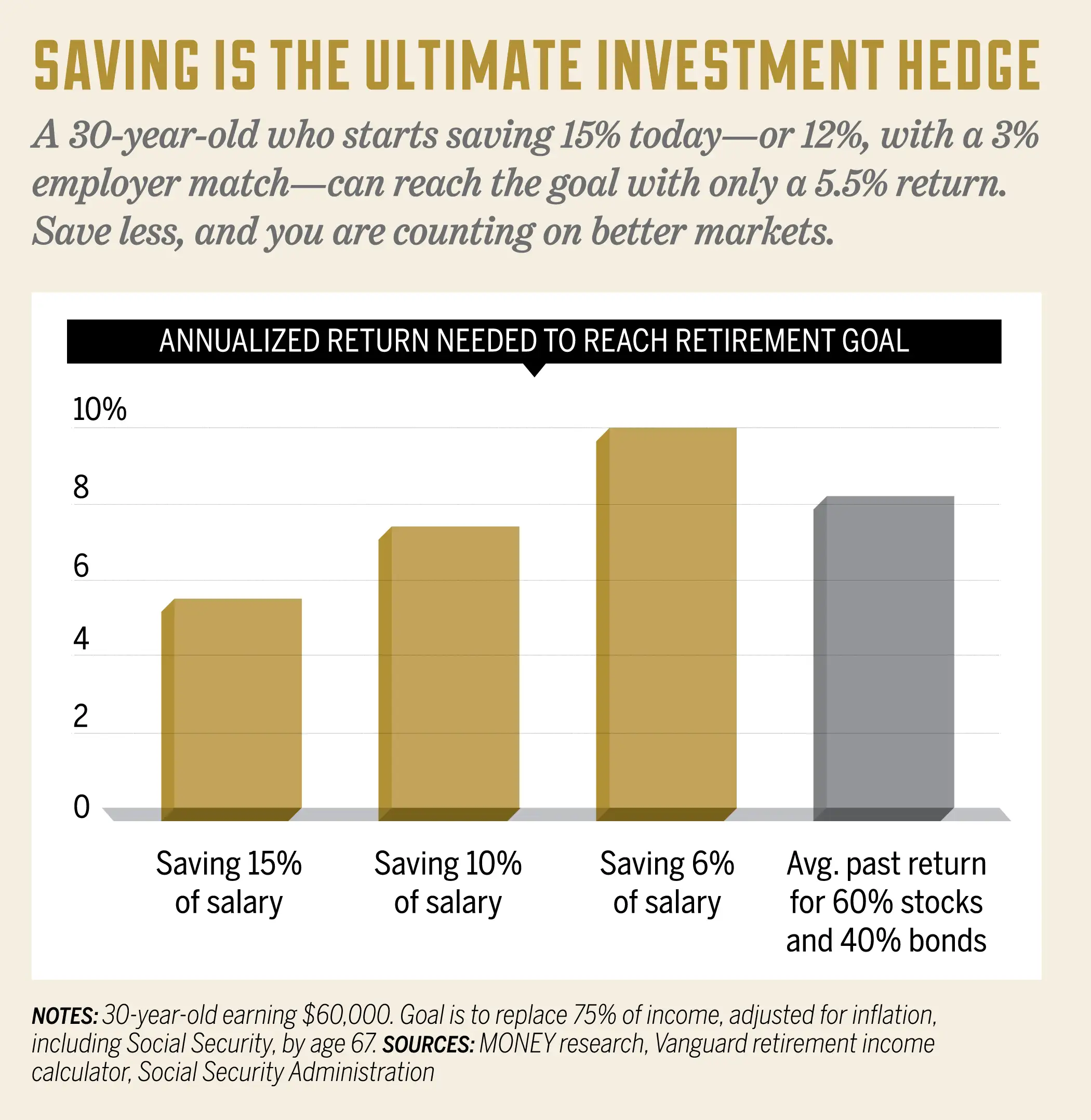

… and saving more reduces your risk. Saving more helps you steadily build wealth. But a less obvious virtue is that it makes you less dependent on high returns. Consider the example in the chart below: It assumes a 30-year-old who starts saving 15% of her salary—including employer 401(k) contributions, making it easier. Assuming she works until 67, she can reach a preset goal of having enough to replace 75% of her pre-retirement income, even if her investments deliver less than a 6% annualized return.

With that margin for error she could choose to invest relatively conservatively. Or she could even take on a bit more risk, since she can sustain some tough losses and still earn the required return over time.

Scale back the savings rate to 6%, and the wiggle room is gone. The required rate shoots up to 10%. That’s the average stock return since 1926—but stocks have failed to hit that number in 39% of all 20-year periods, once earning as little as 3% annualized. And volatility along the way will be high. Maria Bruno, a senior investment analyst at Vanguard, says that historically an 80% stock portfolio has seen losses of up to 35% in bad market years.

For younger people a long way from selling, saving early can actually turn tough markets in your favor. After all, that’s when you can buy stocks at relatively cheap prices.

MOVE #2: Be greedy for every nickel of your returns

So what return can you expect? By at least one important measure, stocks are pretty expensive now. The dividend yield they pay to investors is only 2%, compared to a long-run average of above 4%. Since you get less for your money when you buy shares, that suggests lower returns ahead. Experts, including Vanguard founder Jack Bogle and Princeton economist Burton Malkiel, author of A Random Walk Down Wall Street, cite a classic formula to estimate the baseline return for stocks. Adding the yield to the historical rate of earnings growth, a fair guess for future returns—over decades, not for any particular year—is below 7%. Maybe 5% after inflation.

Meanwhile, the yield on safe 10-year Treasury bonds, which tends to predict total returns over the next decade, is only 2%. In the past, by comparison, stocks since 1926 have earned an annualized 10%, and bonds 5%. If leaner years are truly ahead, you don’t want to be unnecessarily generous with what you pay a mutual fund manager. Or, for that matter, the IRS.

How to win back 20%. Many stock mutual funds charge 1% or more a year. If you expect to earn 5% after inflation on stocks, then paying that rate means you’re potentially giving up 20% of your real return. Of course, most fund managers aim to do better than stocks on average, but the reality is that most actually underperform benchmark indexes such as the S&P 500.

To keep your fair share of return, invest most of your money in a fund that replicates a stock index at a low cost. Schwab S&P 500 Index (SWPPX), on the Money 50, costs less than 0.1%; Vanguard’s target-date funds combine bond, stock, and foreign-stock index funds for under 0.2%. If your 401(k) doesn’t offer low-cost funds—or piles on lots of other administrative costs—you can use it up to the employer match, then put the next dollars you save in an IRA, where you control the fund choices.

Tame your tax bill. For people with additional money beyond 401(k)s and IRAs, “using tax-efficient investing strategies can add 0.25% a year or more on average to your returns,” says Morningstar director of retirement research David Blanchett. For example, try to hold your bonds and REITs, which pay dividends taxed as ordinary income, in a tax-advantaged account. Buy-and-hold stock funds are a good fit for taxable money, since the long-term capital gains they earn are taxed at a lower rate.

Even before you are working with lots of taxable assets, you can “tax diversify.” That means saving in a combo of traditional 401(k)s and IRAs, in which you get a tax break now and owe on retirement withdrawals, and the Roth versions, in which you pay taxes upfront but won’t owe in the future. (The IRAs are subject to income limits.) Having tax-free savings to tap can give you flexibility in retirement, when withdrawals from pre-tax accounts may push you into a higher bracket. The combo makes sense if you aren’t sure what your retirement tax situation will be.

Read Next: Two Ways to Keep Your Nest Egg Safe When It Counts

Donna Rosato and Alexandra Mondalek contributed reporting to this story.