The Great Retirement Account You're Not Using

Since they were launched in 2006, Roth 401(k)s have been typecast as the ideal plan for millennials. Paying taxes on your contributions in exchange for tax-free withdrawals, the reasoning goes, is best when your tax rate is lower than it’s likely to be in retirement. It turns out Roth 401(k)s may be the better option for Gen Xers and baby boomers too.

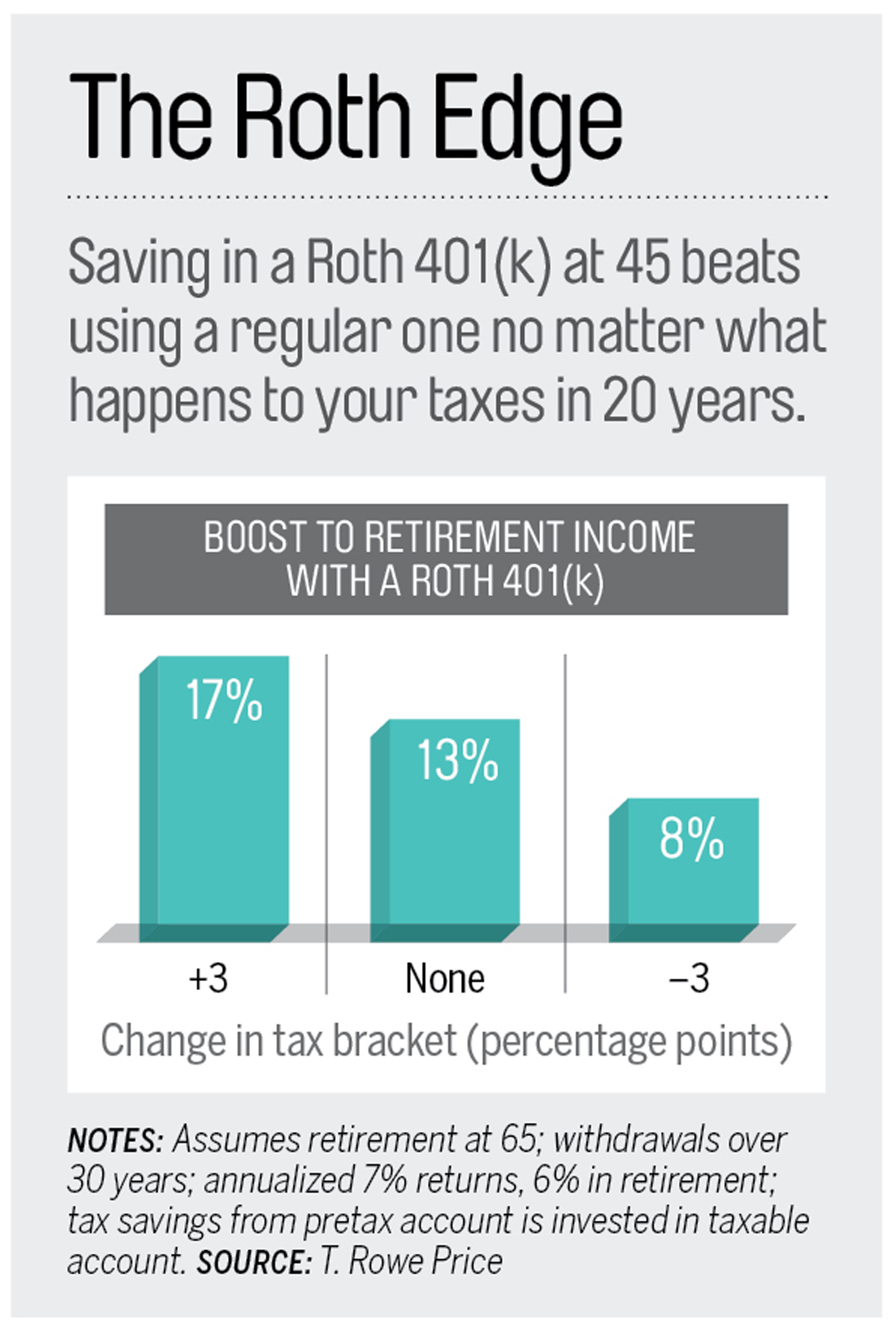

That’s the conclusion of a recent study by T. Rowe Price, which found that Roth 401(k)s leave just about all workers, regardless of age or tax bracket, with more money to spend in retirement than pretax plans do. “The Roth 401(k) should be considered the default investment,” says T. Rowe Price senior financial planner Stuart Ritter.

Yet few workers of any age invest in Roth 401(k)s, which let you set aside $17,500 in after-tax money this year ($23,000 if you’re 50 or older), no matter your income. Just as with a Roth IRA, withdrawals are tax-free, as long as the money has been invested for five years and you are at least 59½. Some 50% of employers now offer a Roth 401(k), up from just 11% in 2007, according to benefits consultant Aon Hewitt. But only 11% of workers with access to a Roth 401(k) saved in one last year. Big mistake. Here’s why:

Higher income. Every dollar you save in a Roth 401(k) is worth more than a dollar you put in a pretax account. That’s because you’ll eventually pay income taxes on those pretax dollars, while you get to keep every penny in a Roth. Granted, you get an upfront tax break by saving in a traditional 401(k), and you can invest that savings. Even so, a Roth almost always overcomes that headstart, the T. Rowe Price study found.

The fund company’s analysis looked at savers of different ages and tax brackets, both before and after retirement. As the graphic shows, a Roth 401(k) pays more even if you face a lower tax rate in retirement than you did during your career. The only group that would do significantly better with a pretax plan: investors 55 and older whose tax rate falls by 10 percentage points or more, which would mean up to 6% less income.

Greater flexibility. With a tax-free account, you can avoid required minimum withdrawals after age 70½ (as long as you roll over your Roth 401(k) to a Roth IRA). You can also pull out a large sum in an emergency, such as sudden medical bills, without fear of rising into a higher tax bracket.

Tax diversification. Having tax-free income can keep you from hitting costly cutoffs. For every dollar of income above upper levels, 50¢ or 85¢ of your Social Security benefits may be taxable. “Many retirees in the 15% bracket actually have a marginal tax rate of 22% or 27% when Social Security taxes are added in,” says CPA Michael Piper of ObliviousInvestor.com. And if you retire before you’re eligible for Medicare and buy your own health insurance, a lower taxable income makes it more likely you’ll qualify for a government subsidy. In short, when it comes to retirement, tax-free money is a valuable tool.