July Mortgage Rates Drop Back Below 3%

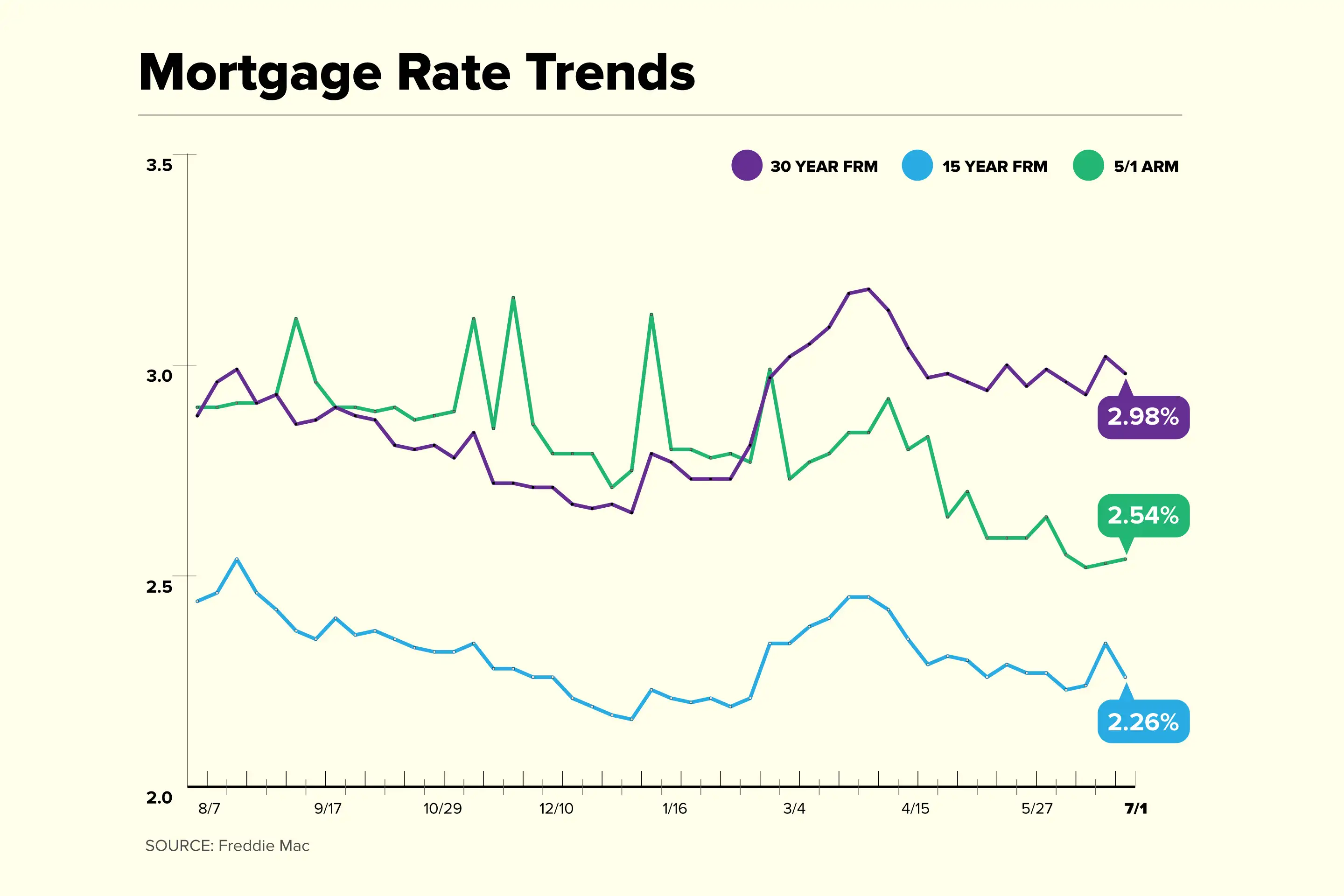

The average rate for a 30-year fixed-rate mortgage dropped to 2.98% with 0.6 points paid for the week ending July 1, according to Freddie Mac's benchmark survey.

The week of June 28th - July 1st represents a decrease of 0.04 percentage points from last week's 3.02%. Rates have been below 3% for five out of the last six weeks. During the same week last year, the 30-year rate was 3.07%.

"Economic growth remains steady and is bolstering more segments of the economy," said Sam Khater, chief economist for Freddie Mac. "Although low and stable mortgage rates have kept the housing market booming over the recent months, a deterioration in affordability and for sale inventory has led to a market slowdown."

Rates for other mortgage terms are mixed:

- The current rate for a 30-year fixed-rate mortgage is 2.98% with 0.6 points paid, down 0.04 percentage points from a week ago. A year ago, the 30-year rate was 3.07%.

- The current rate for a 15-year fixed-rate mortgage is 2.26% with 0.7 points paid, down 0.08 percentage points week-over-week. A year ago, the 15-year rate was 2.56%.

- The current rate on a 5-year adjustable-rate mortgage is 2.54% with 0.3 points paid, a 0.01 percentage points increase over last week. A year ago, the 5/1 ARM rate was 3.00%.

Mortgage Rate Trends

Will current mortgage rates last?

Mortgage rates continue to hover around 3% as economic data remain mixed.

"Mortgage rates were volatile, as investors tried to gauge upcoming moves by the Federal Reserve amidst several divergent signals, including rising inflation, mixed job market data, strong consumer spending, and a supply-constrained housing market that has led to rapid home-price growth," said Mike Fratantoni, chief economist for the Mortgage Bankers Association.

There are increasing signs, however, that the Federal Reserve may adopt a more aggressive policy as the recovery from the pandemic picks up speed. The jobs data set to be released on Friday may also push rates higher over the next few weeks. For now, it remains an extremely favorable interest-rate environment for purchasing a home or refinancing a mortgage.

On Thursday, the yield on the 10-year Treasury note opened at 1.47%, down from Wednesday's close of 1.444%. There tends to be a spread of about 1.8 percentage points between the 10-year Treasury and average mortgage rates, suggesting mortgage rates could move higher.

Why your mortgage rate may be higher than current mortgage rates

Not all applicants will receive the very best rates when taking out a mortgage or refinancing. Credit scores, loan term, interest rate types (fixed or adjustable), down payment size, home location, and the loan size will affect mortgage rates offered to individual home shoppers.

Rates also vary between mortgage lenders. It's estimated that about half of all buyers only look at one lender, primarily because they tend to trust referrals from their realtors. Yet this means that they may miss out on a lower rate elsewhere.

Last year, Freddie Mac reported that buyers who got offers from five different lenders averaged 0.17 percentage points lower on their interest rate than those who didn't get multiple quotes. If you want to find the best rate and term for your loan, it makes sense to shop around first.

Today’s mortgage rates and your monthly payment

More than other factors, your annual percentage rate on your real estate purchase will affect your monthly payments — whether you're refinancing or buying a new home.

On a $200,000 home loan with a fixed rate for 30 years:

- At 3% interest rate = $843 in monthly payments (not including taxes, insurance, or HOA fees)

- At 4% interest rate = $955 in monthly payments (not including taxes, insurance, or HOA fees)

- At 6% interest rate = $1,199 in monthly payments (not including taxes, insurance, or HOA fees)

- At 8% interest rate = $1,468 in monthly payments (not including taxes, insurance, or HOA fees)

Refinancing to a lower interest rate could save hundreds of dollars a month if you kept the same loan terms. Shortening the loan term could negate your monthly savings but save thousands over the life of the loan. You can experiment with a mortgage calculator to find out how much a lower rate could save you.

Other factors besides interest affect how much you'll pay in mortgage payments:

- Mortgage Insurance: Mortgage insurance costs up to 1% of your home loan's value to your payment each year. Borrowers with conventional loans can avoid private mortgage insurance by making a 20% down payment or reaching 20% home equity. FHA borrowers pay a mortgage insurance premium throughout the life of the loan.

- Closing Costs: Some buyers finance their new home's closing costs into the loan, which adds to debt and increases monthly payments.

- Loan Term: Choosing a 15-year mortgage instead of a 30-year mortgage will increase monthly mortgage payments but reduce the amount of interest paid throughout the life of the loan.

- Fixed vs. ARM: An adjustable-rate mortgage's monthly payment could change from year to year after the loan's introductory period expires. A fixed-rate loan's payments remain the same throughout the life of the loan.

- Taxes, HOA Fees, Insurance: A monthly mortgage payment could also include homeowners insurance premiums, city or county property taxes, and Homeowners Association fees. Check with your real estate agent to find out how much they would add to your payments.

Will current mortgage rates save you money if you refinance?

You should consider refinancing your home loan if your current mortgage rate exceeds today's mortgage rates by more than one percentage point. Mortgage refinance fees and closing costs would cut into your savings. You also have to consider whether your credit score would qualify you for today's best refinance rates.

Many online lenders can give you free rate quotes to help you decide whether the money you'd save in interest charges justifies the cost of a new loan. Try to get a quote with a soft credit check which won't hurt your credit score.

You could enhance interest savings by going with a shorter loan term such as a 15-year mortgage. Your payments may be higher, but you could save thousands in interest charges over time, and you'd pay off your house sooner.

Should you buy mortgage points?

Many lenders sell mortgage points (also known as discount points). Buying points means you’d pay more up front to lower your mortgage rate which could save you money long-term. A mortgage discount point normally costs 1% of your loan amount and could shave 0.25% off your interest rate.

With a $200,000 mortgage loan, a point would cost $2,000. Buying two points would cost $4,000 which would be due, in cash, when you close the loan. These two discount points would translate into a 0.5% reduction to your interest rate.

Discount points could pay off but only if you keep the home loan long enough. Selling the home or refinancing the mortgage within a couple of years would short circuit the discount point strategy. But if you stayed in the loan indefinitely, you'd reach a break-even point after which the discount points would save you more and more over time.

Often, spending cash on a down payment instead of discount points saves more unless you know for sure you're keeping the loan for years. If a larger down payment could help you avoid paying PMI premiums, put the money toward your down payment instead of discount points.

How to find the best mortgage lender

The best mortgage lender for you will be the one the can give you the lowest rate and the terms you want. Your local bank or credit union probably writes mortgage loans with rates close to the current national average. A loan officer in your local branch could guide you through the process.

Online lenders have expanded their market share over the past decade. You could get pre-approved within minutes. Your loan amount combined with current mortgage rates could define your price range for home prices in your area. Many online lenders also assign a dedicated loan officer to offer continuity as you shop.

Shop around to compare rates and terms, and make sure your lender has the loan option you need. Not all lenders write USDA-backed mortgages or VA loans, for example. If you're not sure about a lender's veracity, ask for its NMLS number and search for online reviews.

What type of mortgage do you need?

First-time homebuyers can walk into a mortgage brokerage office or visit an online lender without knowing what kind of mortgage they need. But it's always better to have an idea of what you're shopping for, especially since you can't control other factors such as home prices and current rates.

Mortgage loan types include:

- Conventional Borrowing: Shoppers with higher credit scores and higher down payments can get a conventional mortgage with either a fixed or adjustable rate. Mortgage interest rates can be low for qualified buyers.

- Subsidized Borrowing: The Federal Housing Administration and the U.S. Department of Agriculture help first-time homebuyers and shoppers in low-income areas buy homes by subsidizing their mortgage loans. FHA and USDA loans allow shoppers with lower credit profiles (a FICO score of 580) to still get affordable home financing. Subsidized loan restrictions include borrowing maximums and safe housing inspections. These loans are for single-family homes in most cases.

- Veterans Affairs Loans: Veterans and active-duty service members can buy homes with no down payment and no PMI through the Department of Veterans Affairs' lending program. Banks make loans that are guaranteed by the VA. VA loans require a funding fee that could range from 1.4% to 3.64% for first-time homebuyers.

- Jumbo Loans: Homes in high-value housing markets like San Francisco and New York City may not fit within a conventional or FHA loan. Jumbo loans can help because they exceed the conforming loan limits of Fannie Mae and Freddie Mac.