Give Your Portfolio a Midyear Checkup

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

Even if you’re feeling fine, you still visit the doctor now and then to make sure everything’s all right. Well, your portfolio deserves the same level of care. For instance, you may be pleased that the broad market is up again this year—continuing a bull run that has tripled your equity stake since 2009.

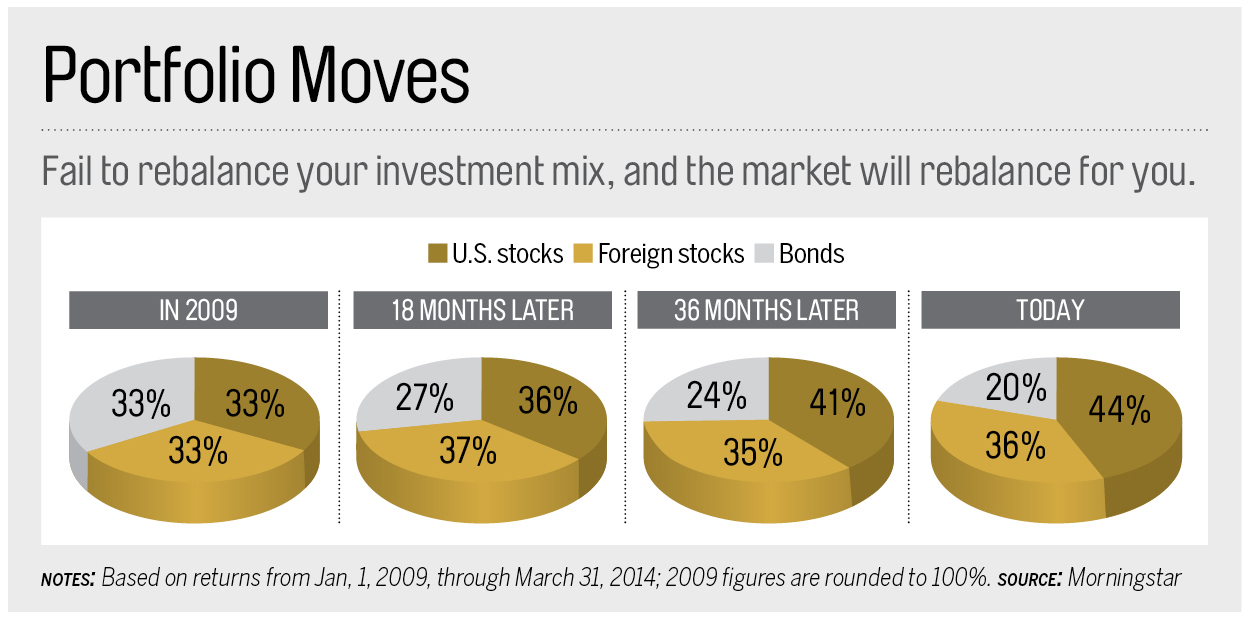

Yet investment success often brings with it a growing exposure to risk—perhaps too great to tolerate. See the chart below:

Here are three ways to review and adjust your investments to make sure they’re in tiptop shape:

Book losses now to capture an important tax break.

You don’t want to be a short-term investor, but you also don’t want to look a tax gift horse in the mouth.

Chances are, you’re sitting on hefty gains after the recent bull run. Want to take some profits off the table by selling winning shares of stocks, funds, or ETFs, but are reluctant to do so for fear of triggering a big capital gains bill? Book some losses now and Uncle Sam will let you offset those gains.

Normally, investors “harvest losses” at the end of the year. However, “you need to plan ahead” in case some of those losses evaporate, says Ann Arbor planner Rob Oliver.

Where to start? Emerging-market equity portfolios have fallen over the past three years, while Chinese region funds have lost more than 8% of their value so far in 2014. Other fertile ground: stock funds that specialize in gold and other precious metal–related investments (down 24% annually over the past three years), and shares of fast-growing small companies (down 7% year to date).

Tip: Don’t upset your portfolio just to take advantage of this break. While the IRS’s wash-sales rule bars you from buying the same or a “substantially identical” investment within 30 days of a sale, there’s nothing stopping you from selling an individual stock or an actively managed portfolio and replacing it with an index fund that covers the same asset. “If you sell a housing stock at a loss, you could buy a housing industry ETF,” says Pittsburgh adviser Jim Holtzman.

The market has changed your portfolio, so change it back.

“This is the first time in years that rebalancing has become really necessary,” says John Rekenthaler, director of research at Morningstar.

That’s because of the wide gap in performance between stocks and bonds lately. While equities posted double-digit annualized gains since 2009, fixed-income investments have returned just 4.8% a year.

Even if you rebalanced as recently as two years ago, you’ll want to at least revisit your mix. Why? Say you started off with a portfolio that was 70% in equities and 30% in bonds in May 2012. Because stocks have soared 45% since then while fixed income has been mostly flat, your portfolio is now 77% stocks and just 23% bonds.

Tip: Review your portfolio semiannually, but make adjustments only if your mix is substantially off—five percentage points or more above or below target. Rebalancing reduces portfolio risk, but there are times when it can also cut into returns. Use this strategy only when your exposure to certain assets grows uncomfortably high.

Make sure your life hasn’t changed either.

Unless you hold the bulk of your assets in a target-date retirement fund—which automatically shifts your mix for you, growing gradually more conservative over time—you’ll have to tweak your approach every now and then simply to reflect changes in your life.

For instance, as a 40-year-old you might have been comfortable holding 80% in equities, but at 50 you’re playing with greater sums and less time, so you might want to cap it at 60% to 65%.

Tip: To show how your asset mix should shift as your circumstances change, check out the free asset allocation calculator at Bankrate.com’s retirement section. Also, when you execute these changes, start in your 401(k)s and IRAs, where you won’t trigger capital gains taxes by selling. Why generate a tax bill when you don’t have to?