Jack Bogle Explains How the Index Fund Won With Investors

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

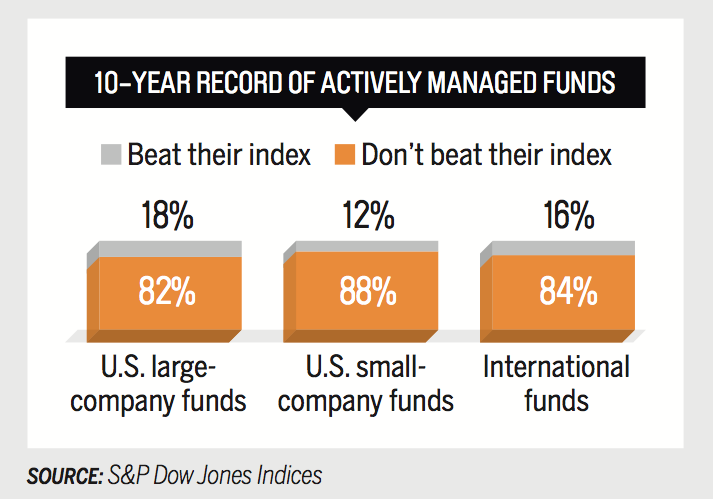

Mutual fund managers who pick stocks haven't had much to show for their efforts (or their fees) in recent years. An investor would likely have made more money over the past decade by picking a low-cost index fund that mirrors the market as a whole. In 1976, John C. Bogle launched the first such fund for retail investors, Vanguard 500. This edited interview originally appeared in the August 2015 issue of Money magazine.

Q: Has the index fund won?

A: It certainly has. Vanguard has the largest share of fund assets—almost 20%—in the industry. Two-thirds of that is index funds.

But index funds had a fabulous year last year. [Vanguard's flagship Total Stock Market Index Fund earned 12.4%, vs. an average of 7.8% for domestic stock funds.] It's not going to happen again, maybe ever, so basically we got overly praised. You shouldn't buy an index fund because you think it's a hot performer. Buy it because you're going to hold it forever.

Look, all I did with the index fund was make sure you got your fair share of the market's return. Sometimes that fair share is going to be bad, so you're going to lose money. And that's a great marketing message—candor as a marketing strategy. And it's paid off. People hawking a particular fund have no idea how long it will continue to do well. They'll say, "Our fund went up 500% in the last 10 years, and the index fund only went up 320%, so indexes are overrated." That's usually the end for that fund.

Q: Vanguard's no longer the only big player in indexing. What's the difference between buying a Vanguard fund and an index-based exchange-traded fund from, say, iShares?

A: The ETF is a different breed of cat. There are really two ETF businesses. One is huge and involves enormous amounts of trading. Then there's the much smaller market of individual investors who aren't trading all day long. They could just as easily be in the traditional mutual fund. [Vanguard sells its index funds in both ETF and traditional form.]

Q: So ETFs have short-term money in them. What's wrong with that?

A: Investors will lose. It used to be you could get your money out of a fund at the close of a business day. Now you can trade in and out of the S&P 500 all day in real time. Don't ask me what kind of a nut would want to do that. It works against investors because if you have a big collapse in the market, and you get out at noon, the odds are pretty good the market will be up by the close. In the long run, trading is just a big distraction. Warren Buffett believes this. He said that 90% of the trust he's leaving to his wife should go in the Vanguard 500 Index Fund.

Q: If he'd asked, would you have suggested the more diverse Vanguard Total Stock Market Fund instead?

A: Yeah! I wrote him about that. I didn't hear back from him. An even more interesting question is why he doesn't use international. Everybody's talking about how you have to have international, but I don't know why.

Q: Why not? More than half of the stocks you could buy, by market capitalization, are outside the U.S.

A: In the long run, market returns are created by business returns. And I think American business and the American economy are going to be the strongest in the world. I think we have more innovation. I think we have better technology. And I know we have a better legal structure, better shareholder protections. Some foreign nations are fine, but not all.

I've said if you want to hold non-U.S. stocks, go to 20%. Now people are saying 40%. You know, if you go from 20% to 40%, and foreign stocks out-perform by two percentage points per year—which would be astonishing—that's a 0.40 percentage point benefit. So my own view is it's not worth it.

Q: What about the benefits of diversification or the idea that going abroad can lower overall risk because markets aren't correlated?

A: Diversification is certainly true, but noncorrelation is bunk. It's applying higher mathematics to something I don't think requires it. We've overanalyzed the whole thing. I'm always the apostle of simplicity and lower costs.

Q: Since 2000, fees charged by mutual funds have been coming down. Have you won that argument too?

A: Forty or so of the 50 largest fund groups are owned by publicly traded companies. They are in business to earn a return on capital for that company's investors, and that's the great conflict. They become great big marketing companies. They hold the line on fees, conceding only where they have to or for PR purposes. The cost structure of the industry is insane—50% profit margins are not unknown.

Q: You set up Vanguard so that it's owned by its own funds, which in turn are owned by fund investors. It seems to me that idea is as important to you as indexing.

A: The conflict of interest in the industry isn't about indexing vs. active management. It's cost. The point of the Vanguard structure is to eliminate the management company's profit. Compare what investors pay at Vanguard to what they pay at a competitor, and we're saving shareholders a total of $14 billion a year.

Q: What's that mean, to cut out the profit? Vanguard keeps costs low, but people must certainly be making financial services industry salaries.

A: I never said we have low costs. I've said we have low expense ratios. That's very different. If you multiply Vanguard's average 0.14% expense ratio by its $3 trillion in assets, that's total expenses of about $4 billion. Go back to when we had about $1 trillion in assets, charging 0.21%—that's about $2 billion. So Vanguard's costs have gone from $2 billion to $4 billion. When you have 20 million shareholder accounts, it costs money. When you're employing 15,000 people all over the world, it costs money. We don't disclose executive compensation anymore, which I think is a little strange. [Bogle stepped down as Vanguard's senior chairman in 1999.] I designed the best company that I could design. But there are ways to make it better.

Q: What are some things you would have done differently?

A: I would have made it mandatory that we continue to disclose executive compensation. And maybe make the company's financial statements more broadly available. I think openness is important if you're a company like Vanguard because these people own not only your funds but the management company too. They're entitled to any information they want. If it's painful to disclose, well, that's too bad.

Q: Okay, index funds win, but I still have to decide how much to invest in stocks. Should I worry that stock prices look high?

A: For most investors, if you're around the norm of 60% stocks and 40% bonds, I wouldn't vary it much now. But based on today's low stock dividend yields and bond yields, be prepared for a period of low returns compared to history.

Q: So then why bother with stocks?

A; Well, put your money in a money-market account, and you get 0.1%. You have to invest, but you can't control the returns. And you should know that if you do stretch for higher returns, you'll be taking on extra risk.

Q: One critic of indexing, money manager David Winters, says that because index funds own a stock no matter what, corporate boards have no incentive to rein in executive pay.

A: He just doesn't know what he's talking about. There is, as far as I can tell, no difference between the corporate governance activity of actively managed funds and index funds. They're both very low. But think through the logic of it: The old Wall Street rule was, if you don't like the management, sell the stock. In the case of an index fund, the rule has to be, if you don't like the management, fix the management, because you can't sell the stock. So I look at indexing as the great hope of governance.

Q: You're concerned that the financial sector is too big. Why?

A; The job of finance is to provide capital to companies. We do it to the tune of $250 billion a year in IPOs and secondary offerings. What else do we do? We encourage investors to trade about $32 trillion a year. So the way I calculate it, 99% of what we do in this industry is people trading with one another, with a gain only to the middleman. It's a waste of resources.

Q: What keeps you at this? Why are you sitting here talking to me instead of, I don't know, looking at paintings in Venice?A: It's a little bit that you carve out, probably inadvertently, the kind of person you are. And people expect you to be that kind of a person. Those kinds of expectations—Adam Smith called them "the invisible spectator"—shape what you do. And I guess I am just the type that likes to keep moving. I can't imagine starting a day not knowing what I'm going to do.

Read next: Vanguard’s Founder Explains What Your Investment Adviser Should Do