New research sheds light on the habits of successful savers

One of the infinite ways in which you can divide up the world into two types of people is savings behavior. People are either diligent savers or they aren't; likely, you know where you fit in without being told.

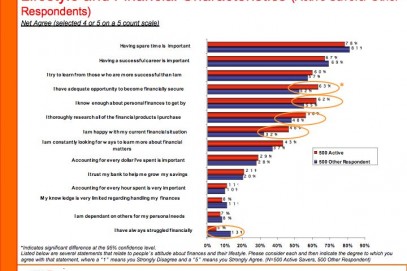

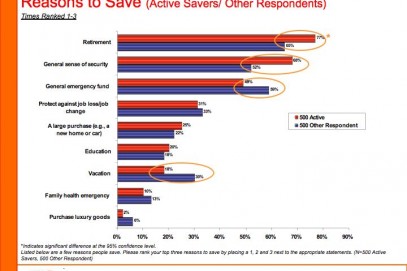

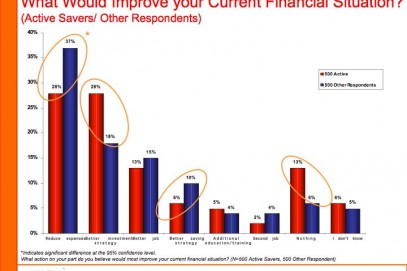

But other than the habit of savings, how are savers and spenders different from one another? Recently, I saw some research from HSBC Direct which sheds some light on the subject. In a survey of 1,000 people--two-thirds of whom had household incomes of at least $100,000--the bank found a few interesting differences between the 22% of the population that the bank designates as "active savers" and the not-so-active rest of us. (Click on each of the charts below to see larger-sized versions with more information; in all of them, the red bar signifies active savers while the blue one represents not-so-active ones.)

- Active savers start early. Seventy-three percent of them say that their parents taught them the value of saving money, compared to 56% of the so-so savers.

The pearls of Norwalk, C.T. range far from the numerous beaches overlooking the Long Island Sound, community gardens to a very vibrant arts and culture scene.City of Norwalk

The pearls of Norwalk, C.T. range far from the numerous beaches overlooking the Long Island Sound, community gardens to a very vibrant arts and culture scene.City of Norwalk