The Five Most Important Years for Your Financial Life

- Retire With Money: Take Care in Picking an Advisor

- Retire With Money: Relax, You Don't Have to Get Everything Right

- This Tax Trick Could Be Incredibly Useful in 2017

- Retire With Money: Don't Let Trump-Mania Derail Your Retirement Plan

- Two Congressmen Are Trying to Kill a Program That Helps People Save for Retirement

When you're saving and investing for retirement, you can make a lot of progress by staying on cruise control. Sign up for your 401(k), set a high savings rate, and continue stashing away money throughout your career. Occasionally, though, you'll reach pivotal ages when your retirement will require hands-on attention—you'll have to make a decision about your savings or health care, for example, that will affect your financial security or quality of life for years to come.

At these times your window of opportunity may last as little as a few months. So mark these five ages (or the ones that still apply to you) on your calendar.

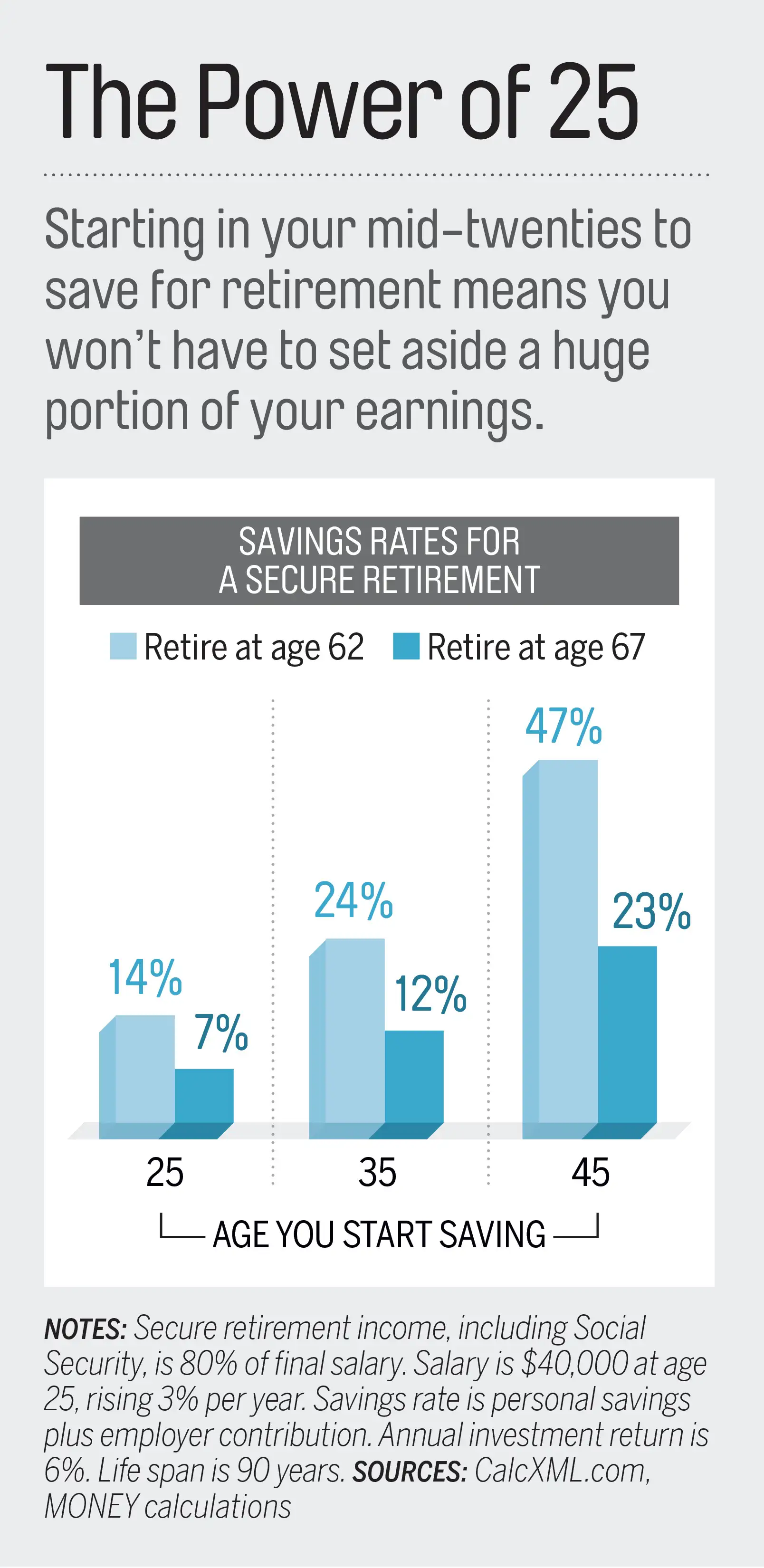

Age 25: Commit to Saving

Why this age is critical: When you're just out of college, saving can be hard. But halfway through your twenties—with a job or two behind you, and maybe grad school too—you're psychologically and financially ready to set money aside. Along with the monetary payoff of starting at 25 (see chart), you'll develop a habit that will serve you well for life, says Denis Horrigan, a financial planner in Farmington, Conn.

Key move: Aim to put away at least 10% of your pay in your workplace plan, if you have one, or a Roth IRA. Feeling pinched? Use a free app to divert small amounts into savings. Acorns.com rounds up your debit or credit card transactions to the nearest dollar, funneling that change into an investment account.

Age 45: Turn Up the Volume

Why this age is critical: You're near your peak earning year—for men, 48, and for women, 39, PayScale found in 2014—so you can power-save. And you most likely have fewer working years ahead of you than behind you, so retirement has to be a priority, says Brooklyn planner Tom Frederickson.

Key move: Use online tools and retirement calculators to estimate how much retirement income your portfolio will generate. While forecasts aren't perfect, they can inspire. A 2014 study out of Stanford and the University of Minnesota found that seeing such estimates helped spur workers to boost their savings.

Age 60: Suss Out Social Security

Why this age is critical: The earliest you can receive Social Security, generally, is at 62, but claiming strategies, especially for married couples, can be complicated. "These are big decisions, and most people need a couple of years to figure out what's right for them," says Jim MacKay, a financial planner in Springfield, Mo.

Key moves: Although some 40% of retirees claim at 62, look for ways to hold off; monthly benefits grow 7% to 8% a year until you're 70. While you wait, build up one to two years of cash to cover emergencies and daily expenses. To lower the risk of a bear market crushing your nest egg, slowly shift your investments so you end up with an appropriately conservative portfolio by your expected retirement date. Most advisers suggest arriving at a 50%/50% stock/bond mix.

Age 65: Enroll in Medicare

Why this age is critical: Unless you or your spouse is still working and you're on an employer plan—coverage via COBRA doesn't count—you have three months after the month you turn 65 to sign up for Medicare (at medicare.gov). Miss the deadline and you'll pay higher premiums—for example, 10% more for each year you delay Medicare Part B (for doctors).

Key move: Shop around for a Part D plan for drug coverage and a Medigap plan to help pay extra costs, such as co-payments and deductibles. Compare choices at medicare.gov/find-a-plan. And go to shiptacenter.org to connect with local experts and trained volunteers providing free guidance on all your Medicare options.

Age 70½: Tackle your taxes

Why this age is critical: Starting the year you turn 70½, the clock begins ticking on the required minimum distributions you must take from your 401(k) and IRAs. (You can defer your first RMD until April 1 of the next year, but you'll have to take a second one before year-end.) Miss an RMD and you'll pay a hefty 50% penalty on the money you should have withdrawn.

Key move: Get charitable. In 2015 Congress made permanent a rule letting direct donations from your IRA—up to $100,000 a year—count toward your RMD (and perhaps lower your tax bill). So if you don't need the money, you can find it a good home.