4 Ways to Bridge the Retirement Income Gap

If you're on the verge of retirement, you've probably heard this Social Security advice: Delay claiming your benefit as long as possible, and it will increase by 7% to 8% each year you wait.

Great idea, except for one problem. Once you retire, how do you come up with enough money to live on until benefits kick in? Two-thirds of workers file before full retirement age—currently 66—and only about 2% wait until 70, when benefits max out.

The good news is that you can make waiting easier, assuming you have money saved up or have other sources of cash. Even if you defer claiming your benefit for only a year or two, you'll permanently boost your income and financial security. Here are four strategies for delaying.

Work ... Just a Little

Because Social Security will come to only a fraction of your salary—typically $20,000 to $25,000 if you retire at $100,000 a year—you need work only a fraction of the time to replace it. Some companies have phased-retirement programs letting older workers cut their hours; if your employer doesn't, maybe you can negotiate a schedule light enough to feel like retirement. Want a change? Start exploring part-time opportunities in new fields, suggests psychologist Robert Delamontagne, author of The Retiring Mind.

The upside is not just financial. "For many people," says Delamontagne, "working part-time, especially if you are highly engaged, can increase health and happiness."

Go Halfway

If you're married, both of you can delay claiming retirement benefits on your own work records at the same time that one of you receives Social Security money—payments that can be equal to half of what the other spouse would be due at full retirement age.

To do this, follow what's known as a file-and-suspend strategy, says Jim Blankenship, a planner in New Berlin, Ill. At full retirement age, the higher-earning spouse files for benefits, then suspends payments. Then the other spouse files for spousal benefits. If the primary earner is due, say, $2,500 a month at full retirement age, the spouse would receive $1,250. Meanwhile, the eventual monthly retirement benefits for each spouse—based on his or her own earnings—would continue to grow until he or she starts taking checks or reaches age 70. Wait until you're both at full retirement age to do this, or your benefits will be trimmed.

Use the free Social Security calculator at FinancialEngines.com to see how this would work for you, or pay up for customized guidance at MaximizeMySocialSecurity.com ($40) or at SocialSecuritySolutions.com (starts at $20).

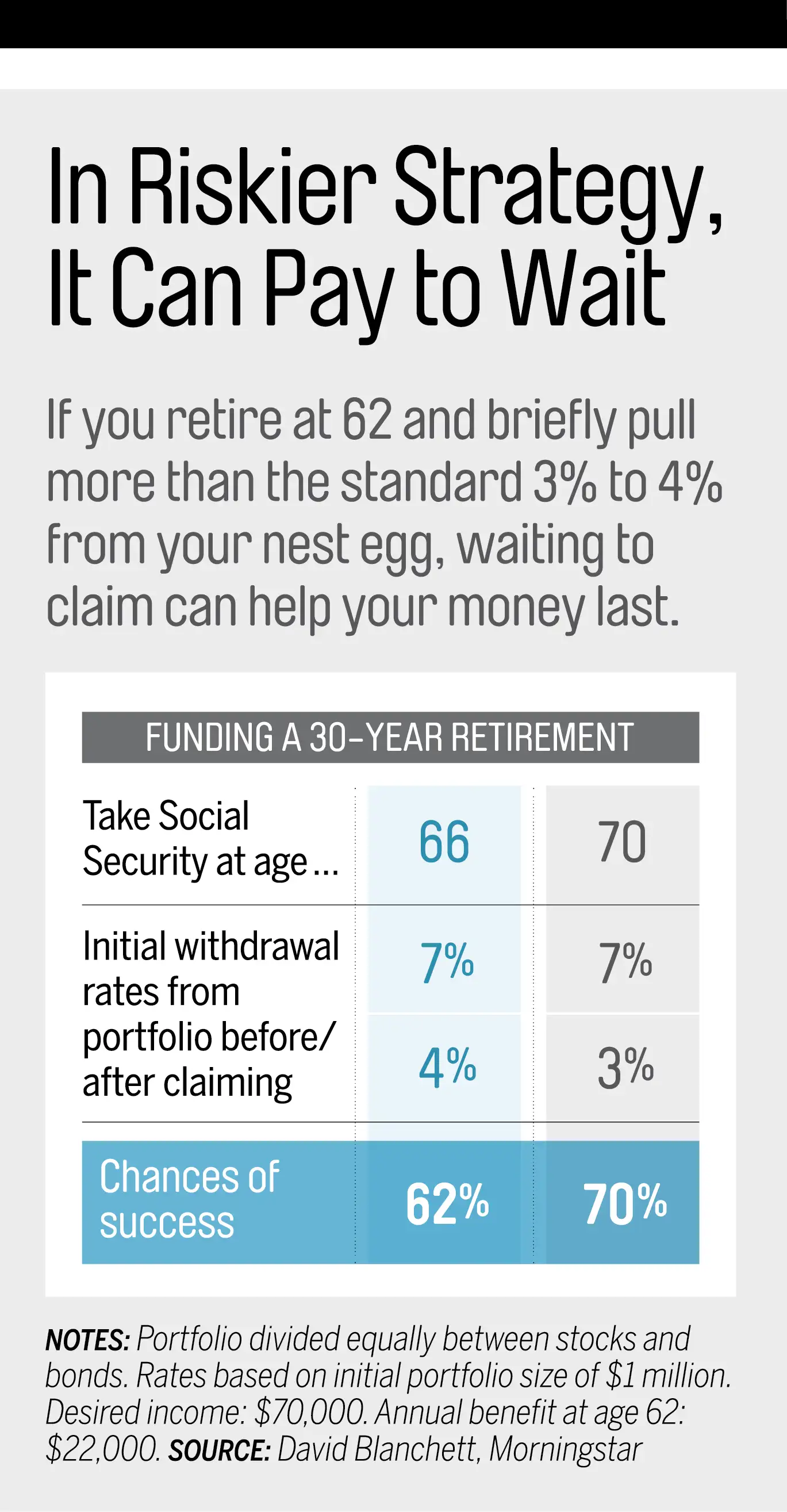

Take Bigger Withdrawls

Ideally, you would minimize the odds of exhausting your portfolio in retirement by limiting your initial annual withdrawal to 3% to 5% of your savings (then adjusting for inflation). If that's not an option, you might try the riskier strategy of starting at a higher rate, then lowering it once you claim benefits.

Although this approach may seem counterintuitive, the longer you wait to claim, the lower your chances of running out of money—as long as you keep your inflation-adjusted income level until you claim, says Morningstar's head of retirement research, David Blanchett. The gains to be had from a higher monthly benefit more than offset the increased drain on your portfolio (see the chart at left). But before you try this strategy, Blanchett advises testing it with a Social Security calculator or consulting a financial planner.

Start With Your 401(k)

Whatever your withdrawal rate, take advantage of your low tax bracket before Social Security and mandatory withdrawals from retirement accounts kick in. Pull money from your pretax accounts, such as your 401(k) or traditional IRA, where most of your investments likely sit, says Baylor University finance professor William Reichenstein, a principal at Social Security Solutions.

His reasoning: After age 70½ you'll have to take required minimum distributions from those pretax accounts. Added to your Social Security checks, those RMDs may generate more income than you need—and more taxes. (For married couples filing jointly and making over $32,000, up to 85% of Social Security benefits are taxed.) By withdrawing pretax money in your sixties, before you have to, you'll have smaller RMDs later, an easier time controlling your income, and a portfolio that—because you'll lose less of it to taxes—is more likely to last you in retirement.

Read next:This Is the Maximum Benefit You Can Get from Social Security