Retiring? Stay or Go, You've Got Moves to Make

Once you start looking at retirement over a horizon of five years or so, it’s time to start thinking about how you’ll manage your biggest single asset: your home.Whether you intend to stay put or move to that lake cottage, keeping real estate costs under control is key to your security.

Those costs may be larger than you think. On average, housing makes up one-third of spending for those ages 54 to 74—the largest single category. More than half of Americans ages 55 to 64 are carrying mortgages, higher than in previous generations. “Paying mortgage debt into retirement reduces your lifetime wealth and limits your spending,” says Pam Villarreal, a senior fellow at the National Center for Policy Analysis.

Staying in your house, with your mortgage paid, doesn’t free you from making decisions. Few pre-retirees think about adapting their homes for retirement living. “It’s hard for active people in their fifties or sixties to think about what they might want 15 years from now,” says Bonnie Sewell, a financial adviser in Leesburg, Va. Should you end up not being able to get around easily, though, you’ll have fewer choices and less ability to make them. So take action now:

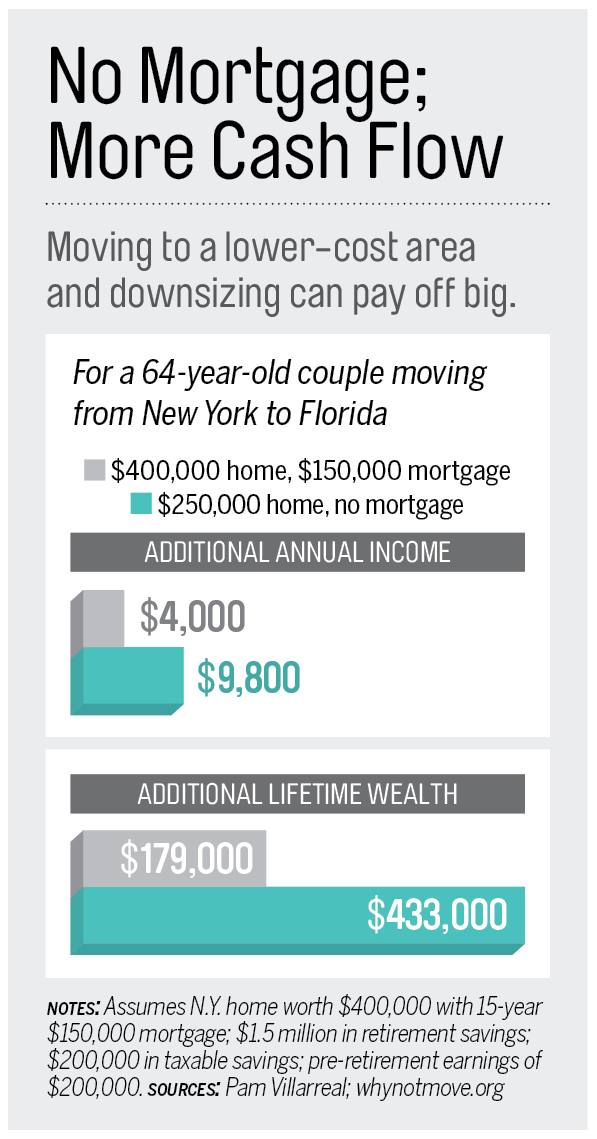

Moving? Don’t take your mortgage with you. Nearly 30% of boomers plan to relocate when they retire, according to a new AARP survey. Many of them are seeking to cut costs by moving to a lower-tax state. Carry a mortgage, however, and this strategy may not have a big impact on your cash flow, as a recent analysis by Villarreal found. Mortgage debt can easily erode the benefits of lower taxes. Run your own numbers at whynotmove.org.

Sure, if you’ve got plenty of cash, mortgage payments may not seem like an issue. But there’s security, and flexibility, in not carrying debt. “Many of my clients see having no mortgage payments as a way of freeing up cash for future health care costs,” says Philadelphia financial planner Cathy Seeber.

If you plan to stay, renovate now. By your late fifties, your kids are probably out of the house, and the tuition bills are behind you—or nearly so. Time to renovate? Use this opportunity to make a few additional changes that will let you stay in your home for the next couple of decades. “The last thing you want to do in your seventies or eighties is manage a major rehab in an emergency,” says Sewell.

If you have a house with stairs, make sure you can live on one floor if necessary, says Mary Jo Peterson, a design consultant in Brookfield, Conn. That may mean expanding a powder room to a full bath. You can also add design touches that appeal to people of all ages—a sloped entrance-walk instead of steps is more convenient for moms with strollers and college students dragging suitcases, not just the elderly. Find more ideas at aarp.org/livable-communities, and your family home can last for generations.