This Is How Much You Could Save If You Got Rid of One of Your Cars

- 'Once-in-a-Lifetime Deals': Buying a Car During Coronavirus Isn't Easy, But You Could Save Big

- 6 Ways To Avoid Taxes Like a Millionaire

- How to Prepare Your Home for Winter and Lower Your Heating Bills

- 5 Easy Ways to Make Your Old Home Feel New

- 5 Home Improvement Projects That Are Easy and Affordable

If your household is like most, you probably have two or three vehicles in your driveway: one for yourself, one for a spouse, maybe one for a teen. Indeed, 57% of U.S. families own two or more cars, KPMG found. Between gas, maintenance, fees, and insurance, the average cost to owners was $4,375 per vehicle in 2015, AAA found—even while fuel prices plunged. That's money that you could be using for family trips or retirement planning. (The cash you'll get by selling won't hurt either.)

So could you save by dumping one vehicle? Over the past half-dozen years, new car- and ride-sharing services have revolutionized the way people get around, creating a new set of alternatives. IBM forecast this year that the number of consumers 35 and older who use car- and ride-sharing as primary modes of transportation will more than double by 2025.

Attitudes have shifted too: "Owning a car today feels like a burden to many people," says Ben Stanley, the IBM study's co-author.

Abandoning car ownership altogether might not be practical. But eliminating even one vehicle could pay off for many families. Follow these steps to calculate whether you would benefit by cutting back.

Know Your Baseline

First, understand how your family racks up mileage, says Atlanta financial planner Brandy Wright. In particular, look at how often you use multiple vehicles at the same time; consider not only commuting but also night and weekend trips.

If you doubled up only a few times a week, you're a strong candidate for downsizing, says David Levinson, a civil engineering professor and researcher at the University of Minnesota's Center for Transportation Studies.

Then, to compare costs, understand what you're spending now. Charge all your gas purchases? Check your account statements to see last year's damage. Add what you spent on maintenance and insurance. If you have a lease or loan, factor that in. Average new-car payments were about $482 a month last year, Experian says.

Price Out Alternatives

Now figure out how you'll cover times that you need more than one car. Your commute may be the biggest hurdle, so consider whether you or your spouse can use public transit or a carpool, or buddy up with colleagues and split the gas.

For other trips, you may need a family heart-to-heart. Can you coordinate your schedules to cut the number of times you'll have a conflict? Once you've reduced those, fill in the gaps. The closer you live to a city, in general, the more options you'll have. If you just need a few one-way trips, try taxis or ride-sharing services. Nationwide, the average Uber trip runs about $16, according to SherpaShare.

For weekend errands, particularly if you're hauling groceries or other goods, car sharing may work better. Zipcar, for example, offers a $70 annual membership (plus a $25 one-time fee) with weekend hourly rates starting at $8.50. Families can save $154 to $435 a month by using car-sharing services, UC–Berkeley's Transportation Sustainability Research Center found.

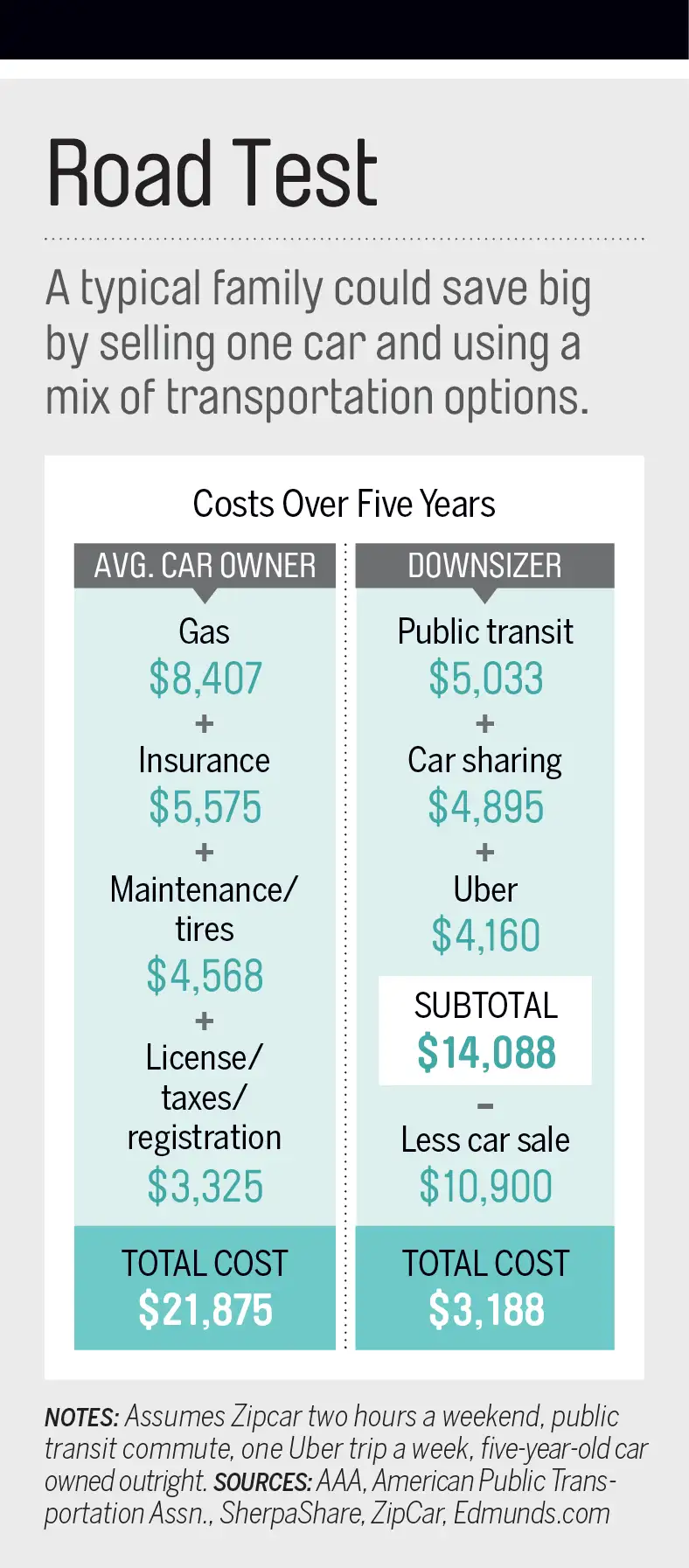

Whatever the best options for you, tally the costs and compare them to what you're spending now. (See chart below.)

Now figure out which vehicle to sell. The more a car is worth, the more you'll gain by scaling back, but be practical: If you chauffeur your kid's swim team around, you obviously can't dump the minivan and keep the coupe. The average five-year-old vehicle goes for $10,900 in a private-party sale, Edmunds.com says. (Driving an old clunker into the ground? Selling it may make environmental sense, but not financial.)

If you have outstanding car loans, sell the most valuable vehicle you can live without, then pay off the debt.

Tip the Scale

Still on the fence? Tweaking some transit habits might make downsizing pay off. Bundling errands into a single day, for instance, may save money on car sharing, says Susan Shaheen, co-director of the Berkeley research center.

And try to avoid Uber's hated surge pricing, which hikes fares at times of high demand. To do so, you may just need a little patience, says Northeastern University professor Christo Wilson, co-author of new research from Northeastern investigating Uber's costs. "Surge prices often last less than 10 minutes," he explains.