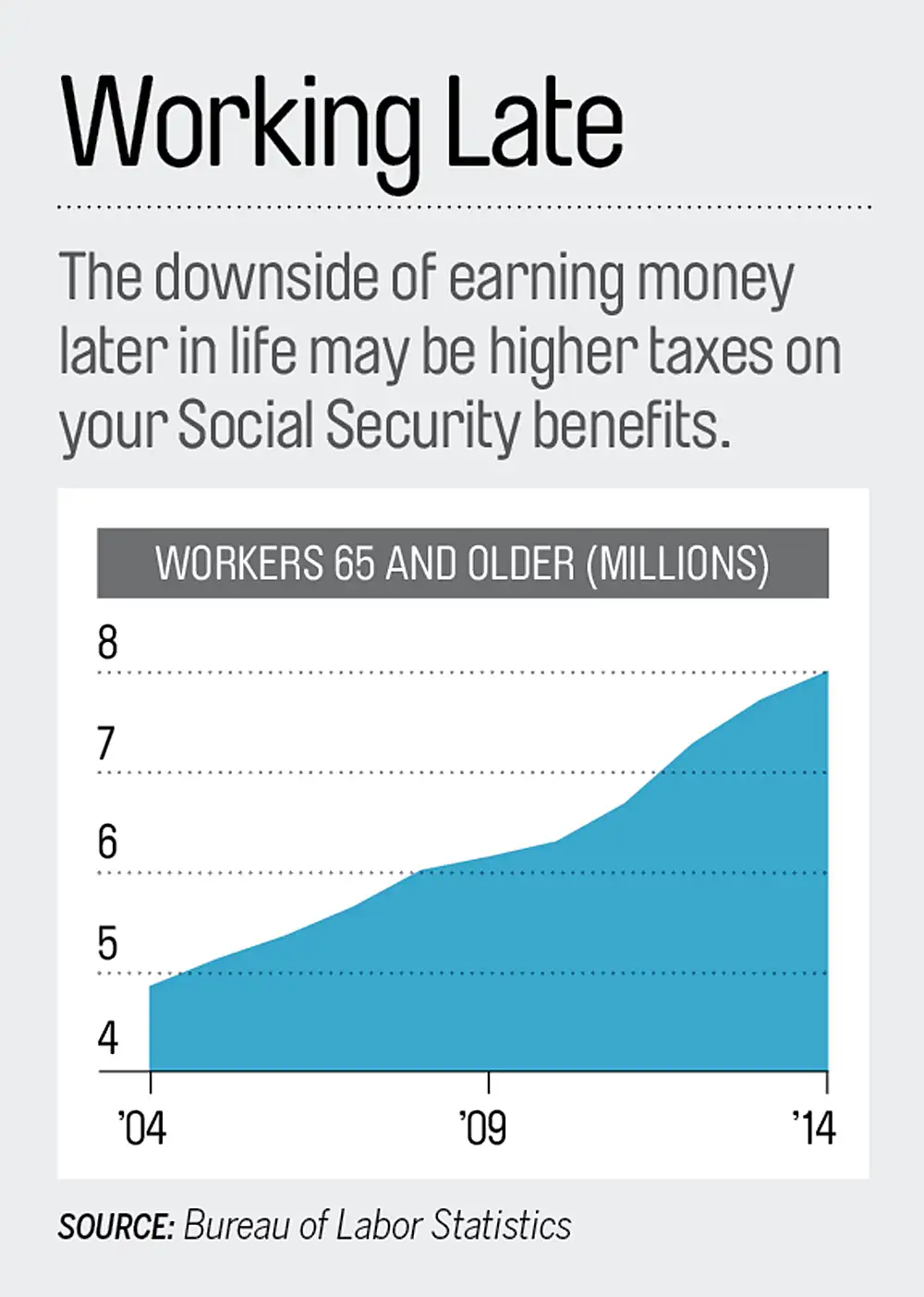

The Taxing Problem With Working Longer

The question of when and how to file for Social Security is a tough one for many retirees—I regularly field questions on the topic. Recently a reader wrote to say he'd like to draw Social Security benefits at age 66 yet keep working until 75. What are the tax implications?

When you continue to work and draw Social Security, your benefits are reduced temporarily if you're 65 or younger and your outside income exceeds certain levels. After 65, these reductions do not apply. You may, however, owe taxes on your Social Security income.

How Earnings Can Hurt

Not all of your Social Security income is taxable. Social Security uses a measure it calls "combined income" to determine how much of your benefit is taxable, and it can be tricky to understand.

To determine your combined income, take your adjusted gross income (check last year's tax return), then add any nontaxable interest income and half of your Social Security benefit. (If you haven't started claiming, you can get a projection online by setting up an account at ssa.gov.)

If the total is less than $25,000 ($32,000 on joint tax returns), you owe no income taxes on your Social Security benefits. If the total is between $25,000 and $34,000 ($32,000 and $44,000 on joint returns), you may have to pay taxes on half of your Social Security that's over that threshold. Above that, 85% of your benefits may be taxable—the top rate.

Here's how that could play out. Take a retiree in the 15% federal tax bracket who is taxed on 50% of his Social Security. When he earns another $1,000, his so-called combined income rises by that much too, subjecting another $500 of Social Security income to taxes. So the tax bill on that $1,000 won't be $150 (15% of $1,000) but $225 (15% of $1,500), for an effective rate of 22.5%.

Your Workarounds

Beefing up your tax-free holdings, especially Roth IRAs, can mean money coming in that won't trigger more taxable Social Security income. (Working less lowers your tax bill too, but you're usually better off earning the money.)

If you can live on just your salary, deferring Social Security until age 70 also helps. Your taxes should be lower while you wait. And delaying benefits will increase your monthly Social Security payments by 8% a year (plus annual inflation adjustments).

Hedging Your Bets

Single retirees should think about one other option: filing for and suspending Social Security benefits at age 66. By doing so you will be able to request a lump-sum payment for all the suspended benefits

anytime until age 70.

Even the best of plans can change, so that payment could come in handy if you face an emergency cash crunch. But there's a downside: Once you request a lump sum, your payout will be valued as if you took benefits at 66, as will your regular monthly benefit going forward.

Philip Moeller is an expert on retirement, aging, and health. His book, “Get What’s Yours: The Secrets to Maxing Out Your Social Security,” was published in February by Simon & Schuster. Reach him at moeller.philip@gmail.com or @PhilMoeller on Twitter.