Some Older Parents Are Missing Out on This Social Security Perk

Older parents, take note: If you have kids who won't graduate from high school until sometime after you turn 62, your family may qualify for extra dollars from Social Security. And those payments for dependent children may make it financially advantageous to file for retirement benefits earlier than you might otherwise.

Your kids can't collect until you do. But the potential benefit is large enough to merit special attention in deciding when you should file, says Kurt Czarnowski, a retirement-planning consultant and former Social Security Administration employee. In some cases, the combined benefit starts out higher than the amount the parent would receive if he or she waited until reaching full retirement age (FRA), now gradually rising from 66 to 67.

Here's how it works: A child under age 18 (or 19 if still in high school) can collect benefits of up to half of what a parent would get at FRA—even if that parent claims benefits at 62. Today that can amount to as much as $16,122 a year for children of high earners.

If you have multiple kids, they can all collect until they age out. An annual family maximum limits total payments to between 150% and 180% of your FRA benefit.

But as with other Social Security issues, you can't be certain if filing earlier or later will be more beneficial. "That depends on how long you live," Czarnowski says.

You can start your retirement benefits at any point from age 62 through 70. The younger you start, the more payments you will receive, but the smaller they will be. As a general rule, many financial planners suggest delaying to full retirement age or later. The larger check helps protect you from coming up short late in life, and it locks in a larger potential survivor benefit for a spouse who outlives you.

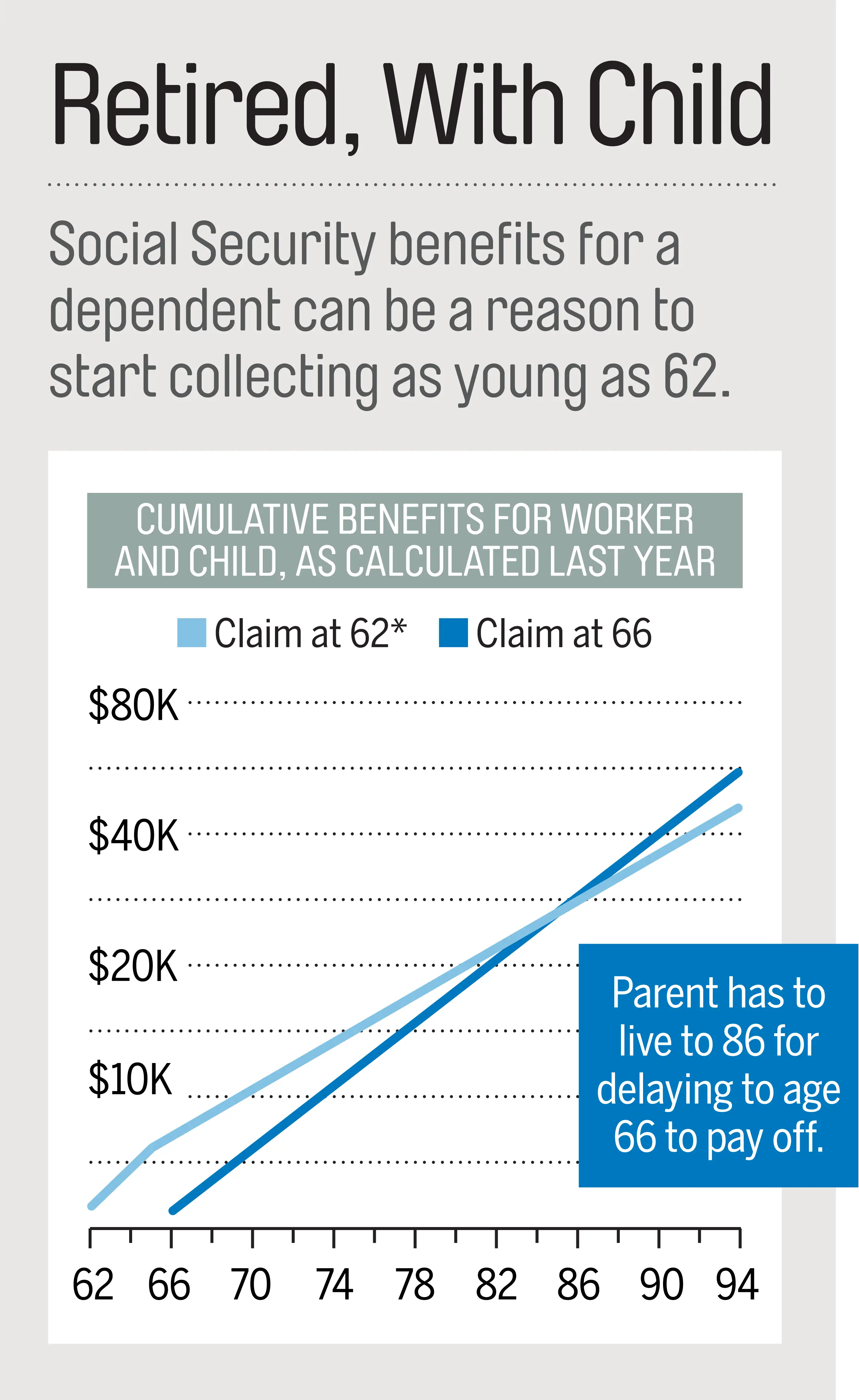

But with minor dependents, claiming benefits earlier becomes more enticing. Consider a parent, 62, with a 14-year-old son and a monthly benefit of $2,000 at full retirement, says William Reichenstein, a Baylor University professor and head of research at Social Security Solutions. If he or she waits until 66 to claim benefits, the son, at 18, will be too old to collect. But if the parent had filed at 62 last year, the family would be getting $1,500 a month for the parent plus $1,000 for the child until he ages out.

The chart above, calculated for that parent who filed last year at 62, shows that he or she would have to live to 86 for early filing to lose its advantage, Reichenstein says. Without minor children, the break-even point would be reduced to roughly 12 years after full retirement age.

One big caveat: Benefits for your kids may not be available before full retirement age if you are still working. Under Social Security's earnings test, some or all of your benefits are withheld if your annual income exceeds certain thresholds. If you lose your benefits, your dependents also lose theirs. You can recoup those payments later, but your kids can't.