You'll Never Guess the Latest Victims of the Student Loan Crisis

Most debt you can get out of—painful as it might be. Credit card debt can be cleared in bankruptcy. A mortgage can end in foreclosure. But student debt is more sticky, and it turns out it can have big consequences in retirement.

Last year, Richard Minuti’s Social Security payments were cut by 10%.

The Philadelphia native was already earning only a bit over $10,000 a year, including some part-time work as a tutor. “I was desperate,” says Minuti. “Taking 10% of a person's pay who’s trying to live with bills, that's the cruelty of it."

The Treasury Department was taking the money to pay for federal student loans he had taken out years before. Just before age 50, Minuti had gone back to college to get a second bachelor’s degree and a better job in social work and counseling. But the non-profit jobs he landed afterwards were lower paying, and he defaulted on the debt.

Student debt’s painful new twist

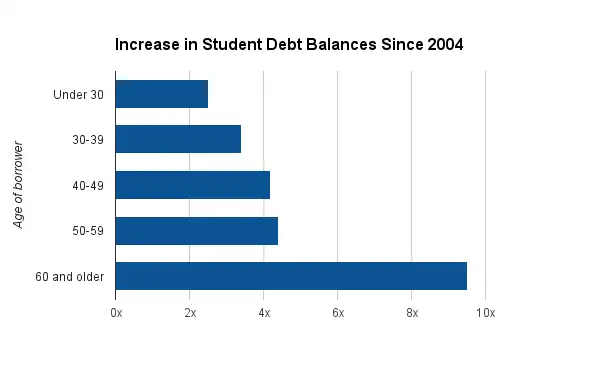

Minuti is one of the small but expanding group of seniors who are hitting retirement with a student debt burden. Over the past decade, people over the age of 60 had the fastest growing educational loan balances of any age group, according to the Federal Reserve Bank of New York. The total amount grew by more than nine times, from $6 billion in 2004 to $58 billion in 2014.

Only about 4% of households headed by people age 65 to 74 carry educational debt, according to a 2014 U.S. Government Accountability Office report. But as recently as 2004, student loans balances in retirement were close to unheard of, affecting less than 1% of this group.

Educational loans are very difficult to pay off when you are in or near retirement. Unlike a new college grad, there’s little prospect of years of rising salary income to help pay off the loan. That’s one reason older debtors have the highest default rate of any age group. (Also, most people who can’t pay off a loan will eventually age into being included among older debtors.) Over half of federal loans held by people over age 75 are in default, according to the GAO.

Student loan debts can’t be discharged in bankruptcy. And, as Minuti learned, federal tax refunds and up to 15% of wages and Social Security can be garnished.

This can be devastating, says Joanna Darcus, consumer rights attorney at Community Legal Services of Philadelphia.

“Most clients find me because the collection activity that they're facing is preventing them from paying their utilities, from buying food for themselves, from paying their rent or their mortgage,” says Darcus, who works with low-income borrowers.

The number of seniors whose Social Security checks were garnished rose by roughly six times over the past decade, from about 6,000 to 36,000 people, says the GAO. Legislation from the mid-1990s ensured recipients could still get a minimum of $750 a month. At the time, this was enough to keep them from sliding below the poverty threshold. But to meet the current threshold, Congress would need to increase this to above $1,000 a month.

In other words, with enough debt, a Social Security recipient can be pulled into poverty.

“That’s pretty stressful for seniors when they understand that,” says Jan Miller, a student loan consultant who has seen a rise in his senior clients.

What’s behind the rise?

It’s not, despite what you might guess, only about parents who are taking on loans for their kids late in their careers.

https://img.money.com/2015/06/ross_seniordebt_audio_v1.mp3Listen: How to decide if you should take out loans for your children's education

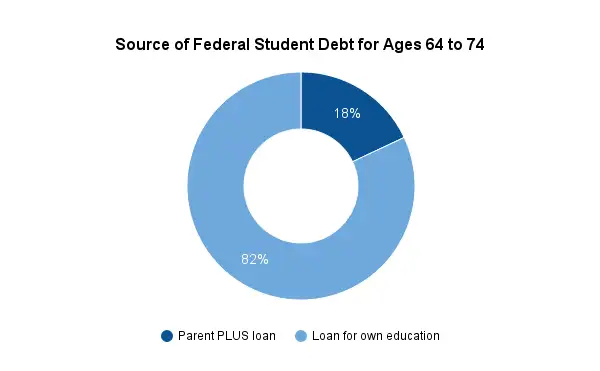

In the GAO data, about 18% of federal educational debt held by seniors was from Parent PLUS loans for children or grandchildren. The remaining 82% was taken out by the borrower for his or her own education. (The GAO data differs from the New York Fed’s, showing lower total balances, so it may be missing some parental borrowing.)

Darcus says many of her clients turned to education as a solution to unemployment and long-stagnant wages. Enrollment for all full and part-time students over age 35 increased 20% from 2004 to its recessionary peak in 2010, according to the National Center for Education Statistics.

“Among many of my clients, education is viewed as a pathway out of poverty and toward financial stability, but their reality is much different from that,” Darcus says. “Sometimes it's their debt that keeps them in poverty, or pushes them deeper into it.”

And in recent years, both tuition and older debts have been especially difficult to pay, as home values and household assets took a hit in the Great Recession. Meanwhile, of course, the cost of higher education has soared. Tuition for private nonprofit institutions is up 78% in real dollars since 2004, according to the College Board.

What may be changing

New regulations and legislation this year may bring some relief to educational loan borrowers. The Senate in March introduced legislation to make private loans, but not federally subsidized loans, dismissible through bankruptcy.

For federal loans, more favorable income-driven repayment plans may be extended to up to 5 million borrowers this year. These plans, which have been growing in popularity since launching in 2009, adjust monthly payments according to reported discretionary income. The Department of Education is scheduled to issue new regulations by the end of 2015 that may allow all student borrowers to cap payments at 10% of their monthly income.

But it is unclear what percentage of that 5 million people are older borrowers who would benefit. Some borrowers have also complained that income-driven repayment plans require too much complex paperwork to enroll and stay enrolled. Borrowers who want to find out if they are already eligible for income-driven repayment plans can go here.

Parent PLUS loans would not be included in the new regulations. However, Parent PLUS loans can still be consolidated in order to take advantage of a similar, albeit less generous option, called the Income Contingent Repayment plan. This plan allows borrowers to cap their monthly payments at 20% of their discretionary income.

Still, some feel the best way to help seniors with student loan debt is to stop threatening to garnish Social Security benefits altogether. This spring, the Senate Aging Committee called for further investigations of the effects of student debt on seniors.

“Garnishing Social Security benefits defeats the entire point of the program—that’s why we don’t allow banks or credit card companies to do it,” said Sen. Claire McCaskill of Missouri in a statement.

Getting out from under

Richard Minuti was able to enroll in an income-based repayment plan last year with the help of a legal advocacy group. Because Minuti earned less than 150% of the federal poverty level, the government set his monthly obligation at $0, eliminating his monthly payment.

“I’m appreciative of that, thank God they have something like that,” Minuti says, “because obviously there are many people like myself who are similarly situated, 60-plus, and having these problems.”

But Deanne Loonin, director of the National Consumer Law Center's Student Loan Borrower Assistance Project, says she doesn’t see the trend of rising educational debts ending any time soon. And some seniors will struggle with this debt well into retirement.

“I've got clients in nursing homes who are still having their Social Security garnished and they were in their 90s,” she says.