This is How Much Money You Should Have in Stocks — at Every Age

- There Are Now More Crypto Coins Than U.S Stocks

- The Best Time to Buy Bitcoin, Explained in One Chart

- This Two-Minute Viral Video Proves It's Impossible to Time the Stock Market

- AMC, GameStop and Hertz: What's Causing the Latest Meme Stock Swings?

- 5 Signs Investors Are Dangerously Overconfident Right Now

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

If you want a secure retirement, you can’t just save. You also need to make sure your investment portfolio keeps pace with inflation. For most Americans, that’s going to mean investing in the stock market, whether inside a 401(k) or at an online brokerage. But determining how much of your money to put in stocks can be tricky.

When you’re young, the hardest part may simply be getting started. In your forties, it’s riding out the market’s ups and downs without losing your cool. After you finally retire, you need to make those hard-earned savings last.

Understanding some simple investing precepts can make the job a lot easier—and up your odds of success. To get started finding the right balance of stocks and bonds for you, read on.

Starting Out

The conundrum: This is the time when you are supposed to invest fearlessly, taking big risks, so you can reap big rewards years down the road. But it’s easier said than done.

The generation that came of age during the Great Recession hasn’t had an easy time financially. After graduating into the weakest job market in memory, you’ve found yourselves saddled with record amounts of student-loan debt, as well as soaring rents and home prices.

As a result, many young people don’t have a lot left over to invest. One recent study by the National Institute on Retirement Security found two-thirds of millennials have nothing saved for retirement.

Even millennials who are ready to invest don’t necessarily favor stocks. Blame, perhaps, memories of the 2008 market crash, which took place when the oldest millennials were in their mid-twenties. “Just when they entered the workforce, they lived through the second--largest stock market drop in history,” says Brian Schmehil, a financial planner in Chicago.

A recent Bankrate survey asked millennials about their favorite long-term investments. More than half said cash or real estate, while only 23% cited the stock market. The rest listed overly conservative options like gold and bonds or overly speculative ones like crypto-currencies.

The solution: Invest just a little to get started. While setting aside money may be hard, it’s easier than ever to get in the market. Over the past decade, more and more 401(k)s have begun auto-enrolling participants. Unless you opt out, your employer may have already taken the leap for you.

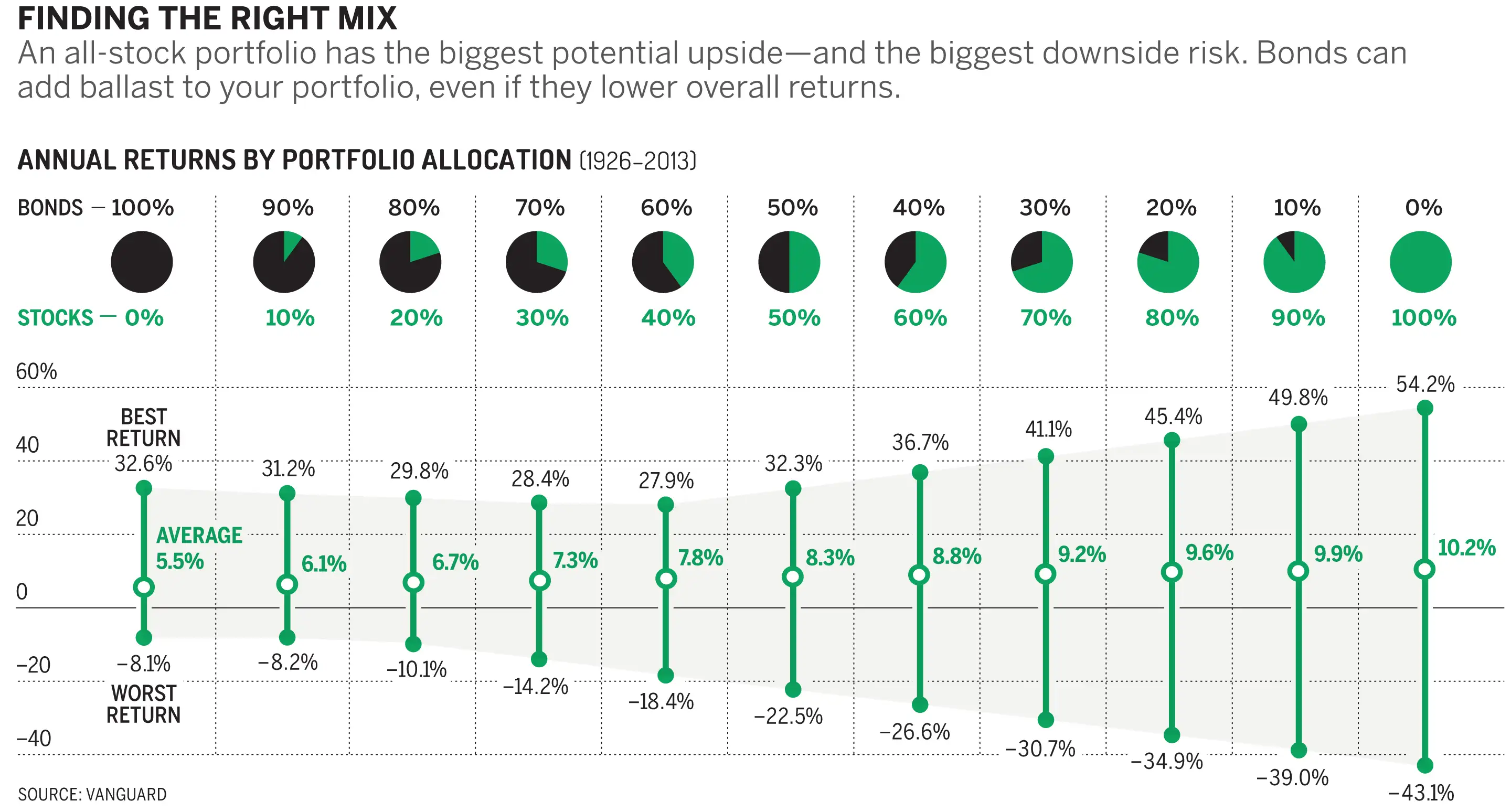

While you may not have much money to invest at first, in some ways you can think of that as an advantage. Experts say now is the time to be aggressive, with 85% to 90% of your investments in stocks, and 10% to 15% in bonds. Stocks offer more growth potential, along with more volatility, while bonds have less upside but throw off regular income. With just a few thousand (or even a few hundred) dollars at stake, the prospect of losing a third or even half your investment in the next bear market shouldn’t seem too terrifying.

One way to think about it, says Wade Pfau, professor of retirement income at the American College, is to consider your coming years in the workforce as part of your overall investment portfolio. “Your future salary behaves like a bond”—a steady income stream to help you ride out rough markets, he says. Of course, simply knowing you have time to recoup your losses doesn’t mean riding out big market dips will be easy. But you won’t have to wait as long as you might think for the stock market to get back into growth mode. Going back to the 1920s, stock investors have endured eight different bear markets, hitting roughly once a decade. While stocks lost about 40% of their value on average each time, the duration of the downturn—measured from the month the market hit its last high until the month it bottomed out—was relatively short: about 1.4 years, on average.

Mid-Career

The conundrum: By the time you’ve reached your forties, you should have a good amount saved for retirement. Ideally, according to investment firm Fidelity, you should have socked away three to four times your annual salary by now. In reality, the average 401(k) average balance for savers in their early forties is about $87,000.

But either way, you’ve still got decades before retirement, and your savings should be on an upward trajectory. That means you should own plenty of stocks—-especially if you’re behind on saving and hoping for investment gains to help you make up some of that lost ground.

Nonetheless, it’s not quite so simple as when you were in your twenties and early thirties. Now that you’ve got a real nest egg, market gyrations can start to feel awfully scary. (If you have three times your salary saved, a 33% market decline is roughly equivalent to losing a year’s worth of pay.) There’s a real risk that when the market plunges, you’ll panic and decide to sell your investments at a low price. “When the market recovers, it recovers quickly,” Schmehil says. “You can miss out on a lot of appreciation.”

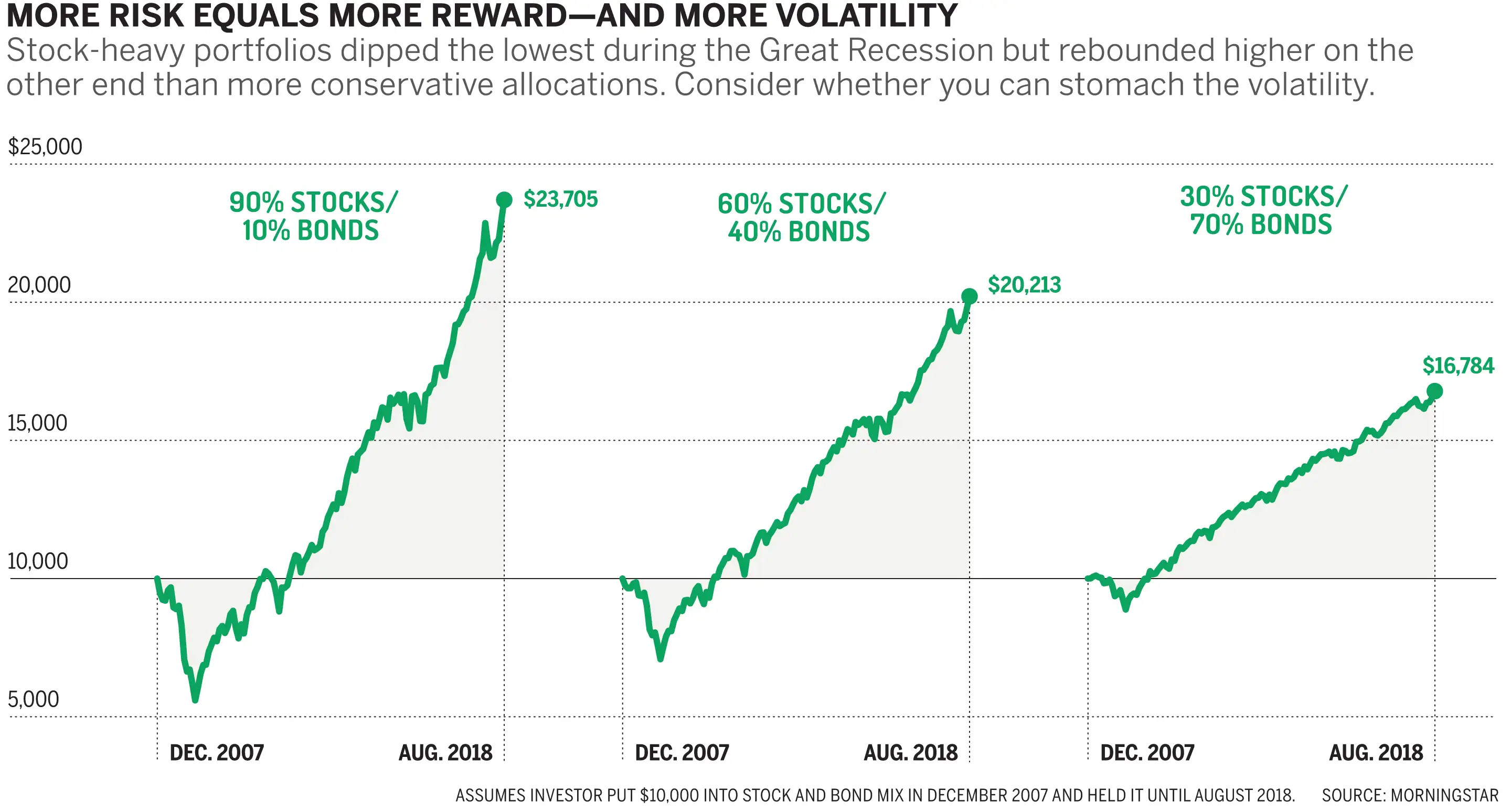

History suggests that’s often exactly what happens. In the five years from the 2008 financial crisis, investors yanked more than $500 billion from U.S. stock funds, according to the trade group Investment Company Institute, while pouring roughly $1 trillion into bond funds. In fact, the stock market hit bottom in March 2009, before embarking on what would ultimately become a nearly decade-long bull market.

The solution: While you may still be decades from retirement, it’s time to start gradually dialing back your hefty stock exposure. Chances are you’ve felt pretty good about stocks these days. Over the past decade the Standard & Poor’s 500 has returned over 14% a year on average.

But, most planners warn, the potential gains from a more aggressive portfolio—with, say, 80% or more in stocks—no longer match the big costs. “When you’ve seen 10 years of almost uninterrupted gains, it’s easy to be complacent,” warns Houston financial planner Ashley Foster. “But when something happens—and it will—you could be exposed.”

Increasing your bond holdings just a little can make riding out downturns much less stressful. Most professional investors recommend gradually moving your portfolio along what is often called a “glide path,” from 80% to 90% stocks in your early forties to 50% to 60% in your late fifties.

If you invest in a target-date fund within your 401(k), this will happen auto-matically. If you plan to handle your portfolio yourself, Foster recommends sitting down at least once a year to do a “gut check” on your portfolio: “Ask yourself, How would I feel if the market went down 10% tomorrow?” Would you be okay?

If you want extra help, one option is to take a quiz that accounts for not just your age and net worth but your risk tolerance too. This is what typically happens if you hire a financial advisor or a robo-advisor. But there are plenty of online versions available for free.

Retirement

The conundrum: For years, the investing world had a well-known formula for calculating your stock allocation: 100 minus your age. Following the rule would mean the oldest boomers, now in their early seventies, would have less than 30% in stocks and more than 70% in bonds.

Many financial planners, however, now see this advice as outdated. While the Federal Reserve has gradually raised interest rates, they remain near 40-year lows. Investors who retired 25 years ago, in the early 1990s, could count on 10-year Treasury yields of nearly 6%. Today those rates are about half that—3%, even after the Fed’s recent rate hikes. (Inflation is lower, but only slightly, about 2.5% today vs. about 2.6% in 1994.)

Meanwhile, today’s investors are living a lot longer too. In 1980, men age 65 could expect to live to age 79 on average and women 83. Today it’s 83 and 86, respectively, according to the Society of Actuaries. While that’s good news, the combination of stingy interest rates and longer life spans means it’s that much harder to count on bonds to fund your entire retirement.

The solution: Many financial planners say the old bond-centric mindset is out-of-date. Instead, you need to maintain a focus on stocks. In fact, today the typical all-in-one target-date fund has about 40% in stocks for investors on the threshold of retirement, with some comfortably above 50%, according to Morningstar.

Increasing your stock holdings can dramatically boost the chances that your savings will last. An investor with a portfolio consisting entirely of bonds, who spent 4% of his savings each year, would have only a 24% chance of making it through a 35-year retirement without running out of money, based on historical returns, according to one recent study by RBC Capital Markets. By contrast, if that same investor moves 25% of his savings to stocks, his chances of success would jump to nearly 70%. With 50% in stocks, the chances jump to 96%.

In general, the bigger share of your savings you hope to spend each year, the more you need to count on the market to boost your portfolio. If you aimed to spend just 3% of your savings a year, your chances of success with an all-bond portfolio jump to more than 70%. If you need to spend down 5% each year, they drop below 10%. “When you are behind on saving, you need to be more aggressive” in terms of stocks, says Dennis Nolte, a financial planner in Winter Park, Fla.

There is another wrinkle. While investors can expect some down years in retirement, the timing of the market-decline years can mean the difference between your savings lasting or not. The biggest risk is a severe bear market in the first few years after you leave the workforce, because it could force you to spend big chunks of your savings, rather than giving them crucial extra years to compound.

To head off that risk, one line of thinking put forward in a recent -academic paper by Pfau and another financial planner posited that investors might consider following what has been described as a U‑shaped stock-bond glide path: That is, a portfolio that begins -aggressively when you are young, grows gradually more conservative around retirement time, then becomes more aggressive again. The authors suggested retiring with 20% to 40% of your portfolio invested in stocks, then gradually upping those levels to between 40% and 80%.

While few pros would go that far, Rand Spero, a financial planner in Lexington, Mass., says this relatively new thinking has helped change the way investors approach the issue: “Don’t follow the traditional advice to just keep blindly reducing and reducing your stocks.”

Instead, you need to do a little math. Look at what would happen if the stock market took a big plunge—say, by 50%—and figure out how your portfolio would fare, factoring in the reality that you’ll need those savings to pay your living expenses before the market recovers. If you feel confident your investments can weather the storm, feel free to increase your stock market exposure, making it more likely your money will last your whole life, with perhaps something left over for your heirs. Spero has clients well into their eighties and nineties, and he says they rarely end up with less than 30% of their portfolios in stocks.