When It Comes to Inflation, Beware the Consensus

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

History shows that when investors are all but convinced that the markets or economy are headed in a certain direction the market finds a way to surprise. Case in point: the smart money was absolutely convinced that interest rates would rise this year. Well, we've reached another "beware the consensus" moment, and you ought to be aware of it.

A big reason why interest rates have sunk is that Wall Street has begun to buy into certain assumptions about the nature of the economy. Among the beliefs: The global economy is stuck in a prolonged period of below-average growth — so low, in fact, that interest rates will stay low and inflation will not be a threat for the foreseeable future.

Bill Gross, bond guru at PIMCO — where strategists have dubbed this development "the new neutral" — recently told clients that this new mindset has been "substantially reflected in current asset prices." This would explain why investors have been piling into bonds, whose modest returns have historically been ravaged by inflation, pushing yields lower. They simply aren't worried because they don't consider inflation a long-term threat. Hence, a bet on bonds makes perfect sense.

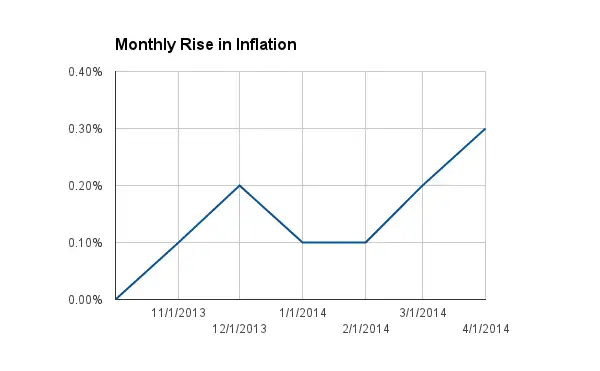

Yet recent government data show that consumer prices, while not out of hand, are certainly starting to climb on a monthly basis...

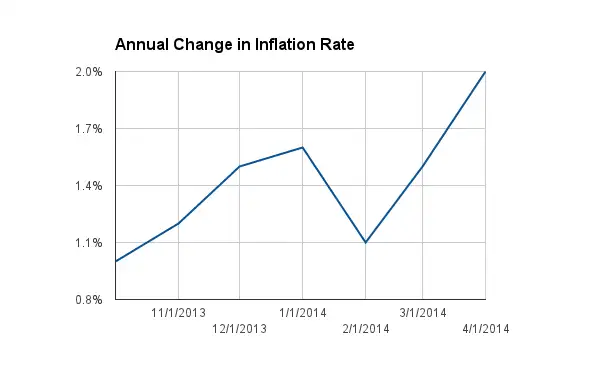

...as well as on an annual basis:

Add to this the fact that for the first time in a while, consumer prices are rising along with wages, says James Paulsen, chief investment strategist & Economist at Wells Capital Management. In the long run, rising wages pose a big threat to overall inflation.

Combine that with some of the other ingredients being stirred in what Paulsen describes as the "overheat cocktail — including a dovish Fed, a globally synchronized recovery, an unemployment rate that's headed toward 6%, among other factors — and you start to wonder," Paulsen says.

"Is the bond market prepared should a mini-overheat/inflation/is-the-Fed-behind-the-curve panic evolve in the next several months?" he asks.

To be sure, inflation running an annual rate of around 2% seems rather benign. Indeed, Sam Stovall, managing director for U.S. equity strategy at S&P Capital IQ, notes that historically, inflation at 4% is "the 'line in the sand' above which stock prices have begun to post average monthly declines."

However, there are two things that investors need to be mindful of:

1) The Federal Reserve has set a target rate of inflation of 2% that it's shooting for. While the Fed doesn't rely on CPI for its measure of prices, other inflation gauges also show that prices are beginning to get close to the Fed's 2% mark. If prices rise above that rate, as they are threatening to do, that would give the Fed even more reason to take its foot off the gas and to start lifting rates to decelerate the pace of growth.

2) While investors would embrace inflation running at 2%, consumers are having a harder go of it. Why? Because CPI does not reflect the real impact of rising household prices. Gasoline, for instance, is up around 3% over the past year. Car insurance is up 4.4%. Propane costs are up nearly 8%. Milk prices are up more than 6%. Beef is up more than 11% at the grocery store. And citrus fruits are about 20% more expensive than they were last year. All according to the Department of Labor.

The fact that food prices are rising so much "is especially difficult for those households that live paycheck to paycheck," says Chris G. Christopher, Jr.

director of consumer economics at IHS Global Insight.

This may already be having an impact on the consumer economy. Even as consumer prices and incomes rose in April, overall household consumption fell slightly. And if consumers pull in the reins, the market will have to take notice.