5 Biggest Trends That Will Affect Your Money in 2018

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

On a day-to-day basis, Wall Street seems to have the attention span of a gnat. One day, stocks sell off because of perceived gridlock in Washington or another crisis in North Korea. The next day, equities are just as likely to rebound because iPhone sales are going through the roof or Amazon just found another industry to disrupt.

It all sounds random. But over time, there's a method to the market's madness. Events that reflect or affect the direction of the economy will always move stocks.

Last year, for example, global equities in general and Chinese shares in particular soared by more than 20%, foreshadowing the reacceleration of the Chinese economy.

But with the global economic cycle maturing, "there are going to be fewer growth surprises" going forward, says Richard Turnill, global chief investment strategist for BlackRock.

So you'll have to choose your targets more carefully, and take note of the big investment trends that are expected to arise in 2018, such as rising interest rates, blockbuster breakthroughs in health care, and accelerating international growth—just to name a few.

1. U.S. Interest Rates Rise

If you smell inflation in the air, you have a better nose than most people. The consumer price index has risen just 2% over the past 12 months, according to the Bureau of Labor Statistics. That's well below the long-term average of 3%.

Nevertheless, economists expect the Federal Reserve to nudge short-term rates higher at least twice more in 2018, bringing the key short-term Federal funds rate to just below 2%.

Why would the Fed push rates higher if inflation isn't rearing its ugly head? Partly because the Fed wants to be proactive, and inflation tends to rise when unemployment is low. As of October, unemployment fell to 4.1%, the lowest since 2000. And the Fed's main tool for fighting recessions is cutting rates—a tactic of limited use when rates are hugging zero.

So what does that mean for you? If you're a saver, a higher Fed funds rate means modestly higher savings rates. "If you shop around, you might be able to do better than 2% on a one-year CD at some point in 2018," says Greg McBride, chief financial analyst for Bankrate.com.

Don't make the mistake of buying long-term certificates of deposit, though, McBride says. Periods of rising rates can last a long time. Right now, the rate difference between one-year and five-year CDs isn't much, and locking into a 2% yield for more than a year can look foolish if short-term rates start climbing back to their historical norms.

Rising short-term rates could also nudge up returns for long-suffering money-market mutual fund investors. Currently the Vanguard Prime Money Market Fund yields 1.2%. Two or more rate hikes could lift top-performing money funds above the 2% mark.

There is a dark side to higher savings rates, though—and that's higher interest rates on home-equity loans, credit cards, and adjustable-rate mortgages.

And a 2% yield could even temper stock gains. Frustrated income investors have been pouring money into dividend-paying stocks for years just to get the payout. But dividend-paying stocks tend to fall out of favor when rates are rising and bonds start to offer higher yields than stocks.

2. Economies Overseas Rebound

"America first" isn't just a political slogan. For much of the past decade, it turned out to be a smart way to manage your portfolio. The S&P 500 index of blue-chip stocks gained an average 8.3% a year in the past decade since the worst of the global financial crisis, while the MSCI Europe, Australasia, and Far East (EAFE) index of foreign shares gained less than 2% a year. Investors who ventured into the volatile emerging markets such as China and Brazil earned less than 1%.

But U.S. stocks are no longer the only belles at the ball. International markets hopped out of bed and started dancing in 2017, as economies abroad accelerated faster than the U.S. EAFE stocks were up 23% last year while the emerging markets rose more than 30%.

"One of the trends that we see is the continuing improvement of global economic growth," says Stephen Wood, chief market strategist for North America at Russell Investments. Indeed, while the U.S. economy is expected to grow 2.5% this year, global GDP is forecast to grow 3.2%.

How can you capitalize on the shift? "People should be using the strong rally in the U.S. to fund a global rebalancing strategy," says Wood. In other words, it's time to take some profits from your U.S. exposure to buy foreign.

Where to start? Foreign shares based in developed markets such as Europe and Japan look relatively attractive. The price/earnings ratio for foreign shares, based on 10 years of corporate profits, currently stands at a modest 17, which is 33% lower than their historical valuation. By contrast, U.S. shares trade at a P/E ratio of 31, which is 90% higher than their historical median.

Meanwhile, the European Commission, which is responsible for managing the day-to-day business of the European Union, predicts the EU grew at its fastest pace in a decade in 2017 and should grow faster yet in 2018.

On our Money 50 recommended list of mutual funds, Oakmark International (OAKIX) is a top-rated portfolio that invests nearly 80% of its assets in undervalued European stocks. The fund has outperformed more than 95% of its peers over the past five, 10, and 15 years.

Emerging markets should also continue producing gains—though probably not as big as last year's, especially if the dollar were to gain strength (a strengthening dollar reduces the gains of Americans investing abroad while a weakening dollar amplifies your gains). For long-term investors who can stomach the risk, emerging markets offer the best growth potential, says Robert Doll, chief investment strategist for Nuveen.

On the Money 50 recommended fund list, go with T. Rowe Price Emerging Markets Stock (PRMSX), which has beaten more than 85% of its peers over the past one, three, and five years. If you prefer a single fund to cover all the foreign markets, Vanguard Total International Stock (VXUS) brings you the world for just 0.11% a year.

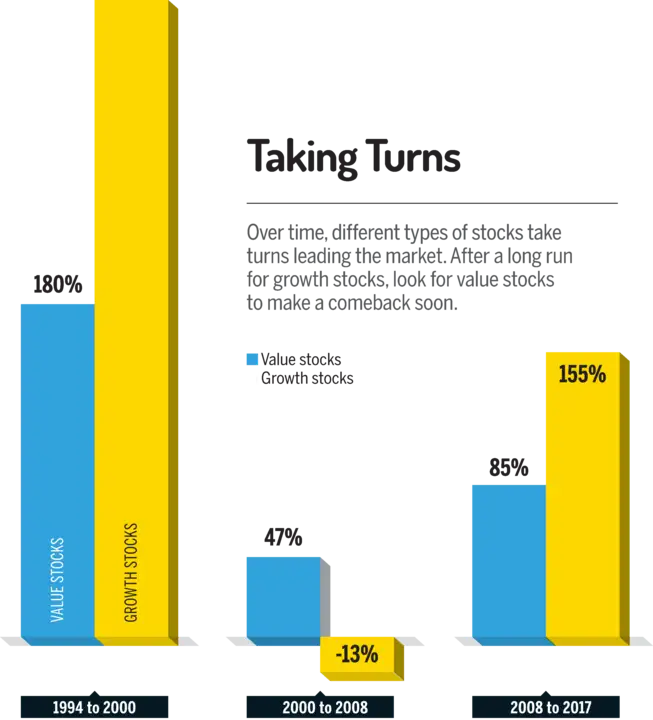

3. Assets Revert to the Mean

In the long run, two things are certain: One is that we're all dead, as economist John Maynard Keynes pointed out. And eventually, outperforming and underperforming investments will return to their long-term average performance.

This phenomenon—called "reversion to the mean"—is something you should keep in mind in 2018 as you review your portfolio.

For example: U.S. equities are divided into two basic groups: "growth" stocks, which are shares of fast-growing companies that often trade at a premium to the broad market, and "value" stocks, or shares of beaten-down or overlooked companies that are trading at discounts. Over the past decade, the average growth stock has returned 159% vs. just 89% for value.

Sooner or later, value investing will start to outperform growth, says Sam Stovall, chief investment strategist at the research group CFRA. "Don't be surprised if we see a reversion to value," Stovall says.

On our Money 50 recommended list of ETFs, PowerShares FTSE RAFI U.S. 1000 (PRF) tilts toward blue-chip value stocks. The typical holding in the fund trades at a P/E ratio of 19, which is a 10% discount to the broad market.

Other areas that might be due for a resurgence:

Energy funds: Still stinging from the collapse in oil prices that began in 2014, energy funds and energy master limited partnership funds are among the few categories in the red for 2017. Even a modest upturn in energy prices could help these funds regain ground. On the Money 50 ETF list, you can go with iShares North American Natural Resources ETF (IGE), with more than 80% in energy.

Inflation-protected bond funds: Inflation has been deader than Cleopatra's coffin, and the average inflation-adjusted bond fund has actually lost 0.5% a year for the past five years, according to Morningstar. But Wall Street could be underestimating long-term inflation: The 30-year projected inflation rate on Treasury Inflation-Protected Securities, or TIPS, is 1.9%—well below the long-term average of 3%. As a hedge, check out Vanguard Inflation-Protected Securities (VIPSX).

4. Health Care Remains Healthy

If any sector of the economy should have been roiled last year, it was health care. Republicans mounted an unsuccessful attempt to repeal the Affordable Care Act and then continued efforts to chip away at it.

Nevertheless, health care funds soared in 2017, posting average gains of more than 20%. Betsy Lind, investment analyst at Orbis Investment Management, isn't surprised. "The health care system is such a complicated Rube Goldberg system. It's hard to change."

A diversified health care fund has some potent medicine to keep its stamina up. The first is demographics. Not only is the baby-boom generation getting older, requiring more health care, more households are achieving middle-class status globally, which means they can afford more treatment. The number of people who can afford Western-style health care in China and India is growing by 5% to 10% a year, and that means growing global demand for new drugs, treatments, and devices.

The second is the revolution in genetic diagnostics and therapy. That's why Lind says the promising segment of health care is large-cap biotechnology, such as Gilead Sciences (GILD), with treatments for HIV and hepatitis, and Celgene (CELG), working on cancer therapies. It's been 15 years since the completion of the Human Genome Project, and companies are only now beginning to convert advances in genome-sequencing into actual therapeutics. The biggest biotech and pharmaceutical companies are well positioned to capitalize on these developments.

To capture both the domestic and international opportunities in this sector, consider iShares Global Healthcare ETF (IXJ), which counts Swiss drugmaker Novartis (NVS) among its top holdings as well as Gilead Sciences and Celgene.

5. The New Normal Sets In

The soaring stock market in 2017 belies a more subdued reality: The U.S. economy is in the late stages of a longer-than-expected expansion and remains mired in subpar growth. Meanwhile, both the stock and bond markets—because of their frothy prices and outsize gains in recent years—are expected to deliver below-average gains over the coming decade.

Research Affiliates, for instance, projects that both U.S. blue-chip stocks and core bonds will return less than 3% a year over the next decade—a fraction of their historical gains.

There's little investors can do about the market. But in a low-return environment, it's more important than ever to preserve what little you do earn.

The good news: In 2017, most of the major mutual fund providers—including Charles Schwab, Fidelity Investments, and Vanguard—dropped the expense ratios on their exchange-traded funds. That means you can now cobble together a portfolio of U.S. stocks, foreign equities, taxable bonds, and money-market securities for less than 0.25% of assets a year.

Currently Morningstar lists 39 ETFs with expense ratios of 0.10%, all of which could serve a useful function in your portfolio. On our Money 50 recommended list of ETFs, the Vanguard 500 ETF (VOO) and Schwab U.S. Broad Market ETF (SCHB) both offer you exposure to a broad market index for 0.04% of assets a year or less. Similarly, you can get access to the total fixed-income market through Vanguard Total Bond Market ETF (BND) for just 0.05% a year.

A study by Morningstar found that low costs consistently lead to better after-fee performance—when it comes to broad stock market funds, sector funds, foreign funds, bond funds, and balanced funds.

The world changes minute by minute, but in the investment world, there's precious little that you can predict or control. Low fees are one tool you can use to improve your performance. So why wouldn't you?