There's a Smart New Way for Investors to Use ETFs

- 4 Big Investing Trends You Can Bet On for the Next Several Years

- How You Can Hang Onto a Small Company That Grows Up To Be a Big Winner

- 5 Biggest Trends That Will Affect Your Money in 2018

- 3 Signs That You Should Be Dumping Your Stocks

- How to Bet on Amazon Without Actually Buying Its Insanely Expensive Stock

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

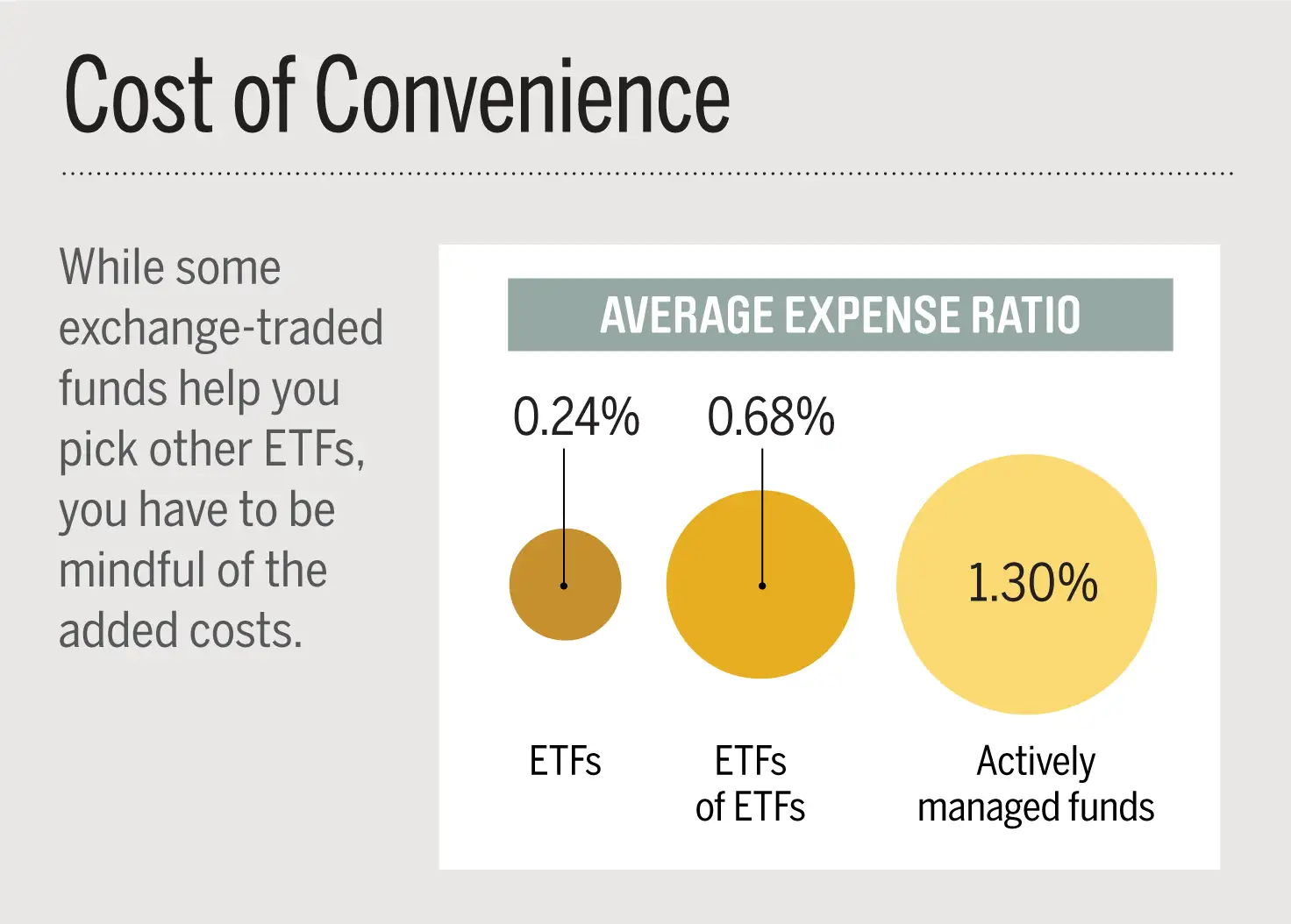

There are now more than 2,400 exchange-traded funds to choose from. Some are terrific low-cost investments, while others are the financial equivalent of hemlock. So how do you choose?

You could hire an advisor, but that might cost 1% of assets or more a year, neutralizing the low-cost reasons for buying ETFs in the first place. Or you could look to ETFs that invest in other ETFs.

"ETFs of ETFs" isn't a new concept. Mutual funds investing in other funds have been around for years. Just as with those "funds of funds," you have to be mindful of high fees. These ETFs "are hardly cheap, but they're not egregious," says ETF.com's Dave Nadig. You just have to know how to use them:

The No-Cost Option

Unlike mutual funds, most ETFs disclose their holdings daily, meaning you can piggyback on their best ideas—without being a client. For instance, by examining Cambria Global Asset Allocation ETF (GAA), which has beaten 95% of its peers over the past year, you'll know which real estate ETFs (Vanguard REIT) or inflation-protected bond ETFs (SPDR Bloomberg Barclays TIPS) that it thinks are best.

The Low-Cost Option

Some ETFs of ETFs expose you to specific timely strategies, while others are all-in-one portfolios of stock, bond, and other ETFs that you can buy and hold. The latter ones tend to be the better deals.

That's partly because they must compete with low-cost asset-allocation funds and therefore must be cheap themselves. Plus, ETFs are a cost-effective way to gain exposure to really broad asset classes. Take iShares Core Moderate Allocation (AOM). This balanced ETF invests in a mix of iShares-run ETFs that hold U.S. stocks, foreign equities, and bonds—and rebalances annually. The fund has beaten 60% of its peers over the past five years, and charges just 0.25% in expenses.

The Higher-Cost Option

ETFs of ETFs that focus on specific stock strategies have had a more difficult case to prove. First Trust Dorsey Wright Focus 5 ETF (FV) invests in the five First Trust–run ETFs that exhibit the greatest momentum and reviews that portfolio every two weeks, making changes as necessary.

Holding this ETF back: Its 0.89% expense ratio, its attempt at market timing, and its increasing size. And when you have just five holdings in a $2.5 billion fund, selling one holding can cause a big jolt to that underlying ETF, says Todd Rosenbluth, senior director of ETF and mutual fund research at CFRA.

To be sure, all-in-one ETFs of ETFs may also invest in only half-a-dozen or so funds. But those asset-allocation ETFs don't make adjustments on a weekly basis. Plus, "getting the asset allocation right can matter a lot more than individual securities selection," Rosenbluth says. "And if funds can do it cheaply, all the better."