Can a Once Shining Fund Regain Its Luster by Betting on Europe?

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

Named Morningstar's foreign-equity manager of the decade in 2010, David Herro has looked more like a dud of late, as Oakmark International , on our Money 50 recommended list, has ranked in the bottom 10% of its peers over the past three years. Adding to the worry are the retirement of co-manager Robert Taylor and the reopening of the fund after $3.5 billion in net outflows. "Owning a contrarian fund like this demands patience, as you can have a couple of lousy years," says Morningstar analyst Greg Carlson. "But its long-term prospects remain very, very good."

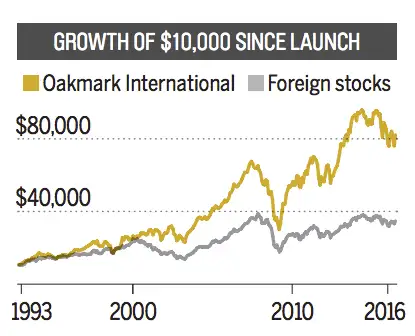

Despite recent troubles, the fund has trounced the field since its inception.

Herro, at the helm since the fund's 1992 launch, is sanguine about his recent struggles. "To outperform over the medium and long term there's a tradeoff with how you will sometimes perform over the short term," he says. In 2007 the fund also ranked in the bottom 5%, only to finish in the top 2% of its peers in three of the next five years. And while Oakmark returned an index-beating 4.5% a year over the past decade, the average investor earned just 1.7% from the fund by jumping in and out.

Rajat Jain of the Litman Gregory Masters International Fund, which uses Herro's team to run a portion of the Masters portfolio, adds that Taylor's retirement isn't cataclysmic: "It's certainly a loss, but Herro is the anchor and has a strong bench."

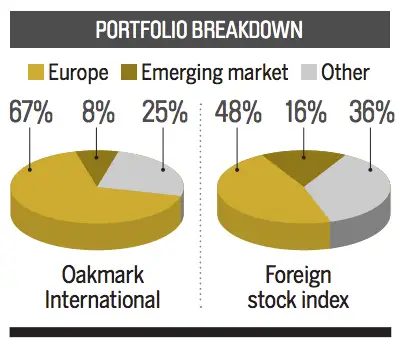

Oakmark International is willing to go against the foreign stock crowd.

"If you are going to pay for active management, you want something that looks different than an index," says Denis Smirnov of Gordian Advisors, which invests in active portfolios such as the fund along with passive funds. You're sure getting that in this value-minded portfolio.

The fund, which charges 0.95% in annual expenses, holds just 50 to 60 stocks—vs. 393 for its average peer—with big exposure to troubled Europe. Right now, Team Herro is leaning heavily toward unloved financial and consumer cyclical stocks but has no holdings in five sectors, including utilities and telecom. "We have a bifurcated market right now where safety is extremely expensive and everything else is extremely cheap," says Herro.

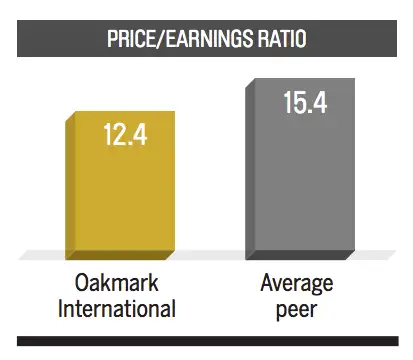

The portfolio is cheap thanks to bets on beaten-down European banks.

When European financials were slammed after Britain's Brexit vote, this fund added to its stakes in Credit Suisse, Lloyds, and Italian bank Intesa Sanpaolo. All three have posted double-digit gains since their Brexit lows. Conventional wisdom says European banks are hobbled by low rates that make it hard to profit from lending. Yet Herro, 56, says these banks have begun to grow earnings, and capital reserve requirements for European banks have nearly doubled.

Herro likens this situation to fear over European banks during the height of the Greek debt crisis. "We made good money when that extreme horror story didn't come true," Herro says. "I expect we'll make money when the market realizes today's fears are overblown."

NOTES: Foreign stocks based on MSCIWorld ex USA index. P/E based on projected profits for current year. SOURCE: Morningstar