The Incredible Shrinking Mutual Fund Manager

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

A generation ago, "actively managed" mutual funds—that is, portfolios run by traditional stock and bond pickers—weren’t just the norm; the managers themselves were larger-than-life figures such as Peter Lynch, John Neff, and Bill Gross.

Today you might not be able to name many of the pros who invest on your behalf, with perhaps the exception of Gross—though not for stellar recent performance, but rather due to the public spat between the "bond king" and Pimco, the firm that Gross put on the map.

This is to be expected. Over the past year, nearly 70% of the new money invested in mutual and exchange-traded funds has gone into index portfolios, like Vanguard Total Stock Market Index, now the biggest fund in the world.

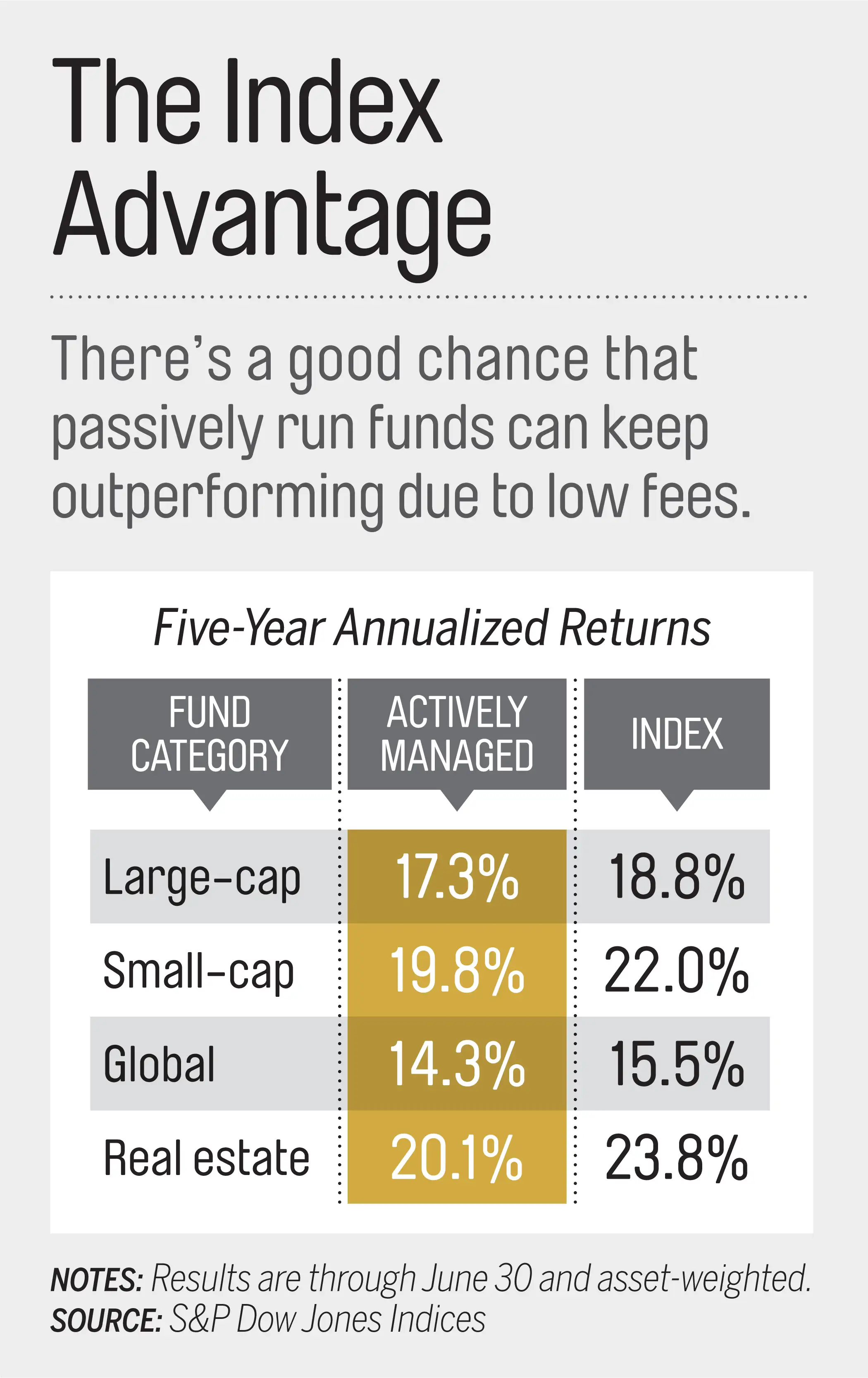

Such funds aren’t really managed at all. They don’t try to pick and choose the “best” investments, but rather hold all the securities in a market benchmark like the S&P 500.

Individual investors aren’t the only ones rethinking their approach. The influential California Public Employees’ Retirement System recently indicated that it intends to embrace more indexing in its $295 billion portfolio.

Why? Countless studies show that forces are stacked against the fund pros, which explains their poor performance (see chart). Over the past five years only two in 10 funds that invest in blue-chip U.S. stocks and three in 10 foreign funds beat their benchmarks.

That doesn’t mean that fund managers no longer have a place in your portfolio. Some — like those in the Money 50, our recommended list of funds and ETFs—have beaten the odds. Yet even those managers should play a limited role in your strategy.

Build your portfolio’s foundation with index funds

It’s not that professional investors are all lousy at their jobs. A study of more than 3,000 actively managed stock funds from 1979 to 2011 found that managers on average generated risk-adjusted returns that were actually better than their benchmarks. Trouble is, that’s before factoring in fees.

“There is indeed skill, but the average extra return managers generate is not enough to offset the average extra fees that come with active management,” says Lubos Pastor, a professor at the University of Chicago Booth School of Management, who co-wrote the study.

So use low-cost index funds and ETFs for the core part of your portfolio: your long-term stakes in U.S. and foreign equities and some bonds. While the average actively managed stock fund sports an annual expense ratio of 1.4% of assets, many index funds charge between 0.10% and 0.40%.

Rick Ferri, founder of the advisory firm Portfolio Solutions, suggests indexing at least 75% of your money. “Betting on the passive horse means you might not win every year,” he says, “but you know you are going to at least place.”

You can add managers to your core — but only the right kinds

“A low-cost actively managed fund can be as good as or better than an index,” says John Rekenthaler, vice president of research at Morningstar. He compared Vanguard’s low-fee actively managed portfolios in various categories with the firm’s index funds. All funds — both active and index — had total returns that ranked in the top 50% of their category for the past 15 years. But Vanguard’s active U.S. stock funds, international stock funds, and allocation funds actually had better returns than the index funds in those categories.

Examples of cheaper-than-average actively managed funds with a solid record in the Money 50 include Vanguard International Growth and Dodge & Cox International. Their annual fees are 0.48% and 0.64%, among the lowest for international equity portfolios. Even better, both are team-managed, which offers you protection in case one of the managers switches jobs or retires.

Treat active funds like specialty investments

There are some niche categories of investments where index funds themselves are costly to run and may not be that diversified. For those reasons, Ferri recommends you skip the index options for municipal or high-yield bond funds.

Also, there may be instances when you’d be willing to pay for unique strategies. FPA Crescent, with an expense ratio of 1.14%, mostly owns stocks. But lead manager Steve Romick is also willing to go to corporate bonds, preferred shares, or even cash if he sees better value.

That kind of flexibility makes it hard to use the fund for the bulk of your holdings. Still, in the past 15 years the fund’s 10% annual return doubled the S&P 500’s gains. And those are the kinds of big results you hope for when taking a chance on a fund manager.