The Best Ways to Invest in Bonds Now

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

The economy is finally gaining traction. Wages are rising faster than at any time since the global financial crisis. Inflation is reemerging—to the point where the Federal Reserve is signaling the need to raise interest rates possibly three times this year. And the Trump administration is primed to open the economic spigot even more with tax cuts and infrastructure spending.

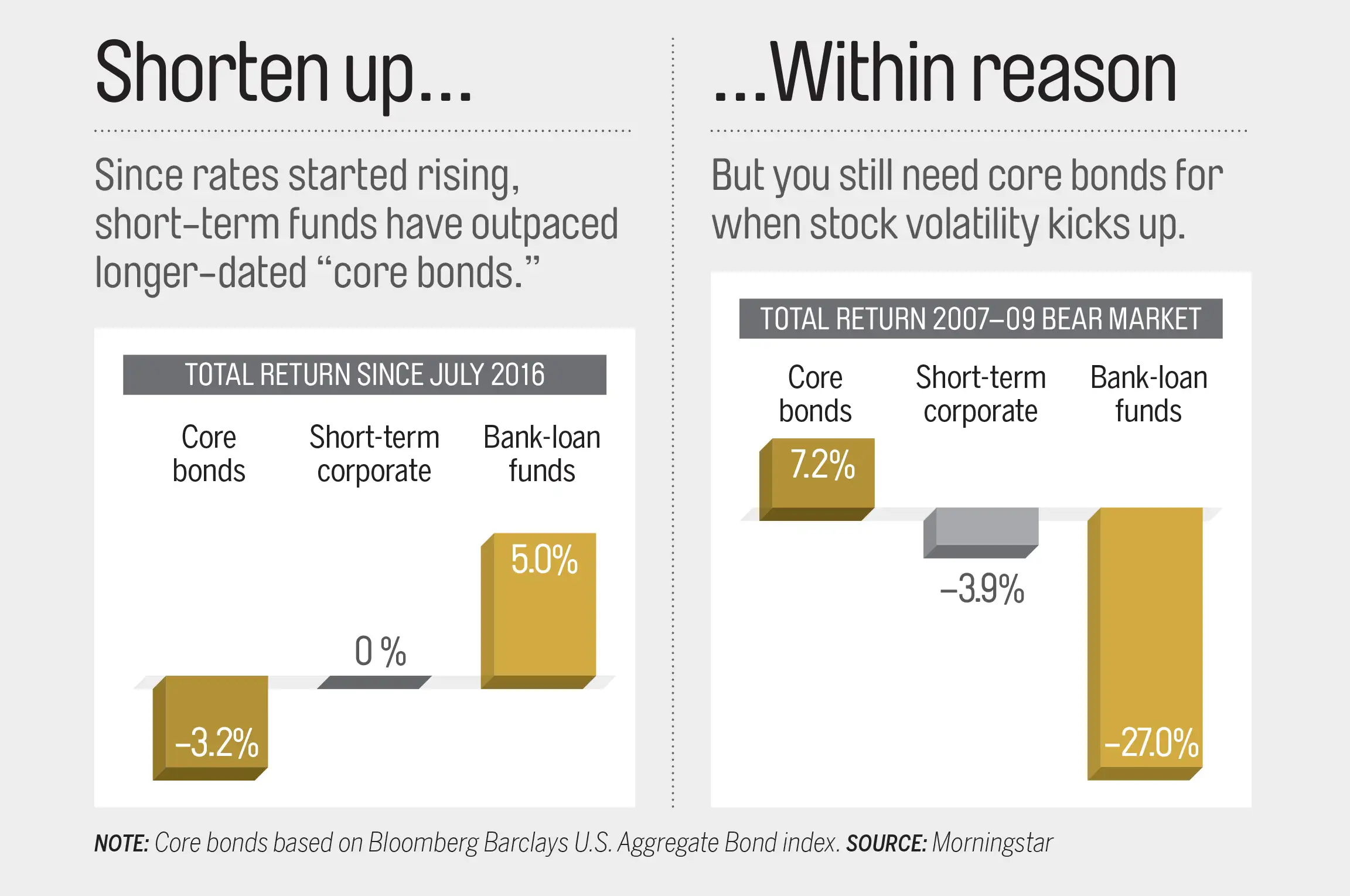

Since many bonds can wilt when the economy and inflation heat up, it's no wonder fixed-income prices have fallen lately, pushing yields on 10-year Treasuries up more than a percentage point since last summer. As a result, core bonds—intermediate- and longer-dated Treasuries and high-quality corporate bonds that anchor many retirement portfolios—have lost more than 3% since July.

There's no need to panic. "It may sound perverse, but there is a benefit to rising rates," says Matt Toms, chief investment officer for fixed income at Voya Investment Management. "If you're patient and are reinvesting the income, over time you are going to be better off with the higher income payout."

And while rates are rising, they aren't likely to keep accelerating this sharply. Ten-year Treasury yields are expected to roam between today's 2.5% and 3% or so this year, mitigating price declines.

Still, there can't be much potential for price gains. "Investors have been spoiled with the good returns bonds have delivered for years," says John Canally, chief economic strategist at LPL Financial. Now it's time to learn how to steer your bond portfolio safely in the new landscape of rising rates and risks.

Look to the Short Term

When rates rise, the price of older, lower-yielding bonds fall. But short-term debt loses less than longer-dated securities.

Another reason to tilt toward shorter-term debt: With stimulative federal spending and tax cuts expected to prolong this aging recovery, high-quality firms should be more than able to pay their debts in the short run. "We can look at corporate balance sheets and have confidence of their cash flow over one, two, or three years," says Warren Pierson, senior portfolio manager with Baird. "That's harder to do when you are investing in bonds with 10-, 15-, and 20-year maturities," he says.

On our Money 50 recommended list, Vanguard Short-Term Investment Grade (VFSTX) has a duration of 2.6 years, implying if rates were to rise one full point, the price of the fund's holdings would decline 2.6%. The fund has beaten more than 75% of its peers over the past three, five, 10, and 15 years.

Bank on Higher Income

Another type of short-term fund to consider as rates are climbing: those that invest in floating-rate debt, also known as bank loans. When rates lift, yields on many of these securities float with the market. Since rates started rising in July, these funds have gained 5%.

But be aware that floating-rate securities are typically issued by companies with below-investment grade balance sheets. The average holding in PowerShares Senior Loan ETF (BKLN) is rated B, landing squarely in "junk" status. That makes these funds an alternative to longer-dated high-yield bonds.

Add Some Inflation Protection

Remember why rates are rising to begin with. Currently, five-year Treasury Inflation-Protected Securities will outperform five-year Treasuries if inflation comes in above 1.86%. That's below the 2% or so inflation rate that is expected to bubble up this year. Money 50 fund Vanguard Treasury Inflation Protected Securities (VIPSX) yields more than 3%.

One caveat: TIPS are about twice as volatile as a core bond fund, so limit your investment to just 10% or so of your core bonds.

Don't Over-Shift Your Core

While core funds are more at risk than shorter-dated bonds, "a core bond fund can still play a very constructive role in a diversified portfolio," says Toms. "Those bonds do a good job of offsetting equity volatility."

To be sure, the typical core bond fund sports a duration of around five years. But a big reason you own bonds is to counteract potential stock market losses. And for truly long-term diversification, a five-year duration can still be a good compromise between higher rates and rising volatility.