Investors: 4 Smart Stock Moves to Make Now

Money is not a client of any investment adviser featured on this page. The information provided on this page is for educational purposes only and is not intended as investment advice. Money does not offer advisory services.

After getting off to a fast-and-furious start following the presidential elections—with the Dow Jones industrial average racing past the 21,000 mark for the first time in history—the stock market shifted into neutral in early spring. And then it was thrown for a loop, as controversies and investigations in Washington threatened the Trump administration's agenda of infrastructure spending and tax cuts.

Time for investors to slam on the brakes? Hardly. You shouldn't assume that the growing hazards on Wall Street are a sign that the eight-year-old bull market is nearing an end.

Instead, consider this moment as the stock market's equivalent of a yellow flag, offering investors a much-needed break to slow down and make any needed fixes or adjustments to their investments, not just for the next few laps but for the long race ahead.

To be sure, a midyear portfolio review may not seem all that necessary, given how well benign neglect has been working in your favor lately. Over the past five years, for example, U.S. equities have delivered annualized total returns of 15%. That's five percentage points higher than the long-term historical average for stocks—with nary a bear market in sight.

What's more, even with the recent slowdown in stocks, the S&P 500 index is still up 8% so far in 2017 while the Nasdaq composite index has gained more than 15%. Both indexes have recently hit their all-time highs.

Even if you haven't been a dedicated re-balancer—that is, if you haven't periodically reset your mix of stocks, bonds, and other asset classes back to your desired allocations— you really haven't paid a price for letting your winners run. And run. And run.

At least so far. "Bull markets can lull you into doing nothing as they make all investors look smart," says Hans Scheil, chief executive officer of Cardinal Retirement Planning in Cary, N.C. "But the time to review your portfolio is before a market correction, not after."

The odds are also good that after an eight-year-old bull market—which ranks as the second longest rally in history—your perception of risks may be somewhat diminished. Behavioral experts refer to this as recency bias, when investors are predisposed to believe that their investments will continue to perform as they have been doing.

On the other hand, your tolerance for investment risk probably has not changed all that much. If anything it has gotten more conservative as you are now nearly a decade closer to your financial goals, including funding a long and comfortable retirement. "I tell people to enjoy this bull market but make sure that you're not taking on more risk now," says New York City investment adviser David Schneider.

Here's how to make sure your investment risks are under control and give your portfolio a thorough once-over to ensure that it—and you—are ready for the long road ahead:

Get Your Allocation Back on Track

Chances are your strategy has strayed, even if you haven't touched your portfolio lately.

How? The bigger-than-average gains for U.S. equities over the past five years—coupled with the modest performance of bonds and the downright disappointing returns for foreign investments—have likely altered your allocations to stocks, bonds, and other assets. This is especially true if you haven't been steering your investments back to your original weightings on an annual basis.

For instance, say you started out five years ago with a balanced portfolio that consisted of 40% U.S. stocks, 20% international equities, and 40% in core bonds. And let's assume you didn't rebalance that portfolio anytime since. By simply letting your winners (and losers) ride, market forces will have morphed that 40-20-40 portfolio into one that's 52% invested in U.S. stocks, 19% in international equities, and 29% in bonds (see chart).

This may not seem like a big deal. But for one thing, you now have a portfolio that's roughly 70% stocks and 30% bonds, instead of the more conservative 60% equities/40% fixed-income mix. And considering that you're now five years closer to retirement, even keeping 60% of your retirement savings in stocks may be too risky, depending on your age and current circumstances.

Moreover, this new strategy leaves you overexposed to the priciest part of the global markets that have done the best lately—U.S. stocks—while being light on those investments that are relatively cheap (foreign equities) and provide ballast for your portfolio when U.S. stocks falter (fixed income).

"Over time the only way to make money is to be a contrarian," says Scott Clemons, chief investment strategist at Brown Brothers Harriman. "Rebalancing is forced contrarianism in that you sell some winners and move money into the other parts of your portfolio that have lagged" and are cheaper as a result.

But rebalancing doesn't simply mean selling some stocks and using that money to replenish your bond exposure. Within your equity portfolio, there are some moves to consider as well:

• Reset your mix between domestic and foreign shares. Going back to our prior example, if you started out with a 60% stock/40% bond portfolio in which two-thirds of your stocks were held in domestic shares, that strategy has shifted too. If you had not rebalanced over the past five years, the equity portion of your portfolio would be more like 75% U.S. and 25% international today.

So now is the time to sell some of your domestic exposure and use those proceeds to shift into cheaper foreign equities; more on this in a moment. Also read 3 Good Reasons You Should Be Investing Overseas Now.)

• Rebalance your U.S. stock holdings as well. The domestic stock universe is generally divided into two groups: "value"-oriented shares of beaten-down or overlooked companies; and "growth" stocks, which are shares of fast-growing companies that are firing on all cylinders.

Normally you'd want to split your equity stake down the middle, with about half in growth and half in value. But so far this year, growth stocks in the S&P 500 have returned about 13% while value has gained just 3%. And over the past decade, growth shares have returned about 7.5% annually—two and a half percentage points better than value stocks.

So consider trimming your growth winners and redeploy that money into value to restore that balance. Why? For starters, if a market correction is lurking around the corner, stocks with loftier valuations tend to suffer bigger losses. And value stocks tend to trade at far more attractive prices. The typical stock in the S&P 500 Value stock index sports a price/earnings ratio of 17, vs. 23 for growth stocks in the S&P 500 index. Because of that valuation advantage, value stocks also tend to outperform growth shares over very long periods of time.

Check out our Money 50 list for solid value minded funds. Among the best options on our recommended list of funds and ETFs are Dodge & Cox Stock Fund (DODGX) and PowerShares FTSE RAFI U.S. 1000 ETF (PRF).

Avoid Big Tax Bills on Stock Growth

Rebalancing inside your retirement accounts is easy, as there is no tax bill when you sell stock, fund, or ETF shares within a tax sheltered 401(k) or IRA. Selling shares in a regular, taxable account is trickier.

If you've owned the investment for at least a year, you must pay the long-term capital gains tax, which currently stands at 15% for most investors. And right now it's probably unlikely you can find sizable losses in your portfolio that you can also sell to offset those gains to lower your taxes.

You're not completely out of luck, though. This bull market has likely set you up for the opportunity to score a rebalancing and tax win by donating shares of appreciated assets to a charity.

When you donate appreciated shares you get a rare twofer. You owe no capital gains tax, and you get to claim the donation as a charitable contribution on your itemized return. For example, if you had a $25,000 capital gain when selling a holding from a regular account, your federal capital gains bill could be $3,750.

Donate the winning investment and you avoid the $3,750 tax bill, and your charitable deduction would be worth $7,000 if you are in the 28% federal income tax bracket.

Not all charities are equipped to deal with donated assets, so you'll need to ask upfront. Another option is to set up a donor-advised fund (DAF). With a DAF you donate your stock into an account that you agree to disburse to charity. You can make those gifts pronto or wait years until you're ready to make the donation. But the minute you move an asset into a DAF you avoid the capital gains tax and are entitled to a charitable deduction for the current tax year.

This could be an especially good time to consider donating appreciated stock and fund shares. If the Trump administration and Congress push through lower income tax rates for 2018 and beyond, the value of a 2017 deduction will generate more tax savings. Fidelity, Schwab, and Vanguard offer donor-advised fund programs.

Add More Foreign Stocks

In addition to rebalancing your exposure to foreign stocks, now may be a good time to think about increasing your weighting as well.

There are a couple of reasons why: First, foreign stocks have lagged U.S. shares for several years now. Over the past decade, international stocks have returned a mere 1% a year, while domestic equities have delivered annual returns of about 7%, according to Morningstar.

"If you look back over many, many decades, what you find is that there's a long-term mean reversion where things that do well for a period of years end up doing poorly over the next few years—and vice versa," says Chris Brightman, chief investment officer for Research Affiliates.

Just refer to recent history. "If you looked at the decade that ended in 2000, U.S. stocks were the leading asset class. But if you looked at the decade that ended in 2010, it was quite the reverse," Brightman says, noting that foreign stocks trounced the S&P 500 index during what was considered a "lost decade" for domestic equities.

The other reason to be bullish on overseas stocks is that they're one of the few attractively priced assets in today's market. U.S. shares are currently trading at a price/earnings ratio of 29, based on 10 years of averaged profits. That's 80% higher than the historical median P/E of 16. The market has been this frothy only twice before: in the late 1990s, during the dotcom bubble, and just prior to the start of the Great Depression in 1929.

By contrast, foreign stocks in Europe and Japan are trading at a P/E of 15, which is roughly 30% below their historical levels, according to Research Affiliates. And foreign stocks based in the emerging markets are trading at a P/E of 13, down from the typical 17.

Today, investors between the ages of 35 and 50 invest only 14% of their stock portfolios abroad, according to Fidelity. That's down from an 18% allocation in 2009. Younger investors have even less exposure—just 13% on average.

Yet a study by Vanguard found that the optimal strategy is to keep at least 30% and up to 40% of your stocks overseas.

"Though there is no expiration date on the U.S. bull market, now is an opportunity to rebalance into non-U.S. stocks, where valuations are much better," says BBH's Clemons.

His firm is advising clients to shift three to four percentage points out of their U.S allocation into international equities. In other words, if you normally keep 45% of your portfolio in U.S. shares and 30% in foreign, you should shift that to about 42% in the U.S. and 33% abroad.

Ramp Up Your Savings Rate

It's human nature to assume that the stock market's stellar performance in recent years will persist for years to come. But history shows that the more expensive stocks are, the less likely they are to deliver decent returns over the subsequent decade.

AQR Capital studied the historical performance of stocks based on P/E ratios using 10 years of corporate profits. It found that when the market's P/E was above 25—as it is now—the average annual real return after inflation has historically been less than 1% over the subsequent decade. By contrast, when the market's P/E is below 10, stocks have historically produced double-digit gains.

"This doesn't mean U.S. equities will do poorly," says Kate Warne, investment strategist for the brokerage Edward Jones. "They will likely outperform bonds. But just understand that what you earn over the next five years is not likely to match the past five years."

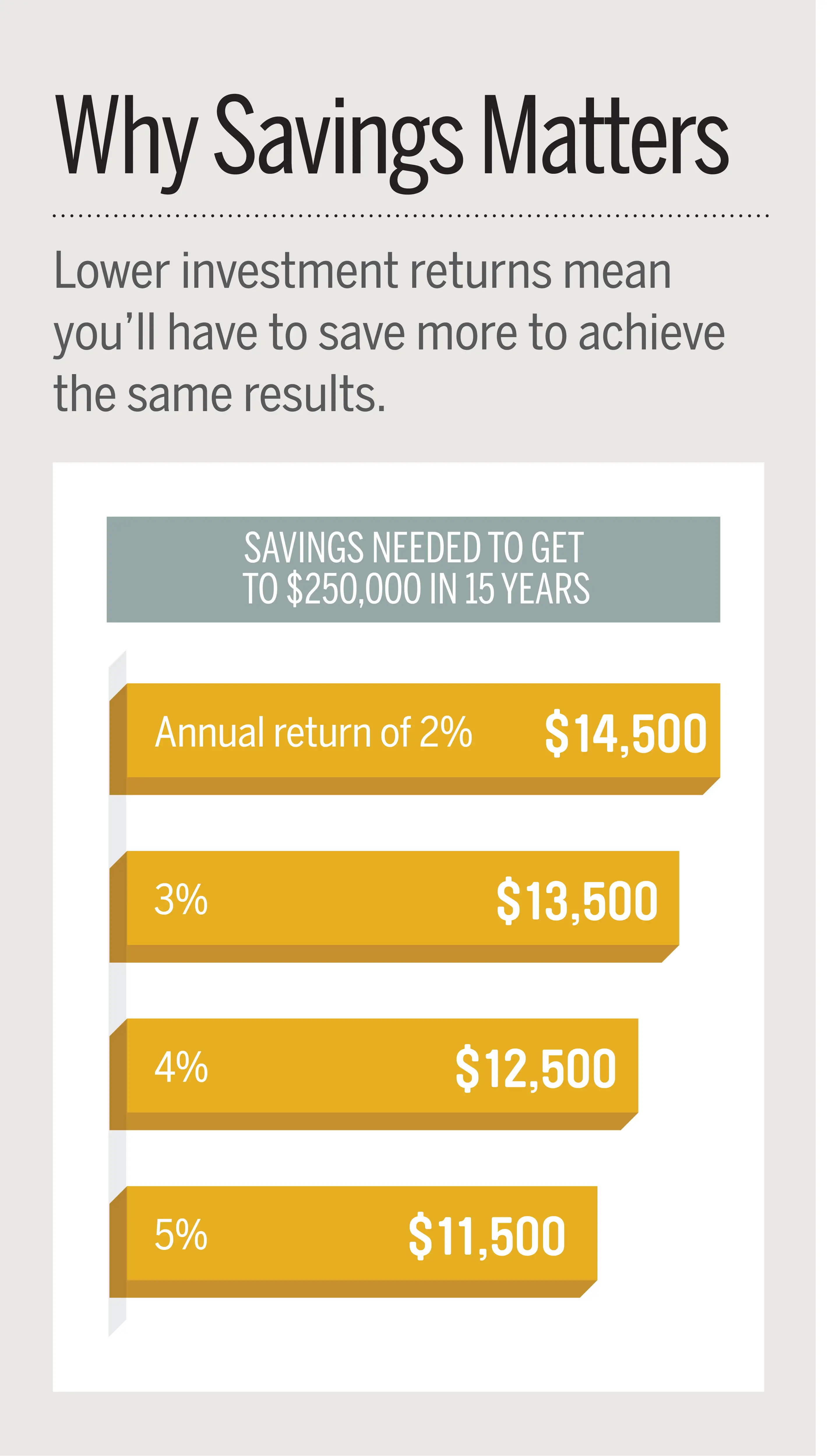

The surest way to counteract this isn't to take on more investment risk by increasing your exposure to the riskiest stocks. Rather, it's to boost how much you save and invest.

Say, for instance, that you want to amass $250,000 over the next 15 years. Over the past 15 years, a balanced portfolio of 70% stocks and 30% bonds produced annual returns of about 7%. That meant you could reach that goal by saving about $10,000 a year.

But if that same balanced portfolio produces only 4% going forward, you could still reach your goal by saving $2,500 more a year. So rather than roll the dice with your strategy, boost your 401(k) contribution rate by a percentage point or two. It's the market's surest bet.