Bank Branches Are Vanishing from Rural America. Here's Why That's a Big Problem

Rural Americans are losing access to bank branches. For some, that may be putting cheap and convenient financial services out of reach, according to a new study.

The shift is driven in large part by the rising popularity of online banking. But, while younger, web-savvy customers have adapted quickly to online banking, the changes have been isolating to less wealthy, rural Americans, research shows.

Overall roughly half of U.S. counties lost bank branches between 2012 and 2017, researchers at the Federal Reserve found. While urban and rural counties both lost branches at roughly the same rate — seeing an average 7% decline — the effect was more pronounced in rural areas, the researchers said, because rural counties had many fewer bank branches to begin with.

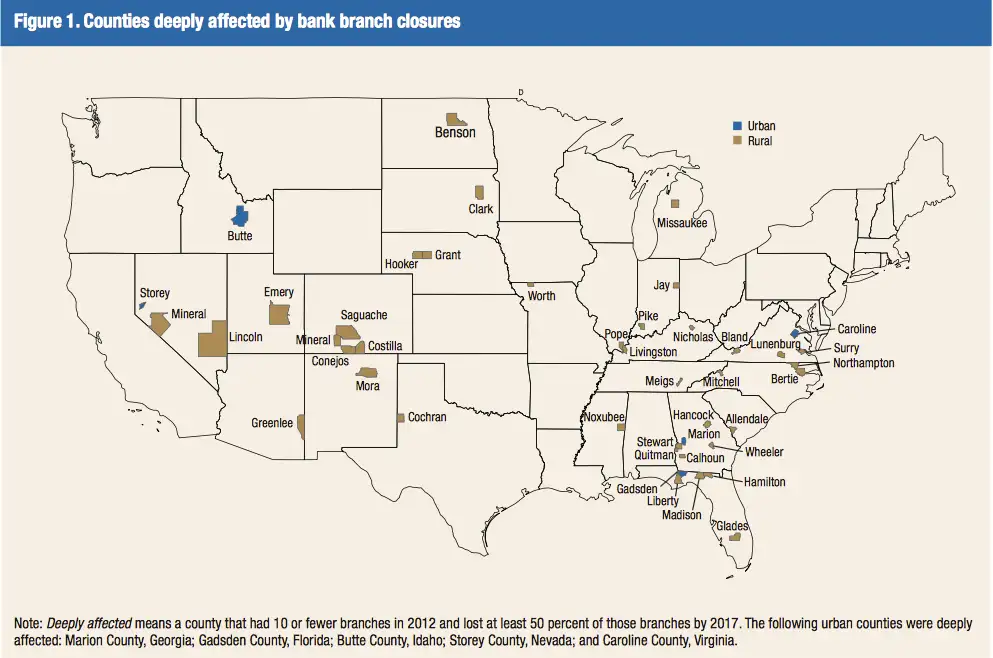

About 40 rural counties qualified as “deeply affected,” according to the Fed, meaning the county had 10 or fewer branches in 2012 and had lost at least half of those five years later. Fed researchers found there are also 100 banking markets, most of them rural, that went from containing at least one bank’s headquarters to containing no headquarters, due to industry consolidation.

The most affected communities tended to be poorer, with lower median incomes and higher poverty rates. Residents also tended to have less education and were more likely to be African American. Those residents also often lacked transportation options to reach a new location.

Not having access to a bank branch can make managing money more difficult, especially for rural, lower-income residents who rely on branches more heavily than consumers in wealthier, urban areas. Branches provide an important face-to-face channel for resolving problems and handling more complicated transactions. In fact, even as banking has shifted to online and mobile channels, bank branches are still the most commonly used way for individuals to access their accounts, according to the report.

Research from consulting firm Bain, for example, found that customers who are taking out a loan or disputing a fee report higher satisfaction when interacting with a person compared with a screen.

Listening sessions conducted by Fed researchers found many rural residents who lost bank branches switched to online banking. Still, others said that costly or unreliable broadband service made switching difficult, while older customers lacked the digital literacy to use online or mobile banking options.

If you live in a community with little access to bank branches and you've started managing money digitally as a result, it's likely worth considering switching to online bank. They tend to offer lower fees and more generous interest rates anyway. Ally Bank and Alliant Credit Union, both winners in Money's 2019-20 Best Banks ranking, offer reimbursements for ATM fees and interest rates on their checking and savings accounts that are at least 7 times the national average.