Do I Need a Financial Adviser to Manage My IRA Rollover?

More than 300,000 U.S. professionals call themselves financial advisers, according to industry researcher Cerulli Associates. That universe covers everyone from Wall Street brokers and bank and insurance reps to independent money managers. What kind you hire could have a big impact on just how your IRA is invested.

Many advisers work with wealthy investors, and in dollar terms they dominate the market, grabbing 70% of rollover assets, Cerulli reports. If plan providers know all about your 401(k), advisers have their own edge: They know you. A full 83% of the rollover dollars advisers capture come from existing clients.

Here, too, the incentive to bring your 401(k) in-house is strong: Once your savings are in an IRA, an adviser can earn 1% or more a year managing those funds or take an upfront commission of as much as 6%. For many advisers—just like savers—an IRA is likely to be the “biggest lump-sum contribution they ever see,” says Jason Roberts, chief executive of the Pension Resource Institute, a consulting company that helps advisers and others with compliance issues.

Finding that “in”

To be in line to get rollover dollars, some advisers, or the firms that manage them, are taking a page from the Fidelity and Schwab playbook: Run the 401(k) in the first place.

Since acquiring Merrill Lynch during the financial crisis, Bank of America has been building up its 401(k) business. In 2013 the bank signed up 750 new plans, vs. 263 new ones in 2012. “We love the retirement business,” said Andy Sieg, head of Global Wealth and Retirement Solutions, in a February 2014 presentation to Wall Street. The plans, Sieg noted, are “a feeder engine for core wealth-management relationships at Merrill Lynch and U.S. Trust, as individuals have needs outside of the plan or roll-out of retirement plans.”

When mom-and-pop advisers don’t have an in, they have to carve one out. David Royer, a former financial adviser, teaches a $1,295 course titled “Keys to the IRA Kingdom” that promises to help advisers learn the tax rules so that they can “capture the exploding 401(k) rollover market.” Advisers have an important role, he says, since confused investors who fall afoul of IRS rules could face needless tax bills. “Mistakes are costly and often irreversible,” Royer warns. “If you have chest pains, you go to the doctor. You don’t go to the pharmacy and say, ‘Give me a bottle of nitro.’ ”

Out of bounds?

Several regulators, including the Securities and Exchange Commission, are taking a closer look at how advisers market rollovers. Kevin Goodman, the SEC official who oversees broker-dealer examinations, says an inquiry started in part because SEC employees were getting emails urging them to leave the Thrift Savings Plan, the federal government’s standout, ultra-low-cost equivalent of a 401(k).

The emails, which warned of “keeping all of your eggs in one basket,” could have been construed to suggest that an event like 2013’s debt crisis put plan assets at risk. “A reasonable person could have read them that way,” he says.

The SEC’s approach, Goodman says, will be to focus on pros with unusually high “batting averages” in terms of winning rollovers. Choosing to roll over is a complicated decision involving costs, investments, and tax rules, Goodman notes, and “the many nuances involved need to be clearly presented.”

Best Moves

— Grill your adviser. When your existing financial adviser suggests a rollover, ask why. Some income strategies, such as building a ladder with individual bonds, are difficult or impossible to execute within a plan. If the rollover recommendation is merely to help you pick funds, think twice. “They should be able to do that from looking at your 401(k) statement,” says Wade Pfau, professor of retirement income at the American College of Financial Services. Plus, your adviser should at least consider annuities for you. “If your adviser rejects them out of hand, that’s a bad sign,” says Pfau.

— Know whom you’re talking to … The trickiest part of hiring an adviser if you don’t already have one may be figuring out whom you’re working with. In a bank branch, brokerage, or insurance office, you may meet an adviser who operates solely on commissions. Registered investment advisers, found at financial planning practices as well as Wall Street firms, charge 0.5% to 1.5% a year of your assets.

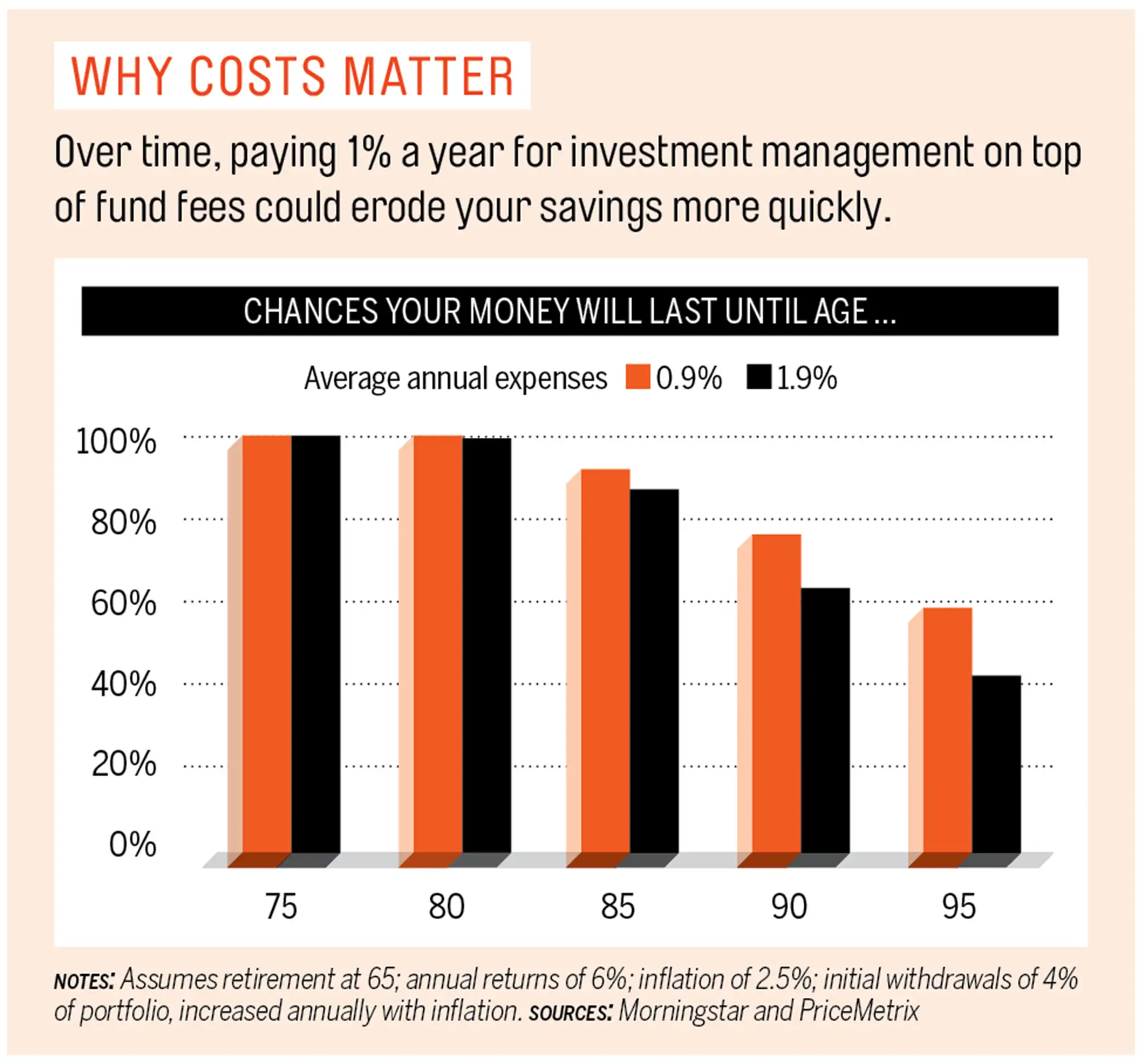

— ... and his biases. While commission advisers must recommend products that are “suitable,” based on factors like your age and risk tolerance, beyond that they are largely free to pitch whatever provides them the fattest payouts. Advisers who levy a fee don’t have the same incentive to sell you a particular product, and by law they must act in your best interest. But even those pros have conflicts. They can’t charge a fee on what’s in your 401(k) or an annuity, giving them a reason to put you in an IRA. Avoid commissions. In today’s world of super-cheap index funds and ETFs, the case for paying a high upfront commission is hard to make, especially since commission advisers often sell expensive actively managed funds. A possible exception: You want an annuity (see next section).

— Determine the adviser’s style. Seek out someone who works with others like you—similar-size portfolios, say, and similar goals. Adviser Mark Atherton of Reston, Va., suggests asking whether the planner favors an active or a passive investing approach and whether other services such as estate planning are offered.

— Do a background check. When an adviser charges a fee, his firm should be registered with the SEC or his state securities regulator. Before you meet, ask for his “Form ADV Part II Brochure,” which outlines the services provided, investment strategy, and fees. Plus, put any adviser’s name into FINRA’s BrokerCheck at finra.org. This will tell you about any “disclosure events,” from felony convictions to disputes with customers.