4 Disastrous Retirement Mistakes and How to Avoid Them

When Cindy Rogers was offered early retirement at Verizon in 2010, the former technician says she didn’t think she could possibly accept. After all, she was only 49.

Then she talked to a financial planner she’d heard of through her union, who assured her she could make it work. So Rogers left Verizon, rolling a $529,000 lump-sum pension payout and an $85,000 401(k) plan into an IRA, buying a variable annuity, and starting up monthly paychecks.

Four years later, it’s not working. She’s withdrawing too much too quickly for her money to last, Rogers explained in a May complaint to the Financial Industry Regulatory Authority (FINRA). And because her withdrawals violate the tricky IRS rules for tapping an IRA early, she faces a steep tax bill. Instead of living the retirement she envisioned, she’s back at work as a $10-an-hour home health aide. (She made about $80,000 at Verizon.) “I’m in a horrible position,” says Rogers.

As you near retirement, no decision is harder—or has higher stakes—than what to do with the nest egg you’ve spent years building up. The crucial decision you face is whether to roll your workplace retirement plan into an individual retirement account, and then how to invest the funds. The average 401(k) balance for high-income workers 60 and older is $414,000, according to benefits consultant Aon Hewitt. Those big sums are catnip to financial pros of all stripes—including advisers peddling misleading or just plain awful advice that could tank your retirement savings. Even worse, you could be the victim of outright fraud.

While no agency tracks rollover complaints, regulators have stepped up attempts to educate pre-retirees about the risks in recent years. “These cases keep popping up,” says Wisconsin securities commissioner Patricia Struck. “We know these people are desirable targets, because they have these pools of money that will soon be accessible. It’s scary.”

No two rollover disasters unfold the same way, but these four rollover problems tend to crop up the most.

1. High Fees Chip Away at Your Savings

Lured by a promise of higher earnings or guaranteed returns, you could roll your money into an investment that’s far more expensive than what you already own. Financial advisers gunning for IRA rollover dollars like to pitch variable annuities, insurance products that allow you to invest in stock and bond funds, tax-deferred, and later convert your balance into regular income.

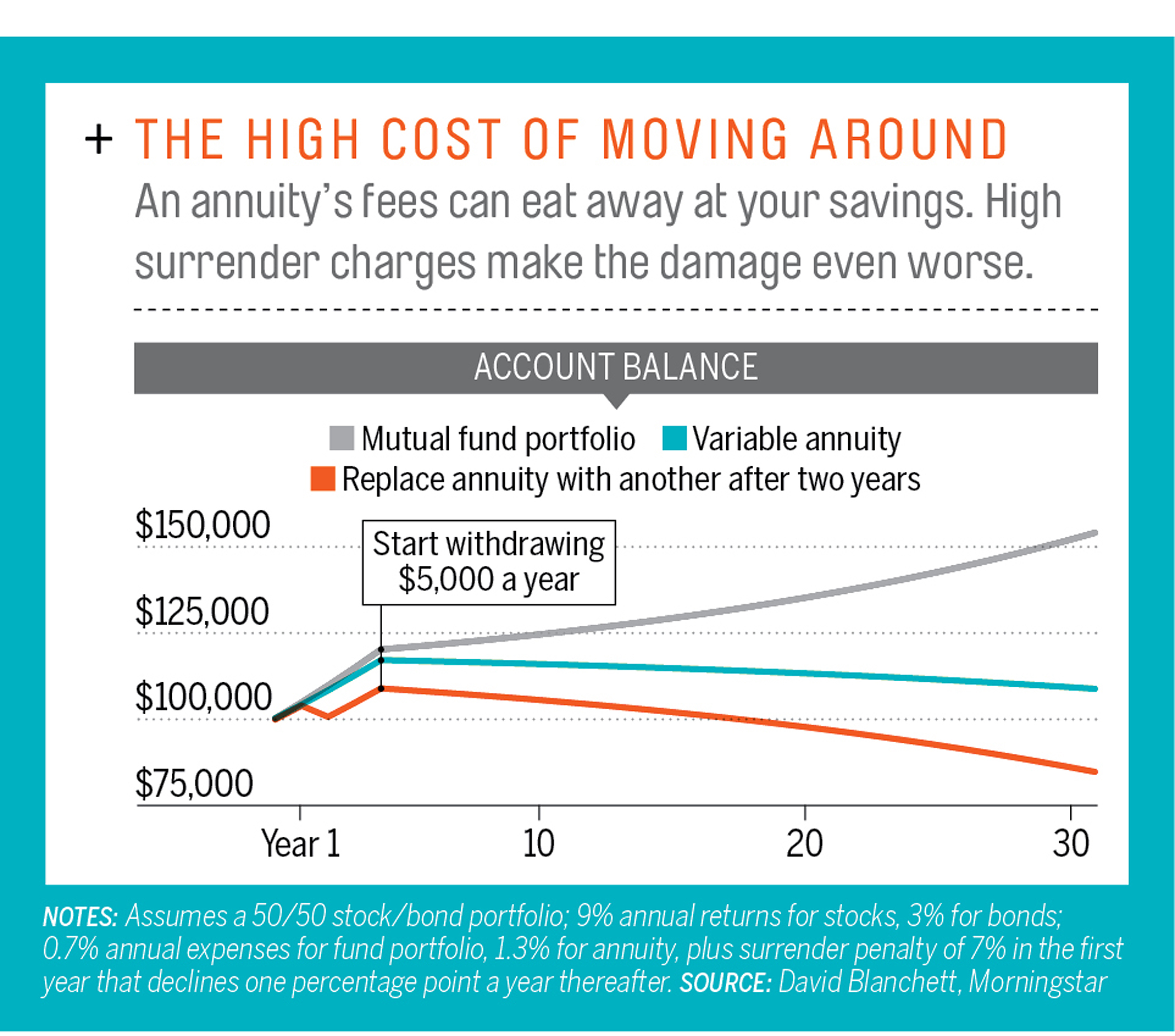

The drawback is the high fees you’ll pay every year for a VA—typically 2.4% of your assets for investment management and extras like income guarantees, according to Morningstar. But the more serious trouble comes when an adviser won’t stop at one, exposing you to large penalties.

In June a group of 16 investors in Mississippi, half BellSouth retirees, filed a complaint with FINRA alleging that starting in 2004 a Morgan Keegan broker had persuaded them to take their pensions as a lump sum or tap other savings and buy variable annuities. Within three years, according to the complaint, the broker had the investors cash in the annuities and buy new ones. Some switched into a third VA. Raymond James, which acquired Morgan Keegan in 2012, declined to comment, citing pending litigation.

In any given year, 40% to 60% of variable annuity sales are switches, according to the Insured Retirement Institute. What makes this kind of turnover so tempting to advisers are the high commissions they can earn on a new sale—typically 5% to 6%, reports the industry research firm Aite Group. For index annuities, which tie your returns to a stock index such as the S&P 500, the payout can hit 8%.

If you cash out in the first six to seven years, however, you’ll pay a surrender charge that can start as high as 7%. As the graphic below shows, early-exit fees on top of even moderate annual expenses can seriously erode your retirement savings.

A sign-up bonus that adds, say, 5% to your account might tempt you to eat that charge, though you typically must wait years to get it.

Index annuities are among the most common pitches Julie Preuitt sees. An assistant regional director in the Fort Worth office of the Securities and Exchange Commission, she is leading an SEC initiative to help federal employees— 25% of whom are 55 and older—make informed rollover decisions. “The need for more education is incredible,” she says.

2. You Needlessly Give Up a Sure Thing

An adviser might persuade you to cash out your pension, perhaps by suggesting you can earn higher returns. Judson Lee, a lawyer for the Mississippi investors, says the Morgan Keegan broker often noted that pensions wouldn’t let them leave an inheritance, while investing lump sums with him would. Money was not able to reach the broker, who appears to be out of the business.

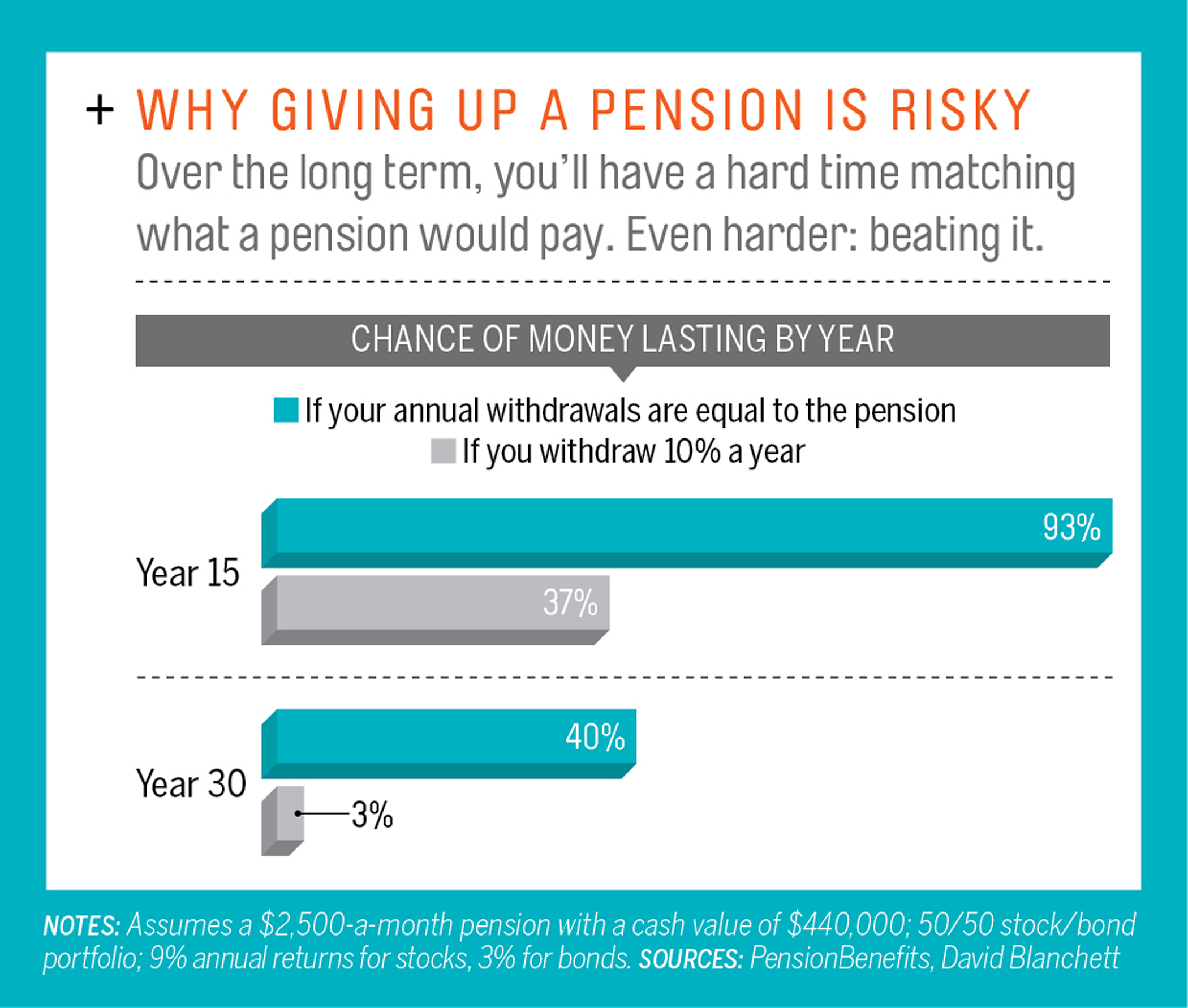

When given the chance, 56% of workers take a pension as a lump sum, according to a study by the Employee Benefit Research Institute. That could be smart in certain cases—say if you have health problems.

Cashing out, though, is definitely in an adviser’s interest, since your pension becomes a pool of money he can earn a commission on. Financial planner Sheryl Garrett, who founded a network of planners who charge by the hour, has been an expert witness in about a dozen arbitration and court cases involving lump-sum pension withdrawals, most involving a switch to a variable annuity. “Tens of thousands of dollars are at stake,” she says. “For a financial adviser, it could translate to a new car.”

Yet as you can see in the graphic at below, cashing out can backfire over time. With a pension, those who die early subsidize folks who live a long life. If you take a lump sum and buy an annuity or invest on your own, you have to be more conservative to make sure your money lasts, says Garrett. You simply can’t match a pension check.

Cashing out also shifts risk from your employer to you, notes Barbara Roper, director of investor protection at the Consumer Federation of America. “Things happen. If they happen to happen in the first few years of your retirement, you are seriously at risk,” she says.

3. You Go Through Your Money Too Fast

Another pitch is the tantalizing prospect of early retirement. The danger is that it’s based on sloppy or misleading math, says Gerri Walsh, head of investor education at FINRA.

Verizon retiree Cindy Rogers says her adviser told her that her annuity would produce ample income to cover her expenses, while the principal would last her lifetime, according to her FINRA complaint. But Rogers’ $3,700 monthly payouts mean she’s withdrawing 8% a year—twice what’s typically suggested for a retiree who’s 65, let alone 49. Including fees, she’s depleting her savings at a rate of 11% a year.

Plus, Rogers owes an estimated $9,000 in tax penalties. She was able to tap her IRA before 59½, the normal age for penalty-free withdrawals, under exemptions spelled out in Section 72(t) of the tax code. FINRA warns that advisers present 72(t) withdrawals “as a ‘little-known loophole’ that allows you to retire early.”

The trouble is, you must withdraw a steady amount, which is capped based on your age. “You’re not going to get as much as you think,” says CPA Ed Slott, who runs IRAHelp.com. Going over the limit just once triggers a 10% penalty, plus interest, on all your withdrawals.

Rogers’ adviser, Joan Norton, says in a filing with FINRA that her client was aware of what she was getting and that Norton doesn’t hold herself out as a tax pro. Brooke Galassi, senior compliance officer at the brokerage Norton is affiliated with, Ausdal Financial Partners, declined to comment.

4. You Make Bets That Are Foolhardy

Chasing high returns can get you in trouble. Rolling money into what’s known as a self-directed IRA so that you can shoot for the stars is especially perilous. The SEC estimates that in 2011 investors had $94 billion in this type of IRA, which lets you invest in pretty much anything, from real estate to tax liens.

Last year the state securities regulators association warned that because self-directed IRAs can hold exotic assets, which IRA administrators don’t generally vet, the accounts leave you vulnerable to risky pitches.

In a video of a 2013 sales presentation, Curtis DeYoung, founder of American Pension Services, a Utah-based retirement plan administrator, promised retirees the freedom to “take control of your own destiny” with a self-directed IRA. At the end of 2013 his nearly 5,500 clients had IRA accounts worth $352 million. But a lawsuit filed in April by the SEC claims that DeYoung steered $22 million in clients’ money into now worthless real estate investments and loans to friends. A lawyer for DeYoung told Money that the retirees chose the investments; the firm was merely an administrator.