Why Is Rolling Over My 401(k) Such a Big Deal?

This section of the Ultimate Retirement Guide has been adapted from “The One Retirement Move You Must Get Right” by Ian Salisbury, which appeared in Money’s July 2014 issue.

Financial services companies usually seek out new clients. In 2013 the brokerage Charles Schwab said it was walking away from some, namely several 401(k) plans covering more than 300,000 workers, with a total of $25 billion saved.

As Steve Anderson, Schwab’s executive vice president of retirement plan services, explained in a webcast for Wall Street investors the following February, the problem was that employers were making it too tough for Schwab to pitch individual retirement accounts to retiring or departing workers. “What we look for … [is] to communicate openly with their employees, to be able to have education meetings that would be Schwab branded, to be able to have rollover conversations,” he said. In a statement about the move, the company said cutting the plans, some of which were unprofitable, was part of a larger strategy of focusing on lower-cost investments while delivering advice within 401(k) plans.

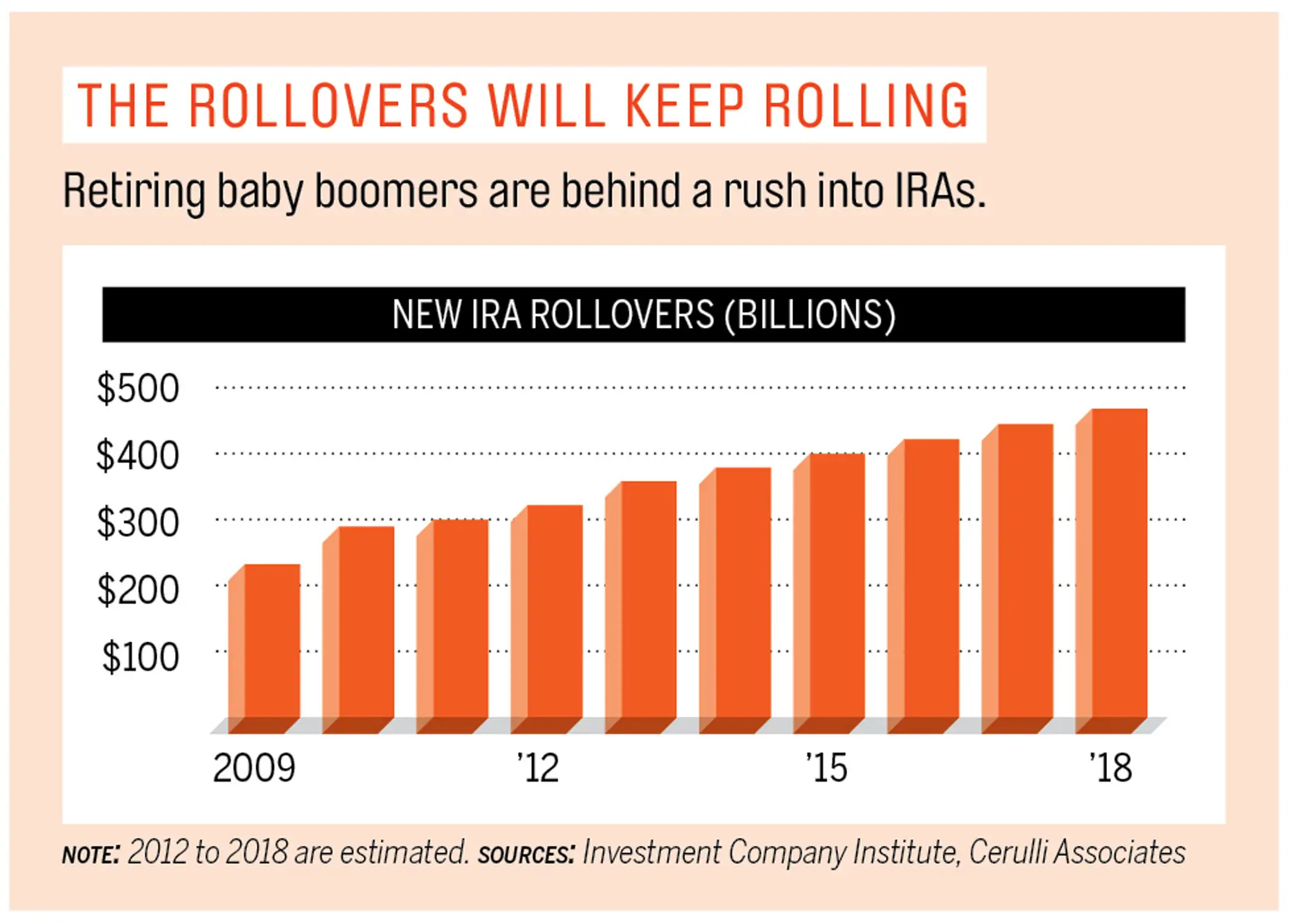

Schwab’s keen interest in “rollover conversations” is understandable. Americans have amassed $5.9 trillion in 401(k)s and similar plans. Now baby boomers are starting to hit the exits, fueling a rollover boom.

For fund companies, Wall Street brokers, insurers, and financial advisers, snagging a piece of that transfer can be lucrative, especially since IRAs are twice as profitable to run as 401(k)s are. “Rollovers are the biggest moneymaker in the retirement business,” says Michael Kozemchak, managing director of IIC, a consultant to retirement plans.

But if the IRA market is a multitrillion-dollar opportunity for the industry, it’s fraught with risks for you. You could pick the wrong product, pay too much in fees, or needlessly give up a standout 401(k)—all of which could add up to as less comfortable retirement.

The average 401(k) balance for workers 60 or older making $100,000 or more a year stood at $414,000 at the end of 2013, reports benefits consultant Aon Hewitt. Deciding what to do with that money—do you stay or do you go?—may be the most important financial call you’ll ever make. “If you get it wrong, it’s extraordinarily difficult to recover,” says Barbara Roper, director of investor protection at the Consumer Federation of America.

The six sections that follow will walk you through you what you need to know to stay on course, from the pitches you're bound to hear from financial professionals to the best moves you should make.